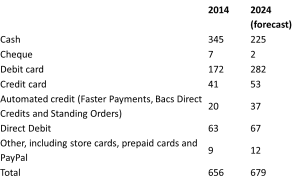

Our friends at PaymentsUK have released their latest forecasts, the ever excellent UK Payments Market 2015. Whilst we don’t have a copy of the full report (hint, hint…), the press release does give us some interesting insights. For example, payments will hit 44 billion transactions a year by 2024. This is a net growth of 3.4 billion, which hides significant and continued declines in both cash and cheque usage (53% to 33%, and 1.1% to 0.4% respectively). The table provided (and replicated below - the link above has a better quality version) shows that, for consumers at least, cards continue to drive the growth. There are obvious reasons for this: consumers switching from Oyster-like cards to contactless, and indeed, contactless generally, is just one good example. Number of annual consumer payments made per adult One thing that really stood out for me is the final line before the total – the “other” category. Celent’s forecasts typically count prepaid and store cards into our debit forecasts. But what is notable is that PayPal is explicitly mentioned… and mobile payments aren’t. At all. We’ve not seen the full report, so it may be explained there, but given what we read in the press, this is hugely surprising. Recent examples include:

One thing that really stood out for me is the final line before the total – the “other” category. Celent’s forecasts typically count prepaid and store cards into our debit forecasts. But what is notable is that PayPal is explicitly mentioned… and mobile payments aren’t. At all. We’ve not seen the full report, so it may be explained there, but given what we read in the press, this is hugely surprising. Recent examples include:

Actually, it’s not surprising. Firstly, what is a mobile payment? That in itself will cause heated debates! Secondly, for the latter to be true, I ought to know at least someone who is making those mobile payments – or rather, every other person I know! I’m being slightly tongue in cheek –

read Zil’s post from a few weeks back about him at least trying. However, I’d still argue that even this wasn’t a true mobile payment – the mobile device is just holding the card credentials. I refer you to my first point!

So what are the takeaways?Firstly, the growth may continue – but in reality is perhaps less strong than you may initially think. A 3.4 billion growth in 10 years is actually only a CAGR of c 0.5% a year. Compared to some developed countries (France for example) that’s good, but compared to some develop

ing countries that’s low.

Secondly, there may be 101 new ways to pay, but they’re unlikely to make significant inroads, instantly. Current methods are deeply embedded in our every day life. Indeed, many of the “new” methods run on top of the existing rails, and the volume often gets counted as the old method. This doesn’t mean that there are no improvements to be made but that they are just that – tweaks to the existing. Finally, perhaps the phrase of there are lies, damn lies and statistics, ought to be caveated that many of the issues seem to be with PR people and journalists. Many inadvertently misread the numbers, but some of the latest releases underline that we all ought to find the original source rather than necessarily solely relying on what’s being reported.

One thing that really stood out for me is the final line before the total – the “other” category. Celent’s forecasts typically count prepaid and store cards into our debit forecasts. But what is notable is that PayPal is explicitly mentioned… and mobile payments aren’t. At all. We’ve not seen the full report, so it may be explained there, but given what we read in the press, this is hugely surprising. Recent examples include:

One thing that really stood out for me is the final line before the total – the “other” category. Celent’s forecasts typically count prepaid and store cards into our debit forecasts. But what is notable is that PayPal is explicitly mentioned… and mobile payments aren’t. At all. We’ve not seen the full report, so it may be explained there, but given what we read in the press, this is hugely surprising. Recent examples include: