Despite largely positive AUM growth, sustained growth in active investment remains elusive due to the onslaught of secular headwind factors and the changing economics across the buy side industry. With a combination of persistent margin pressures, uncertain business conditions, and slowing revenues, investment firms are rethinking or reshaping how they go to market operationally. The mantra today in the quest for transformation continues to be the twin challenge of "front office efficacy" and "back office efficiency", which isn't new, but is now manifesting itself through new waves of change.

In this research, we examine where and how investment managers are forging new tactics in their quest to improve operating economics and efficiencies. At a typical investment firm, personnel-related costs are a relatively large component of the underlying challenges. On average, players are allocating more than 60% of their cost structures to people, while leading firms operate in the low 40s. Therefore, the quest towards stronger middle and back office efficiencies are important pillars for success. Technology advancements around digital, cloud and artificial intelligence have meant that even traditional avenues of driving improvements, such as automation, outsourcing, and systems rationalization, are now given "fresh leases of life" and are poised to underpin new waves of incremental innovation.

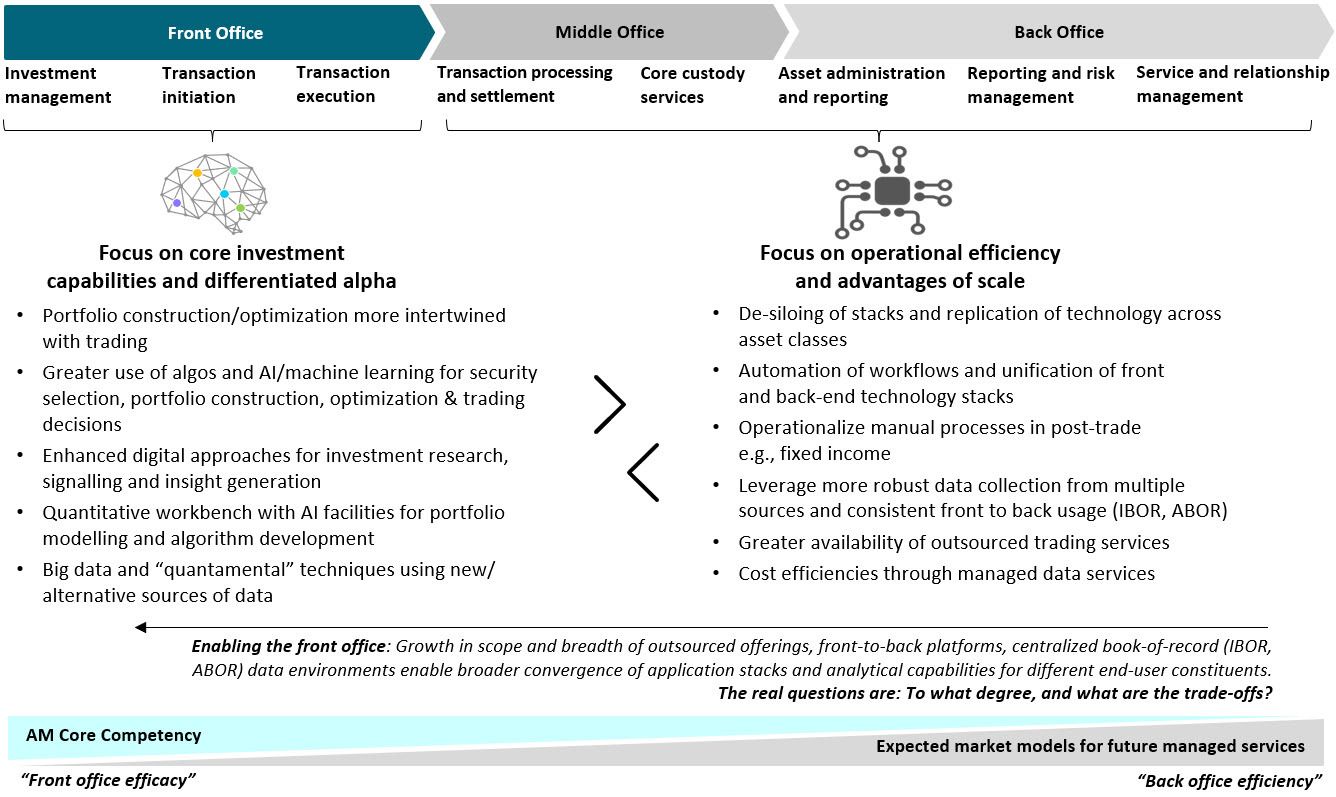

Raising the efficacy of front office capabilities remains core to an asset manager's identity and proposition to they clients. Investment firms are investing and streamlining technology infrastructure to better enable the gathering, mining and generation of insights from data to equip and enable core portfolio functions (research, asset allocation, portfolio construction and optimization), with the strategic intent of creating an alpha advantage.

By the middle of the decade, we anticipate digital approaches and data science techniques will reach a tipping point toward critical mass—enabling investment managers to create impact for the firm around interactions (better workflow and information harmonization), facilitate a more agile approach around investment optimization, and construct more timely and accurate predictive models and forecasts.

Smart analytics will allow more accurate client targeting, increased quality of advice, asset allocation, and portfolio construction through real time financial planning, personalized reporting, and enhanced financial analysis. The adoption of new technologies is also altering the dynamics of how the next-generation “digital native” investors engage with investment firms in their use of automated/ machine-based investing rather than their traditional “hands-off” relationship with active asset managers.

The prospects and opportunities associated with new shifts and business model reconfigurations will mean that investment firms, technology vendors, and solution providers will need to prepare and position themselves in order to win in the years ahead.

To learn more about how investment management firms are upgrading their operations and technologies, please contact Celent for more information on our latest reports on these topics (subscribers can link through to the full reports):

- Operational Alpha on the Buyside: Crystal Balling Future Hybrid Provider Propositions and Ecosystem Innovations

- Operational Alpha on the Buyside: Strategic Levers to Exploit “Ecosystem in a Box” Paradigms

- End-to-end solutions set to revolutionize investment technology

- NextGen Invest and Risk Tech: Gazing Through A Crystal Ball Into 2030

- Embracing NextGen Invest and Risk Tech (Asset Manager Edition)