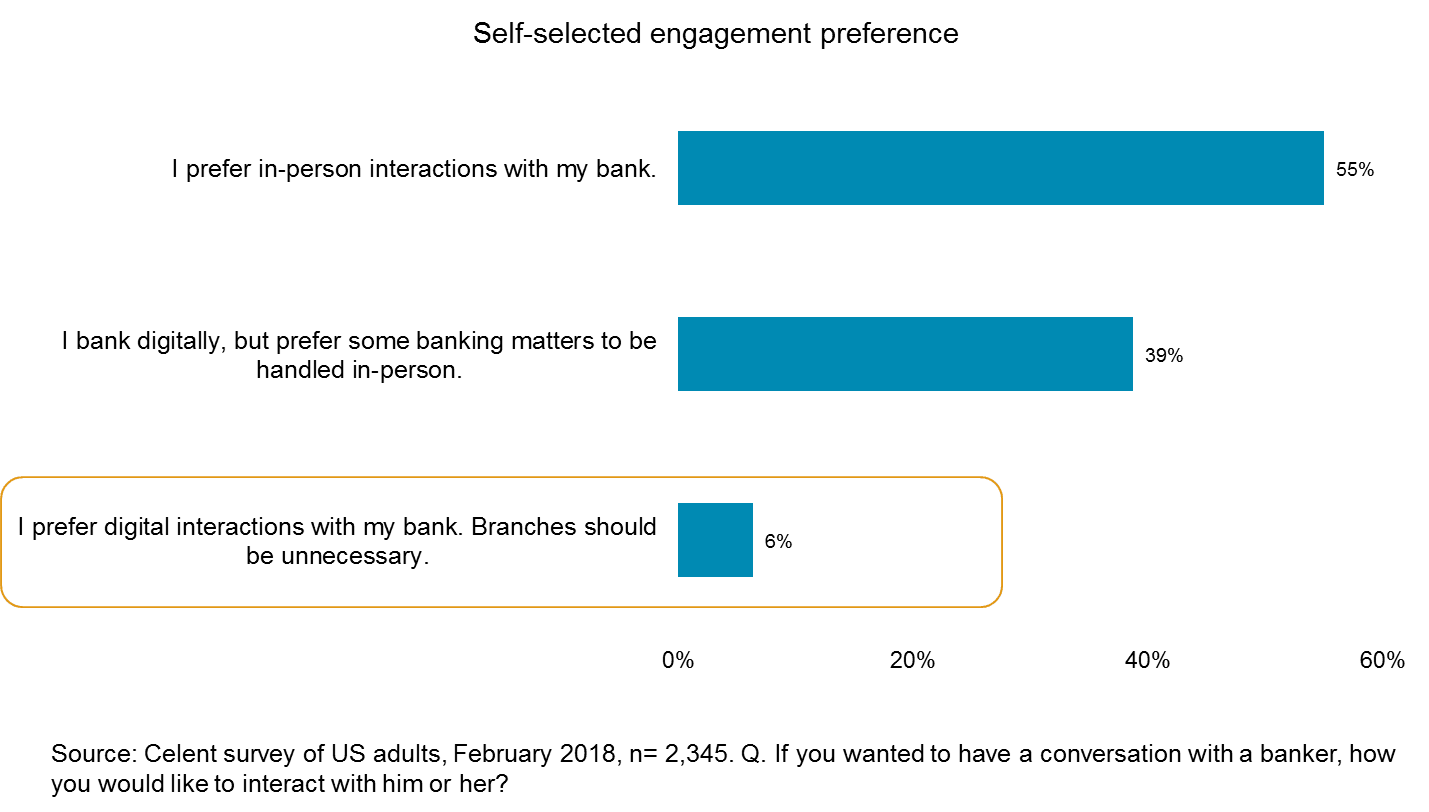

Six percent. Remember that number.

In our research, we’ve seen digital - partially mobile initiatives get higher priority in institutions, while branch and contact center investments play second fiddle to digital. Is this a good thing? Be careful before you answer.

Digital advocates point to undeniable growth in channel utilization and a corresponding decline in branch footfall. Undeniably true. But, those metrics are transaction driven. From our research, transactions and customer engagement are two different things. And, if our assessments are overly influenced by transactions, we are at great risk of blowing it.

Some point to growth in the use of social media and video chat, for example, as evidence for the branch channel’s irrelevance. They’re wrong. The fact is, consumer’s personal digital habits are a poor predictor of their preference for interacting with their bank – today.

Celent conducted research among US banked adults in February to understand when and how consumers prefer to engage and what it means for banks. We found that just six percent of adults prefer a fully digital banking experience - when both transactions and engagement are considered.

