Don’t Be Scared S---less Small Business Bankers – Fintechs Are Coming to Partner

During JPMorgan Chase’s Earnings Call, Jan. 15, 2021, Jamie Dimon responded to a question regarding his 2015 warning that “Silicon Valley is coming”:

“I gave to the management team, my whole operating committee, a little deck that showed Visa, $500 billion; MasterCard, $350 billion; PayPal, $220 billion; Ant Financial, $600 billion; Tencent, $800 billion; Alibaba, $1 trillion. Facebook, Google, Apple, Amazon, you can go on and on. But absolutely we should be scared s---less about that.”

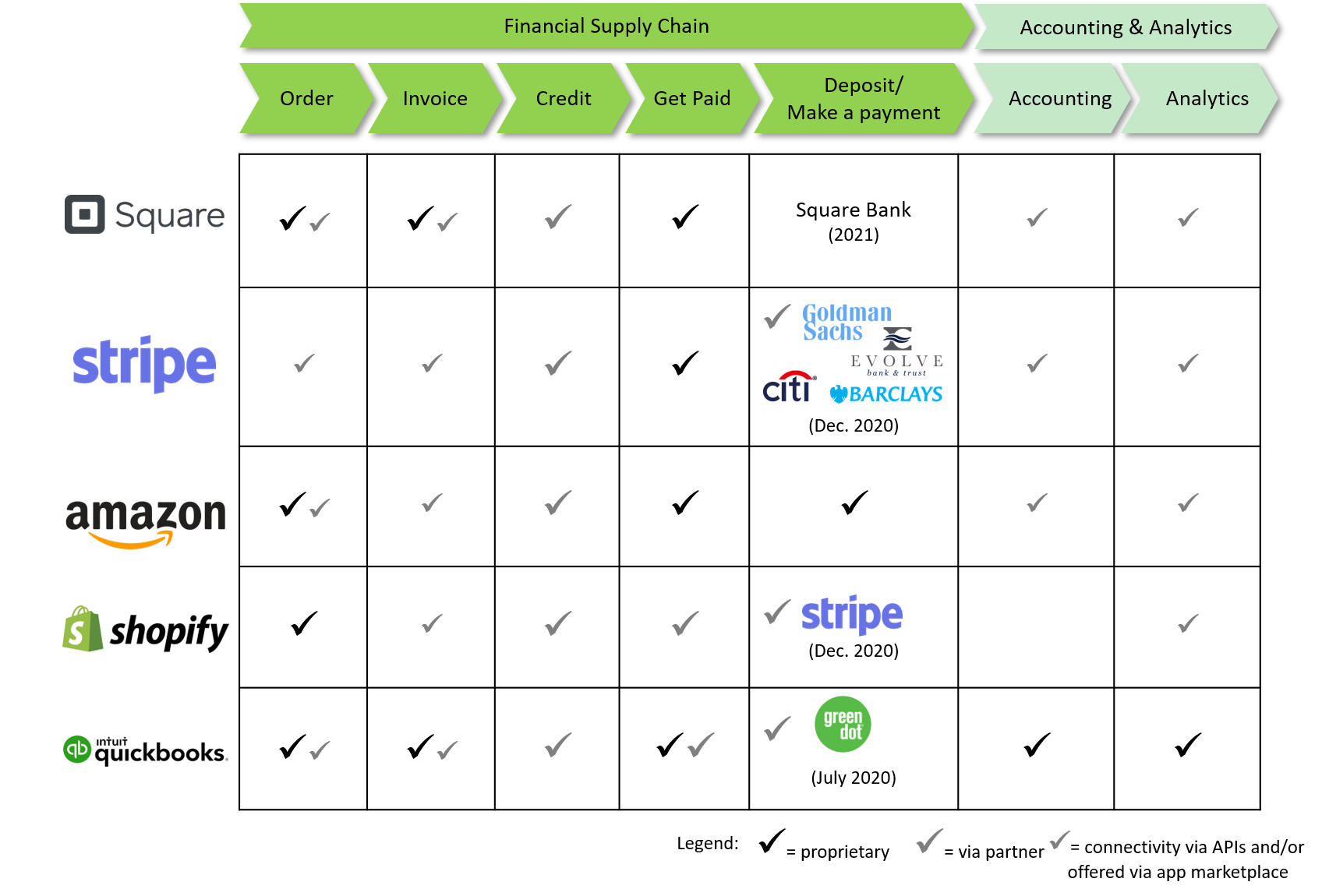

For the small business banker, in addition to Amazon, I would add Intuit ($107B), Square ($116B), and Stripe (aiming for ~$100B after ongoing fund raising). But I wouldn’t say small business bankers should cower in face of these next generation competitors. To the contrary, they should seize the opportunity to reinvent small business banking. It needs reinvention because small businesses view banking as well as financial management overall dramatically different from banks’ view. Small businesses think about workflows and banks think about products with most still offering “checking accounts.”

Reinvention translates into supporting each chevron in the financial workflows of small businesses and embedding banking services. With the addition of a deposit account these platform players are nearing the finishing line.

