For starters, nothing in this blog post should be misconstrued to defend digital inaction; quite the contrary. Many banks should double down on digital transformation efforts. In a previous blog, I admonished banks to pursue a simple — yet paradoxically difficult objective. That is, to do whatever it takes to deliver excellent customer service across all points of customer interaction, including the branch network. Strangely, some find this controversial.

Remember: transactions and engagement are two different things.

Few would find it controversial to suggest that banks are over reliant on the branch network for sales. From our research, most US banks attribute well over 70% of sales to the branch. Standing up competitive digital origination capability therefore, is a high priority for many banks – for good reason. Don’t delay! There are multiple, cloud-based platforms you can stand up quickly and inexpensively. With some fine-tuning, you can garner a terrific ROI.

But, talk to some industry influencers and you’d think that once you do, no customer in their right mind would ever darken the lobby of one of your branches ever again. Really? Said another way, what expectations should you have for digital customer origination in the short term? Will digital origination (online + mobile) grow to 30% of sales? 40%? 60%? The answer depends - at least in part - on your bank's market. For this discussion, let's focus on the US.

The largest U.S. banks attribute between 25% and 30% of new account sales to the digital channels. Importantly, these results followed significant investments in digital customer origination capability and dedicated branch staff effort focused on customer digital activation and lead management/follow-through. Most smaller financial institutions are nowhere close to this mix. Does 30% define a near-term high water mark? Said another way, are branches destined to remain the dominant source of new customer origination for most banks in the near-term - despite massive industrywide investments in digital customer origination?

What Consumers Say

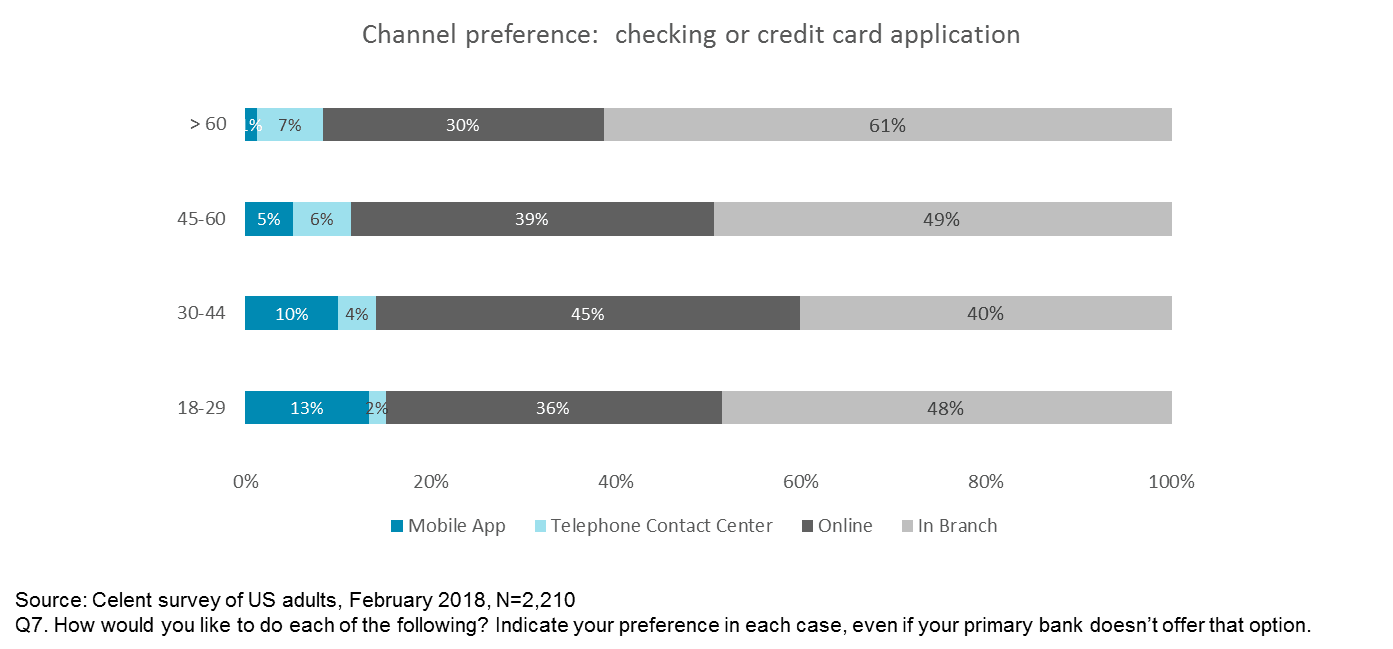

Earlier this year, Celent fielded two consecutive surveys designed to understand when and how consumers prefer to interact with their banks in-person. Yes, consumers still do that. One of the survey questions was, “How would you like to do each of the following? Indicate your preference in each case even if your primary bank doesn’t offer that option.” We then offered a number of things, such as disputing a charge, applying for a new account, etc. Here’s what we found specifically related to new checking and credit card accounts broken out by age. Roughly half of U.S. banked adults prefer opening new accounts in the branch. About a third preferred online. About ten percent preferred mobile.

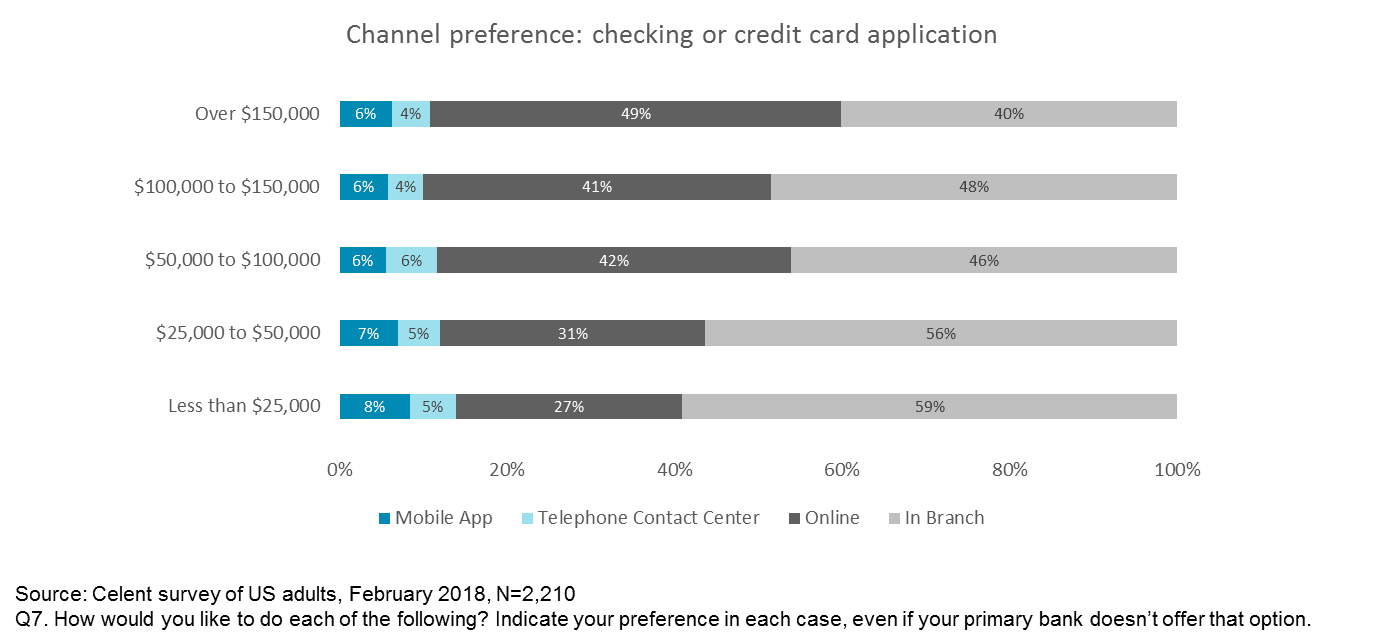

When viewed by annual income, it is the highest income earners that show the greatest preference for digital (mostly online) origination

Based on this view, banks could reasonably expect to attain up to ~40% of sales of some products digitally (depending on the bank’s target market). Achieving this would require a number of things to be done exceptionally well. Among them:

- A reasonably frictionless user experience

- Thorough integration with marketing programs

- A seamless way for prospects to get questions answered in-process

- Digital appointment booking for prospects wanting face-to-face engagement

- Rigorous follow-up of abandoned carts

- Omnichannel save-and-resume capability

- Proper attribution when other channels are involved

Could banks exceed this in time? Sure, but I am aware of no US mass market bank with results this compelling today.

Why is it hard for some to accept that a percentage of consumers want face-to-face interaction before making a purchase decision having consequential financial impact? Let me offer a personal anecdote to help you.

The Meara household is embarking on a major kitchen remodelling project. Our old kitchen is now in a dumpster (yes, it's stupid...). Anyone who has done something like this knows there are many decisions to make along the way. Key among them is choosing a contractor. To do so, I relied heavily on digital mechanisms. Specifically, I:

- Searched for prospective contractors digitally

- Reached out to potential contractors and customer references digitally

- Arranged appointments digitally

- Received and negotiated proposals digitally

But before making such an important purchase, I wanted to meet the contractor face-to-face. I had to be comfortable about the decision and in-person engagement helped me get there. Don’t be surprized when your customers (and prospective customers) feel similarly.

An infographic summarizing Celent’s consumer research is available here. Clicking the link will download a PDF. The first of two published reports is available to clients here.