Paying banks to take your money -- huh?

24 July 2015

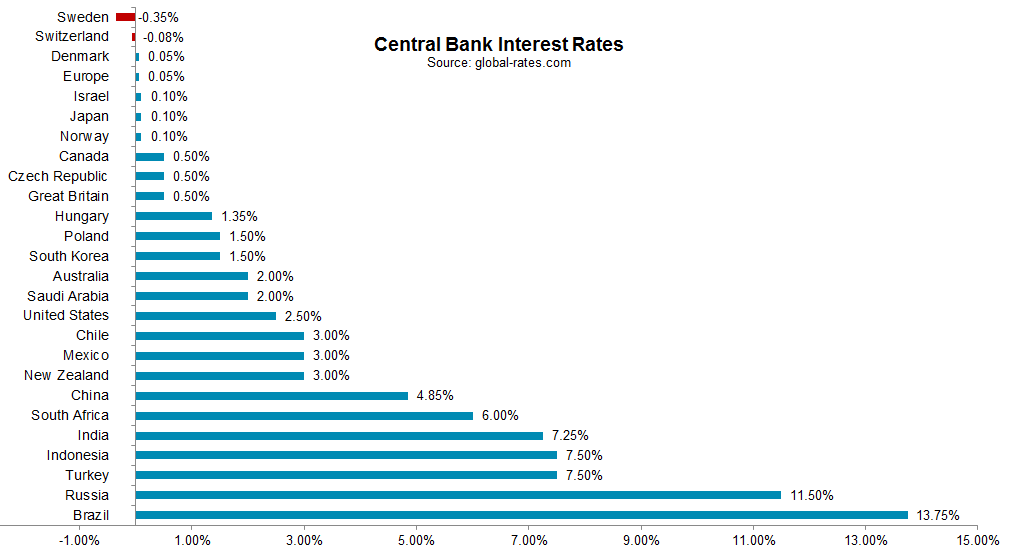

Corporations have historically parked excess cash in their demand deposit accounts to take advantage of earnings credit allowances. Each month, the bank calculates the earnings allowance for a client’s accounts by applying an earnings credit rate to available balances. The earnings allowance is then used to offset the cost of cash management services. In the United States, corporates got the option of earning interest in money market accounts with the repeal of Req Q by Dodd Frank. The Liquidity Coverage Ratio (LCR) provisions of Basel III and the advent of negative interest rates in some European countries are upending traditional cash flow management for banks and their corporate and institutional clients. The LCR requires large and internationally active banks to meet standard liquidity requirements. It makes assumptions for deposit runoff in times of financial stress, resulting in a liquidity squeeze. Banks must hold enough high quality, liquid assets (HQLA) to fund their operations during a 30-day stress period. Examples of high quality assets include central bank reserves and government and corporate bond debt. The phase-in of the LCR started on January 1, 2015. It requires banks to distinguish between two types of short-term (30 days or less) deposits. Operational deposits include working capital and cash held for transactional purposes. Non-operational balances are other cash balances not immediately required and assumed to be investments; such as short-term time deposits with a maturity of 30 days or less and accounts with transaction limitations, such as money market deposit accounts. Non-operating/excess balances are assigned a 40% runoff rate for corporations and government entities and 100% for financial institutions, making them the least valuable to banks. As a result, corporates with non-operational cash investments may find it difficult to place in overnight investment vehicles. Many banks are reducing their non-operating deposits either by encouraging corporates to place their funds elsewhere, or by creating new investment products such as 31+ day CDs, money market funds and repurchase agreements to avoid the LCR charge on excess balances. Similarly, corporates also face a risk of higher costs for committed lines of credit which also require more Basel III capital to be held by banks. Bank demand for HQLA in the form of central bank reserves along with European fiscal policy has pushed central bank interest rates into negative territory for the safest monetary havens (Sweden and Switzerland). In other countries with central bank rates hovering near zero, once you take the inflation rate into consideration, those rates are negative as well (ECB and Denmark).  Central banks had hoped that negative interest rates would encourage commercial banks to increase lending, but there’s only been a slight increase in outstanding loan balances. Financial institution clients are hardest hit by central bank negative interest rates, particularly deposits in Euros, Swiss francs, Danish crowns and Swedish crowns. Many global banks are charging “balance sheet utilization fees” or other deposit fees. For corporate clients, savvy banks are taking a collaborative approach—working with corporate treasurers to educate them on the impact of regulatory and economic forces on their cash management and investment decisions and advising them on the available options.

Central banks had hoped that negative interest rates would encourage commercial banks to increase lending, but there’s only been a slight increase in outstanding loan balances. Financial institution clients are hardest hit by central bank negative interest rates, particularly deposits in Euros, Swiss francs, Danish crowns and Swedish crowns. Many global banks are charging “balance sheet utilization fees” or other deposit fees. For corporate clients, savvy banks are taking a collaborative approach—working with corporate treasurers to educate them on the impact of regulatory and economic forces on their cash management and investment decisions and advising them on the available options.

Central banks had hoped that negative interest rates would encourage commercial banks to increase lending, but there’s only been a slight increase in outstanding loan balances. Financial institution clients are hardest hit by central bank negative interest rates, particularly deposits in Euros, Swiss francs, Danish crowns and Swedish crowns. Many global banks are charging “balance sheet utilization fees” or other deposit fees. For corporate clients, savvy banks are taking a collaborative approach—working with corporate treasurers to educate them on the impact of regulatory and economic forces on their cash management and investment decisions and advising them on the available options.

Central banks had hoped that negative interest rates would encourage commercial banks to increase lending, but there’s only been a slight increase in outstanding loan balances. Financial institution clients are hardest hit by central bank negative interest rates, particularly deposits in Euros, Swiss francs, Danish crowns and Swedish crowns. Many global banks are charging “balance sheet utilization fees” or other deposit fees. For corporate clients, savvy banks are taking a collaborative approach—working with corporate treasurers to educate them on the impact of regulatory and economic forces on their cash management and investment decisions and advising them on the available options.