If you’re not failing, you’re not innovating enough

Elon Musk once said “Failure is an option here. If you’re not failing, you’re not innovating enough".

When I reflect on our work here at Celent, and the view it affords across the industry – and despite nearly a decade of insurtech and fintech investment – life carriers have quite simply played things too safely. A recent paper from our team explores one aspect of this: The Slow Automation of Life Insurance New Business. With more than a year since the start of an existential impact (possibly the biggest exogenous shock since the inception of the business), where has there been failure where innovation has been cited as the root cause? Not failing due to conservatism is failing for the wrong reason – this is a glide-path to obsolescence echoing the recent sentiment we’ve heard from one of our Research Panel members “If you are not adapting, you are in the business of going out of business.”

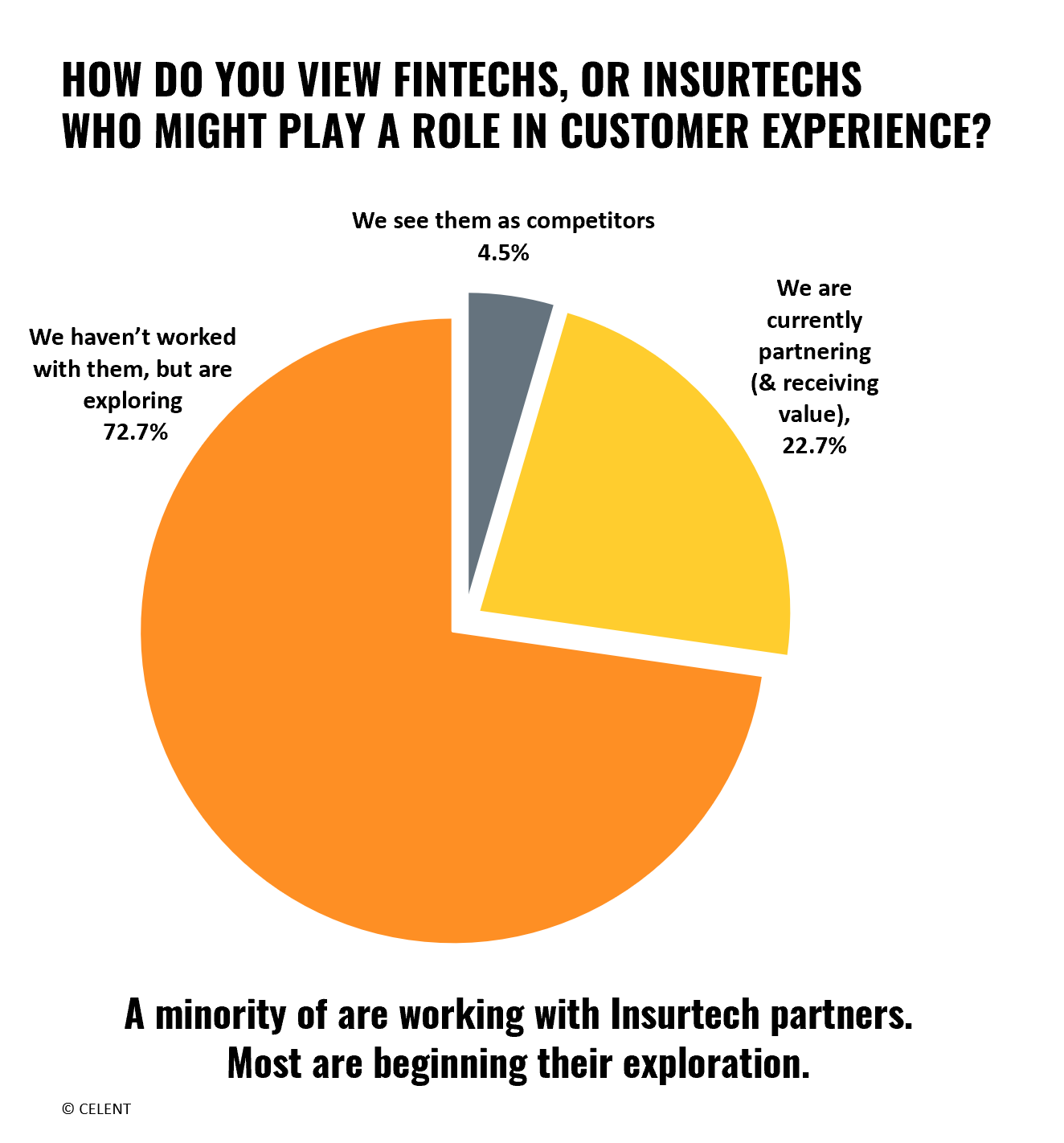

Celent are no strangers to this challenge. In 2017, we wrote “Why Are There No Drones in Life Insurance”, while more recently, we’ve continued our focus: Innovation Is Dead - Long Live Innovation!. We’ve also recently conducted snap-polls on the topic of innovation and the customer’s experience: Life Insurance Customer Experience – in which we asked “How do you view fintech or insurtech (as partners or contributors) who might play a role in customer experience?” The large-majority response was “Nothing yet, but exploring” with a minority who view them as competitors.

This result feels problematic to me. Insurtech investment, as a proxy for innovation and disruption, is an order of magnitude greater than any one firm’s allocation to transformation (just Google 'Insurtech investment' and you can quickly get the picture). Do we see enough engagement with partners to tap into the innovation happening “outside the four walls” of an insurer’s purview? Life carriers must do more through a combination of targeted internal investment and external engagement.

OK, I will make a few concessions – recently, the Life industry has had a maniacal focus on “digital transformation”, but the citations are often examples of value-chain optimization (for straight through processing, improved underwriting, portals, etc.) And I admit that there is great value to be earned through incrementalism – however, compared to what’s been going on in auto and usage-based insurance (not to mention innovations outside of insurance), it’s not much to brag about. Finally, I understand that the past year has been a driver for unexpectedly higher life insurance sales. But the industry’s tag line shouldn’t be “When you’re frightened enough, give us a call – we are ready – we’ve spruced up our business model.”

As a means to manage innovation, “Failure is an option here”. How will Celent help? Please watch this space, my next report Catching Up In Life On The Digital Continuum, will provide insights.