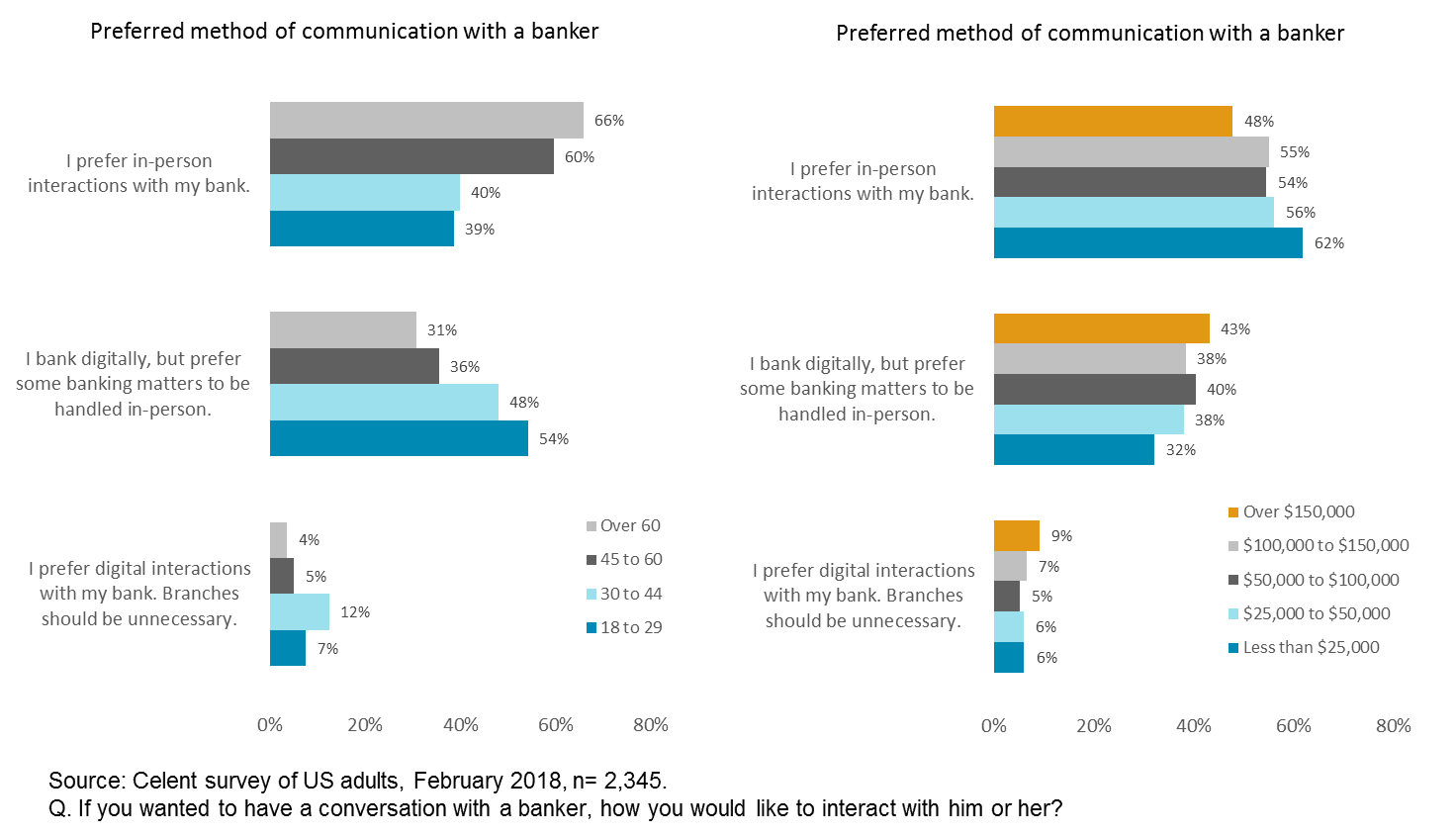

Hard to believe? It shouldn't be. If the questions asked about how consumers want to move money, make deposits or pay bills (common digital transaction activity) answers would have been very different. Of course, preferences vary by age and income, as most would expect – but not dramatically so. Take a look:

If digital engagement (not transaction execution) was such a no-brainer, why are so many banks training branch personnel to coach consumers to use the bank’s digital capabilities?

