ACH: The Glory Days may be Over

10 June 2009

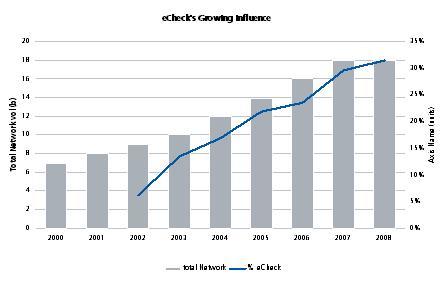

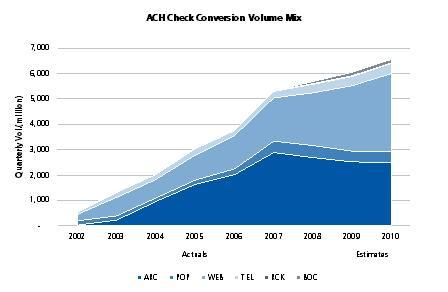

NACHA and the ACH have been on a roll for most of the decade, posting impressive network transaction growth rates year after year. From 2000 through 2008, total ACH volume (network + off-network) has almost tripled from 6.9 billion to 18 billion transactions. But from our perspective, the Glory days are nearing an end. This can be seen in the recently released Q1 2009 network volume statistics, with total network volume up just 1.9% versus year ago. Prior to the invention of check conversion SECs (ARC, BOC, POP, RCK, TEL and WEB), the ACH was used almost exclusively for recurring transactions. Indeed, it was designed specifically for this purpose. Network volume was dominated by cash concentration activity and prepaid credits (direct deposit of pay checks) and debits (recurring bill payments). But after years of promotion, the growth engine slowed to an idle. Then came check conversion, beginning with POP introduced in 1999. The collective check conversion introductions have produced impressive results. Through 2008, check conversion activity accounted for 38% of total network volume (32% of total ACH volume), up from just 6% in 2002. [caption id="attachment_591" align="aligncenter" width="448" caption="Check Conversion has Rapidly Become a Significant ACH Contributor"] [/caption] For the multiplicity of eCheck SECs, the vast majority of check conversion volume has come from ARC and WEB. ARC was adopted by a significant number of large billers and retail lockbox operators because, at the time, ARC offered compelling savings versus paper check clearing methods. WEB has been propelled by PayPal transaction activity, with significant growth over the past two years in particular. [caption id="attachment_592" align="aligncenter" width="448" caption="ARC and WEB Dominate eCheck Volume"]

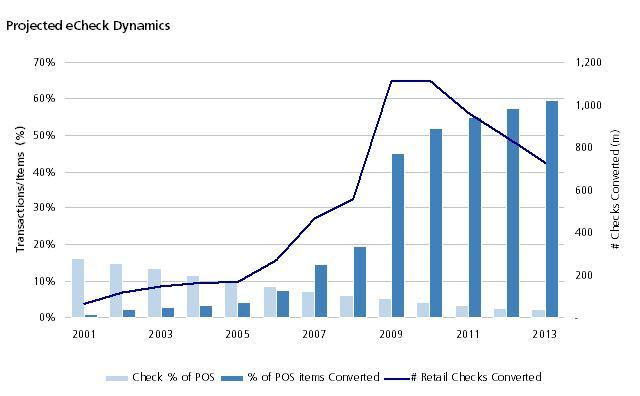

[/caption] For the multiplicity of eCheck SECs, the vast majority of check conversion volume has come from ARC and WEB. ARC was adopted by a significant number of large billers and retail lockbox operators because, at the time, ARC offered compelling savings versus paper check clearing methods. WEB has been propelled by PayPal transaction activity, with significant growth over the past two years in particular. [caption id="attachment_592" align="aligncenter" width="448" caption="ARC and WEB Dominate eCheck Volume"] [/caption] But, what lies ahead for check conversion? We see growth, but a far cry from the glory days gone by. In large measure, this is a direct result of the inexorable decline in consumer check writing. There are at least two additional factors. • Electronic bill pay will likely continue to grow at 5% to 7% annually for the next few years, but a good portion of that growth will cannibalize ARC volume as electronic initiated payments displace ARC conversions of mailed remittance. • Even though POP and BOC will see continued adoption by retailers, the resulting ACH volume will be unimpressive. [caption id="attachment_593" align="aligncenter" width="640" caption="POS eCheck Volume will Decline Amidst Continued Retailer Adoption"]

[/caption] But, what lies ahead for check conversion? We see growth, but a far cry from the glory days gone by. In large measure, this is a direct result of the inexorable decline in consumer check writing. There are at least two additional factors. • Electronic bill pay will likely continue to grow at 5% to 7% annually for the next few years, but a good portion of that growth will cannibalize ARC volume as electronic initiated payments displace ARC conversions of mailed remittance. • Even though POP and BOC will see continued adoption by retailers, the resulting ACH volume will be unimpressive. [caption id="attachment_593" align="aligncenter" width="640" caption="POS eCheck Volume will Decline Amidst Continued Retailer Adoption"] [/caption] This likely outcome is perhaps why NACHA and the network operators have begun merchandizing same-day ACH. We provided a position on that initiative in an earlier post, Same-Day ACH: Whose Interests Would be Served?

[/caption] This likely outcome is perhaps why NACHA and the network operators have begun merchandizing same-day ACH. We provided a position on that initiative in an earlier post, Same-Day ACH: Whose Interests Would be Served?

[/caption] For the multiplicity of eCheck SECs, the vast majority of check conversion volume has come from ARC and WEB. ARC was adopted by a significant number of large billers and retail lockbox operators because, at the time, ARC offered compelling savings versus paper check clearing methods. WEB has been propelled by PayPal transaction activity, with significant growth over the past two years in particular. [caption id="attachment_592" align="aligncenter" width="448" caption="ARC and WEB Dominate eCheck Volume"][/caption] But, what lies ahead for check conversion? We see growth, but a far cry from the glory days gone by. In large measure, this is a direct result of the inexorable decline in consumer check writing. There are at least two additional factors. • Electronic bill pay will likely continue to grow at 5% to 7% annually for the next few years, but a good portion of that growth will cannibalize ARC volume as electronic initiated payments displace ARC conversions of mailed remittance. • Even though POP and BOC will see continued adoption by retailers, the resulting ACH volume will be unimpressive. [caption id="attachment_593" align="aligncenter" width="640" caption="POS eCheck Volume will Decline Amidst Continued Retailer Adoption"][/caption] This likely outcome is perhaps why NACHA and the network operators have begun merchandizing same-day ACH. We provided a position on that initiative in an earlier post, Same-Day ACH: Whose Interests Would be Served?