Life Insurance Research Outlook 2024

2024 RESEARCH THEMES

As we move into the final quarter of 2024 the key topics identified by Celent for this year continue to resonate and direct the attention of life and health insurers.

The art of possible and the demand for growth with efficiency encourages insurers to embrace key areas such as data and AI, reshaping the distribution, application of smart automation, taking advatage of innovation, insurtech, and emerging technologies, and imrpoving the core systems critical for supporting insurers' operations.

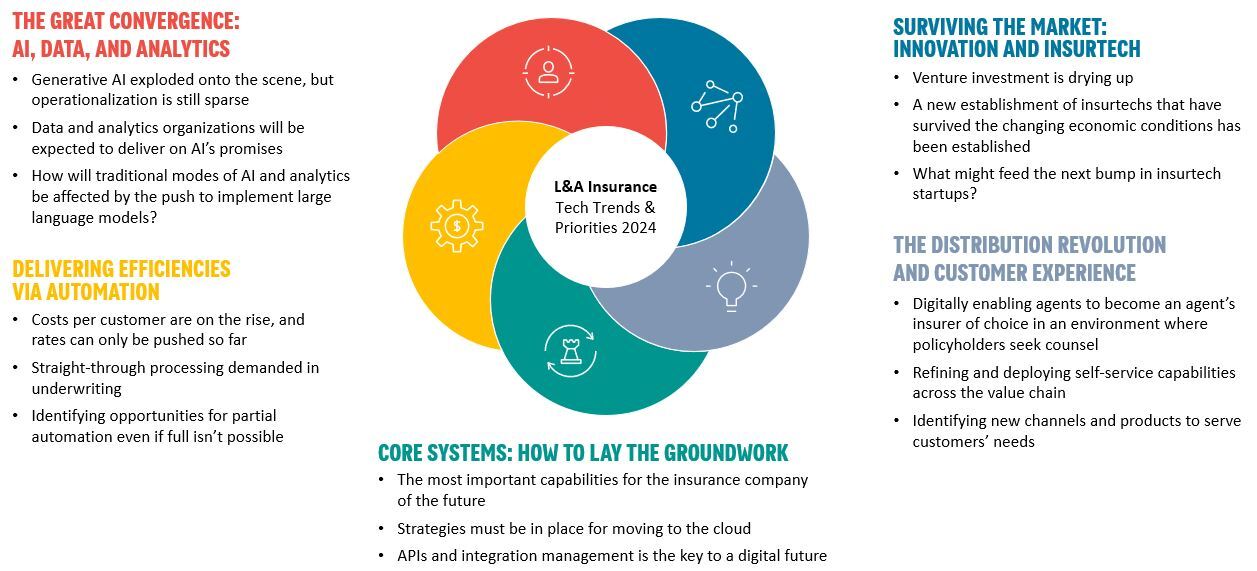

The availability of vast amounts of data and the rise of artificial intelligence (AI) have revolutionized the life and health insurance industry. Insurers now have access to a wealth of information, ranging from medical records to lifestyle data, enabling them to gain deeper insights into customer risk profiles, underwriting processes, and claims management. However, there are challenges and opportunities associated with leveraging data and AI in life and health insurance, including data privacy and security concerns, ethical considerations, and the development of AI-driven underwriting and claims processes. AI also has the opportunity of enhancing the customer experience, personalize insurance products, and improve risk management and health outcomes.

Distribution is being reshaped with higher doses of digital customer engagement, direct-to-consumer distribution strategies, and the evolving role of intermediaries. Insurers need to up their game as they reimagine the new digital distributor.

The potential of smart automation in life and health insurance is broad, covering opportunitis of automation in areas such as underwriting, policy administration, claims processing, and customer service. The integration of automation technologies with data and AI can create intelligent and adaptive insurance processes that enhance customer experience and improve health outcomes.

Innovation and insurtech are shaping the future of life and health insurance in areas such as digital health solutions, telemedicine, digital engagement with clients and agents, and the integration of insurtech solutions into traditional insurance operations. Emerging technologies such as wearables, genetic testing, blockchain, and advanced analytics are reshaping the life and health insurance landscape with potential impact on risk assessment, underwriting, claims management, fraud detection, and customer engagement. However, there are challenges for implementing and integrating these technologies into insurers' core systems, such as legacy system modernization, data interoperability, and cybersecurity considerations, along with regulatory and ethical implications of adopting emerging technologies in life and health insurance to ensure privacy, security, and fairness.

Efficient core systems are vital for supporting life and health insurers' day-to-day operations. Keeping up to date on what’s important in core and non-core insurance systems is a must for insurers to avoid piling up technical debt. Modern systems are incorporating AI, new and better use of data, and increased levels of automation and integration, to better support the business and build ecosystems that provide value to their clients and partners.

The areas of research that we’re working on for this quarter are critical areas that we suggest insurers consider to optimize the value of their technology investments.

Contact us for more information about what we have planned in Q4.

If you are a client, please sign in to access a detailed view of our 2024 agenda.