Figure 1: Next Gen Small Business Banking Competitors’ Value Proposition

While Dimon didn’t divulge how JPMorgan Chase was going to out compete Silicon Valley, he did say:

“…we have plenty of resources, a lot of very smart people; we just got to get quicker, better, faster which we do.”

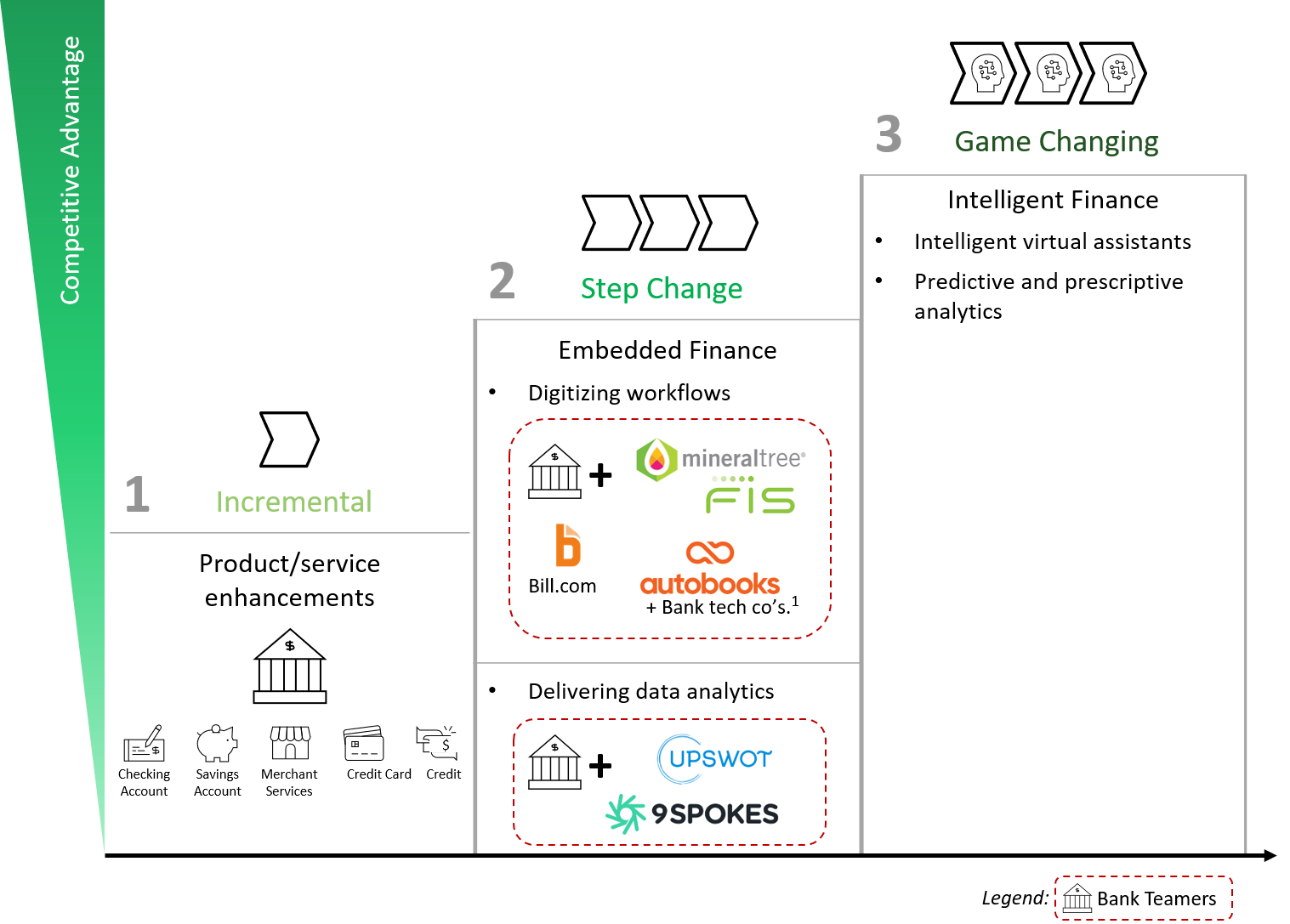

In my report, Reinventing Small Business Banking Part I: Pacesetters in Embedded Finance, I outline how banks can become “quicker, better, faster.” I delve into the important role partnerships can play and profile seven potential bank partners. Five are digitizing and simplifying workflows: Autobooks, Jack Henry & Associates (JHA) (which has embedded Autobooks in several of its solutions), Bill.com, MineralTree, and FIS (whose Invoice-to-Pay is powered by MineralTree). Two are delivering enhanced data analytics: 9Spokes and Upswot.

Figure 2: Achieving Step Change Through Partnerships

The game is on in small business banking, and banks have a right to win if they can reinvent. Confidence not fear should drive them.

Further to helping banks navigate and reinvent, Kieran Hines, a senior analyst at Celent, wrote Using Open Banking to Build Stronger SME Propositionsin which he discusses open banking and the opportunities to use embedded finance for service improvements. He analyzed over 100 TPPs in Europe leveraging PSD2 to offer services to SMEs and distilled 10 distinct value propositions.