Last week we published a report on the impact of COVID-19 on payments. It looks not only at the devastating effect the pandemic had on some payment instruments and flows, but also for signs of change in customer behaviour that might point to what lies ahead. In this blog, I’d like to highlight three sets of data points, containing expected as well as surprising elements.

First, 76% of consumers surveyed by LINK, the UK ATM network, said the coronavirus will affect their use of cash over the next six months; most expected to use various forms of digital payments more. However, 10% reported that they wanted to pay cash, but it was not accepted. I do believe we’ll be using less cash going forward, but the last point is likely to be an anomaly from the early days of lockdown – there is too much political pressure to maintain access to cash for cash to stop being accepted and disappearing in the UK entirely any time soon.

Also, my report explores how the industry might migrate to “contact-free” payments, i.e. shopping experiences where users don’t have to touch a payment terminal at all. Among the examples of such payments discuss in the report are biometric contactless cards and voice commerce.

Fingerprints, a company providing biometric sensors found in many consumer devices, partnered with Kantar, a customer research company, to survey 1,200 consumers in the UK, France, and China. According to that study, 56% of consumers want a biometric card and 50% are prepared to pay more. Actually, both these figures are a little surprising. The first one sounds too low – why wouldn’t you want a biometric card? Only if you either didn’t understand what it was and its benefits, or you thought it would be too expensive. Which is why the second figure is a little higher than I would have expected in that context – it implies customers really value the security, convenience, and safety that a biometric card can provide, and are prepared to pay for it. Issuers should take notice!

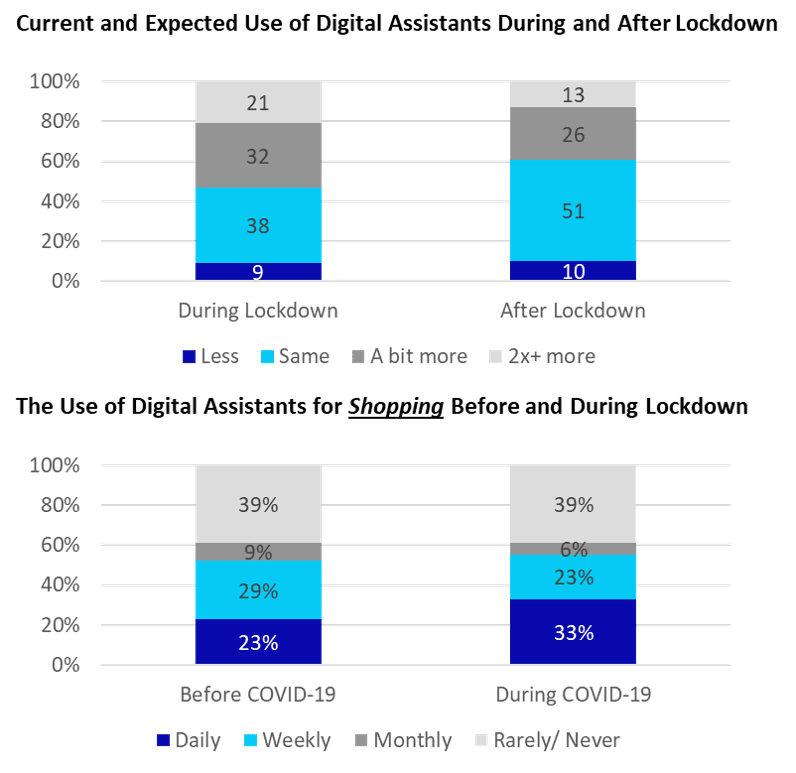

Voxly Digital, a software development agency focused on voice experiences, surveyed 400 UK-based consumers that use a voice assistant (e.g. Amazon Alexa, Google Assistant) during the COVID-19 lockdown in March. 53% said they used voice assistants more during the lockdown than before, with 21% saying their usage went up at least twice as much as before. Furthermore, 40% of users predicted they will also use voice more once the crisis is over than they did before. Finally, the percentage of those that use voice for shopping at least daily rose from 23% before the lockdown to 33% during it. The somewhat surprisingly high figures of daily shoppers can be explained by the fact that the respondents were all existing users of voice assistants, while around three quarters of the UK households don’t yet own a smart-speaker. Nevertheless, they do show that there is a clear demand for voice-based commerce.

Source: Voxly Digital

We will be discussing these and other developments in Retail Banking and Payments at an upcoming webinar, part of our Survive to Thrive webinar series. If you would like to join, please register here.

This blog is part of a data series in our ongoing coverage of developments around COVID-19. View other blogs within this series: