Getting SME banking "right" is a huge opportunity for the industry. Despite the market for small and medium enterprise (SME) banking services being both large and highly dynamic, many banks fall short when it comes to meeting the needs of this customer group.

This situation is not new, and over time has led a range of niche and nonbank providers to enter the value chain and compete for a share of SME business. Indeed, it can be argued that we are witnessing the long-predicted unbundling of the SME banking offering into multiple constituent components, offered by a range of different providers. This represents a significant challenge for incumbent banks. While we have yet to reach a tipping point, financial institutions must consider their strategic responses or put substantial portions of their future SME banking revenues at risk.

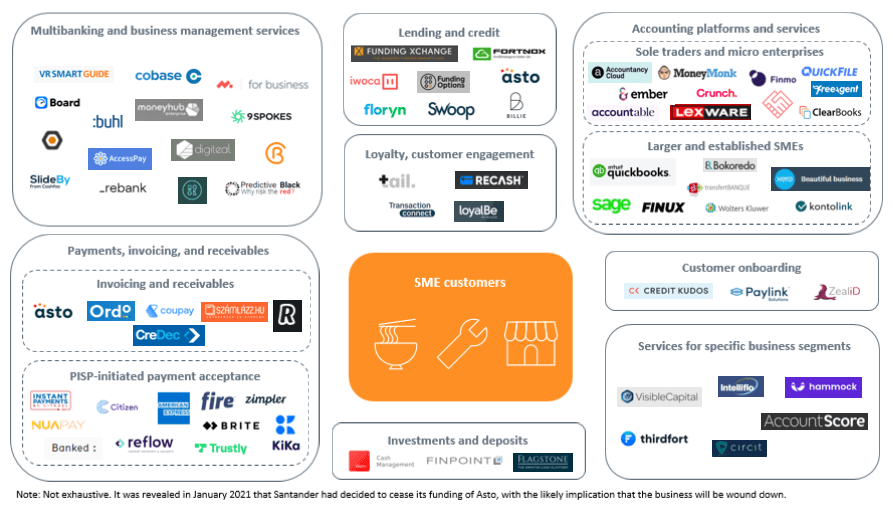

Open banking and the opportunities to use embedded finance for service improvements are increasing this competitive threat. In Europe, PSD2 in particular is accelerating both the entry of new providers into the value chain and enabling all third party providers (TPPs) to deliver value-adding product enhancements. There were 106 TPPs in Europe leveraging PSD2 to offer services to SMEs at the end of Q1 2020. Across these providers there are 10 distinct value propositions being offered, which can be grouped into four categories:

- Incorporating SME account data into TPP services. Multibanking, forecasting and analytics services lead here.

- Lending and credit. Often leveraging open banking to streamline the application process.

- Payments. Enhancing the invoice process and offering easy acceptance of account-to-account transactions.

- Leveraging consumer account data. Use cases include customer onboarding and loyalty services.

Figure 1. Europe's TPP landscape for SME services (not exhaustive)

While this analysis focuses on Europe, the findings and implications are equally applicable to SME banking in most major markets. Celent recommends three strategic responses for financial institutions.

- Forming partnerships with innovative or otherwise wide-reaching TPPs is the most obvious and immediate path for financial institutions wishing to expand the reach of their service offerings.

- Leveraging open banking to directly enhance the core SME banking proposition. As a minimum, financial institutions should look to offer multibanking and forecasting services alongside enhanced invoice functionality and propositions that enable SMEs to accept account-to-account payments from customers.

- Banks should invest in the opportunities of embedded finance. Introducing SME customers to partner TPPs and ensuring a smooth onboarding and service experience can help to maintain and strengthen the customer relationship, while also retaining some influence over the TPPs that customers interact with.