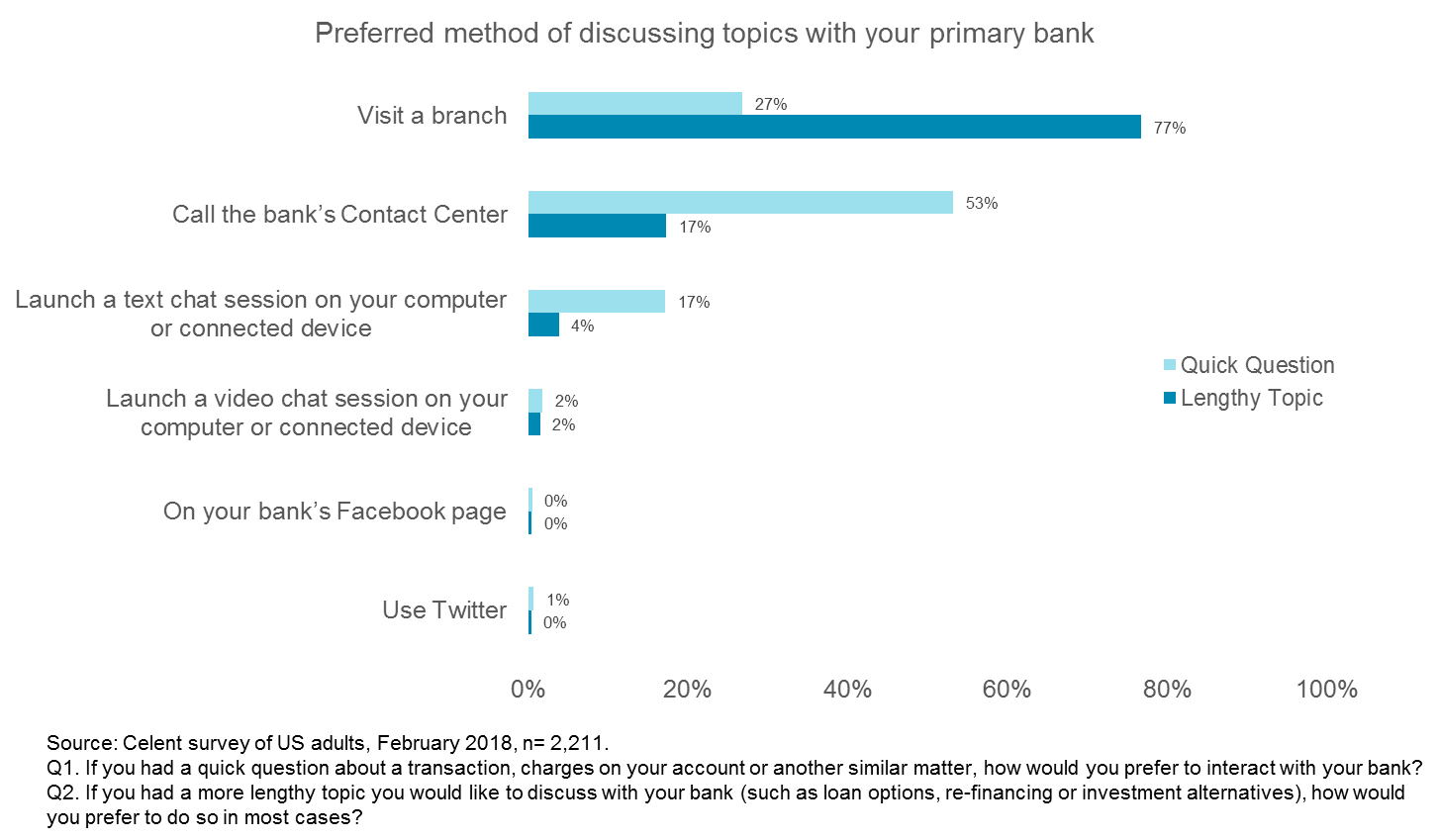

In a separate question, when asked how they would prefer to interact with their bank to answer quick questions, virtually no one chose text, chat, video chat or social media. Instead, across all age and income segments, if offered a choice, most consumers prefer to pick up the phone or drop by the branch. Are you kidding? Transactions and engagement are different things.

For more substantive conversations, such as mortgage, auto loan or even checking account options or origination, the majority of customers prefer to engage their bankers face-to-face in a branch. This is precisely why branches will remain strategically important to financial institutions

It gets better. When asked what sorts of poor experiences would make consumers likely to switch banks, for most adults (particularly high income earners) it is a poor branch experience.

Digital matters - a lot! So does the branch experience. Institutions neglect either of them at their peril. How much and how quickly this will change is anyone’s guess. In the meantime, don’t fall for the hype promulgated by those trying to sell you something.

An infographic summarizing Celent’s consumer research is available here. Clicking the link will download a PDF. The first of two published reports is available to clients here.