Amid the coronavirus pandemic, financial institutions are still figuring out the implications for their bottom line technology spend. While it is all but certain that budgets will be trending downwards, certain technology areas may see their renaissance period. Over the course of the last few weeks, many technology vendors have been asking Celent how this will affect their success, questioning whether they should maintain the current model, re-examine their future strategy, or completely reinvent themselves. Over the course of the next 2-months, the Wealth Management team aims to investigate this pressing question by looking at CIO outlook on technology spending in financial services, as well as incorporating client feedback.

While the analysis is underway, we can still theorize how human behavior is fundamentally changing, thus providing a better understanding of which technology areas are likely to succeed in this new paradigm.

Hybrid Advice Models: More collaborative than ever before

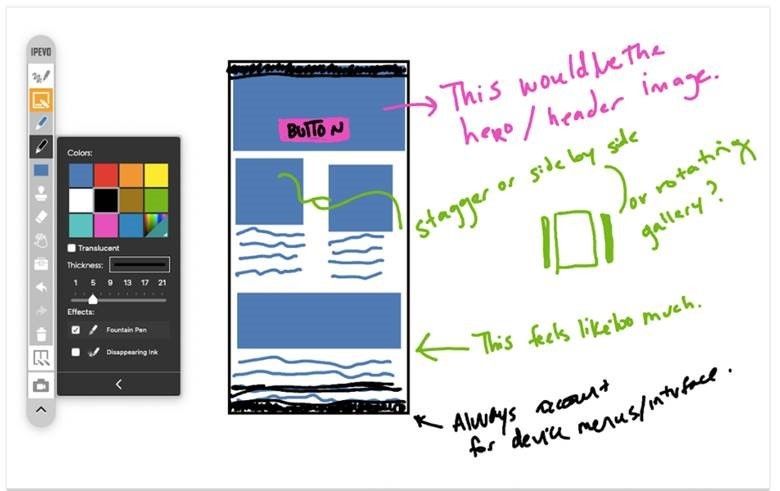

As clients become more accustomed to new methods of digital collaboration, wealth managers must swiftly adapt and focus on more than just enabling remote work. They now need to go a step further and invest in better collaboration tools. Microsoft recently reported a 2X increase in employees working and learning through video, with big surges in demand for video streaming as well. While demand for video conferencing might decline when this pandemic ends, the client’s desire to find more dynamic ways to share information will not. Digital whiteboarding tools, where clients and advisors take turns collaborating and making live annotations to information shared, may be the part of the answer.

See Hybrid Digital Advice: Pathway to Personalization at Scale

Self-Serve Migration: Low touch and low quality, no longer perceived synonymously

Historically, the degree of self-service shares a negative correlation with client wealth. The wealthier the client, the more personal the service the tended to receive. Yet this pandemic was completely impartial, forcing even wealthier clients to adapt to remote working styles via digital collaboration.

Virtual Assistant can be a great way to quickly deliver answers to general client inquiries, especially in emergency situations where a high volume of clients will be asking similar FAQs. However, it is critically important to ensure these tools have been sufficiently trained to escalate complex or urgent inquiries to human advisors. Additionally, financial institutions shouldn’t shy away from moving their clients to cloud infrastructure to enable automated, more seamless workflows.

See Calling All AI: Automating the Contact Center Environment, and An Introduction to Voice-First Investing: Key Steps to Harnessing its Potential

In light of this pandemic, many clients have been forced to think about end-of-life planning. Yet, social distancing norms have made it increasingly difficult coordinating with advisors and estate planners to submit estate related documentation and identify beneficiaries. As a result, financial institutions have started to think about the concept of digital estate planning which gives clients access to a digital vault that enables them to upload their estate information themselves. The program also gives the advisors unique collaboration tools so they can digitally support clients throughout the entirety of the estate planning lifecycle (e.g. overseeing their digital vault, pushing missing legal documentation that still needs to be completed, etc).

See Digital Estate Planning: COVID Proofing your Estate

Digital Engagement: The streets are silent, but you shouldn’t be

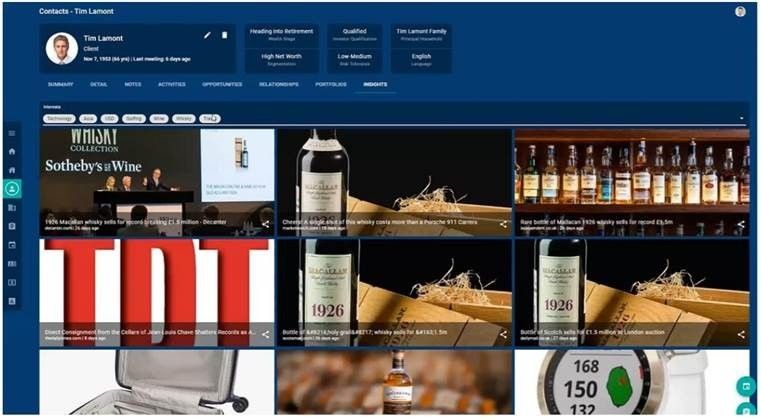

With limited human interaction and generally more free time, clients are now looking for new ways to consume information. Advisors should consider exploring content marketing as a unique way to deliver news to their clients. This strategy offers a subtle way of keeping them engaged when physical meetings and industry/company events have been cancelled. However, this idea is not novel and it’s safe to assume many clients have been bombarded with ads and contextual marketing material. The winners of this strategy will be those that are able to deliver content that is not only personalized but also of high quality. For instance, AdvisorStream enables advisors to push premium licensed content to its clients which was previously inaccessible as it was positioned behind a paywall from publishers.

Next Best Action recommendation tools are also useful in understanding client preferences as well helping advisors engage their clients on channels that best suit them. NexJ’s CRM also offers this capability and alerts advisors to content that is tailored to their client’s interests.

See my report The Next Best Action: Using Machine Learning to Anticipate Client Needs

There’s a very strong chance that global financial services technology spending will see a decline in 2020, even under best case world economic and health scenarios. However, financial institutions can use this as an opportunity to refocus their spending onto technology areas that are more likely to promise ROI. Technologies that are nascent or considered even somewhat experimental may begin to see a trough as financial institutions focus more on their core business and exploring more directly related technologies. Perhaps COVID-19 is the great accelerator for technologies that were always doomed to fail, or maybe it’s just a temporary filter. Only time will tell.