Our parent firm, Oliver Wyman (OW), is closely monitoring COVID-19 events in real-time and has compiled resources to help clients and the industries they serve. For financial services firms, OW experts has published their perspectives on topics ranging from liquidity management to risk functions.

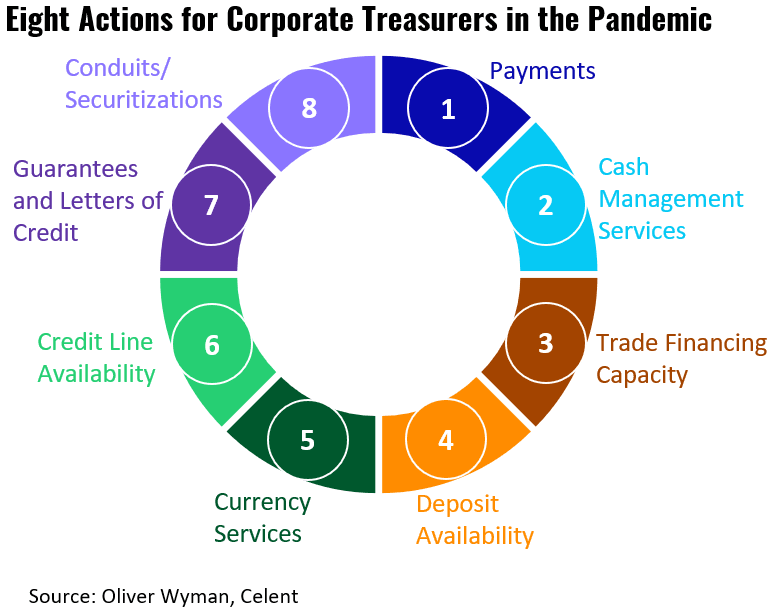

OW's most recent publication is "Oliver Wyman: Eight Actions for Corporate Treasurers in the Pandemic." At a high level, the firm recommends that treasurers remain in close contact with bank providers across a range of topics including payments, credit-line availability, and cash management, while monitoring market indicators of the financial strength of key relationship banks. In particular, corporate treasures should consider these eight actions:

- Payments: Monitor payment activities to ensure banks’ attempts to manage intraday liquidity through throttling of payments do not impact time-sensitive obligations (nor other payments for that matter).

- Cash-management services: Review and confirm that any cash sweeps/investments are being made to sufficiently conservative investment instruments.

- Trade financing capacity: Make certain banks have provided a critical role in facilitating global trade through the provisions of trade financing services, such as documentary letters of credit and import/export bills.

- Deposit availability: Treasurers have traditionally utilized banks as points at which to aggregate surplus cash on both a short term as well as longer-term basis. As COVID-19 impacts revenue and cash generation across sectors, the availability of those deposits needs to be continuously confirmed.

- Currency services: Some corporates rely on their “relationship banks” as a source of currency payments – the unimpeded availability of currency needs to be assured at reasonable rates. This may also raise the question of reviewing currency-hedging strategies.

- Credit line availability: Committed credit and liquidity facilities are a key mainstay of banks’ service offerings. As mentioned above, banks’ liquidity positions have been materially enhanced through post-financial-crisis regulations, and that, coupled with central bank aggressive support, should make drawing on facilities simply to “hoard cash” an expensive proposition that is not worth it.

- Guarantees and Letters of Credit: The availability of these should continue uninterrupted. Monitoring for any indications of capacity reductions or increased pricing should be in place.

- Conduits/Securitizations: Banks facilitate the asset financing needs of corporates through a number of key roles, such as sponsor of single or multi-seller conduits, participation in conduit-liquidity facilities, or underwriting securitization transactions. Corporate treasurers need to stay informed on the conditions of financing markets for maturing conduit-issued commercial paper. Any disruption in financing markets may result in corporate treasurers having to seek alternative financing sources for their assets. Similarly, should a bank sponsor suffer a ratings downgrade, that could impede its ability to continue in its role as a conduit sponsor, resulting in potential loss of financing capacity for corporate assets.

As a prudent measure, corporate treasurers should also monitor market measures, which may provide indications of deteriorating financial strength of key relationship banks. Indicators could include, for example, a widening in credit spreads or in credit-default swaps that is not correlated with those of other comparable financial institutions and rating agency announcements related to financial outlook changes or credit downgrades.