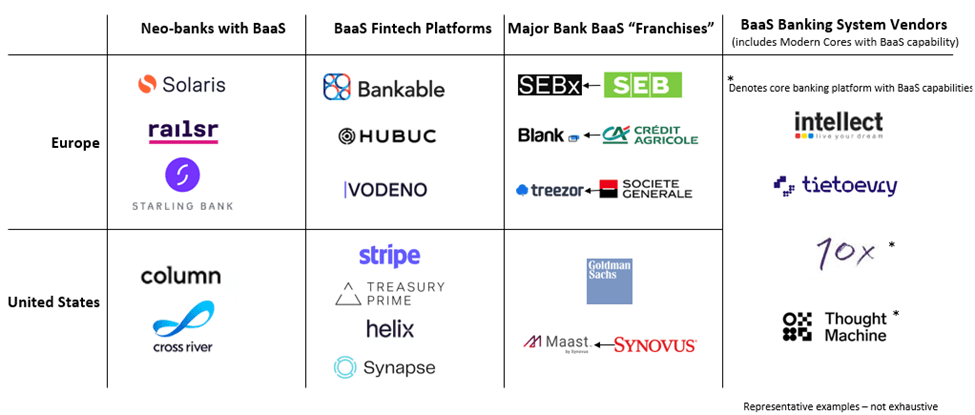

Although the UK Open Banking and European Union PSD2 legislation had specific goals to open up consumer financial services, it also paved the way for new global ecosystems and business models, enabled by open data and open APIs. In effect, Open Banking and PSD2 legislation gave rise to what we now globally call Banking as a Service (BaaS), enabling embedded finance and fostering a broader ecosystem of market participants. Celent sees increasingly exotic partnerships between banks and fintechs, but also between BaaS fintech platforms and more traditional application vendors of ERP solutions and core banking systems. Many of these new developments and partnerships focus on enabling not just B2B (business to business) banking, but B2B2B and B2B2B2C. In 2023, Celent anticipates more banks looking for opportunities to drive influential partnerships that help them engage more directly with their corporate and business banking clients.

Banks need to adopt a “partnership mindset” more so than their traditional approaches to vendor management. A partnership should be worth more than the sum of its parts, and be aligned along cultural fit, strategic direction, and technology. Regulators are also paying much closer attention to bank-fintech partnerships to ensure that banks manage partners responsibly, hold them accountable, and not take on undue risk as they seek growth opportunities. There are opportunities for new adventures in the corporate banking ecosystem, and new partnerships to forge. However, banks and fintechs must be clear about the reasons, rewards, and risks.