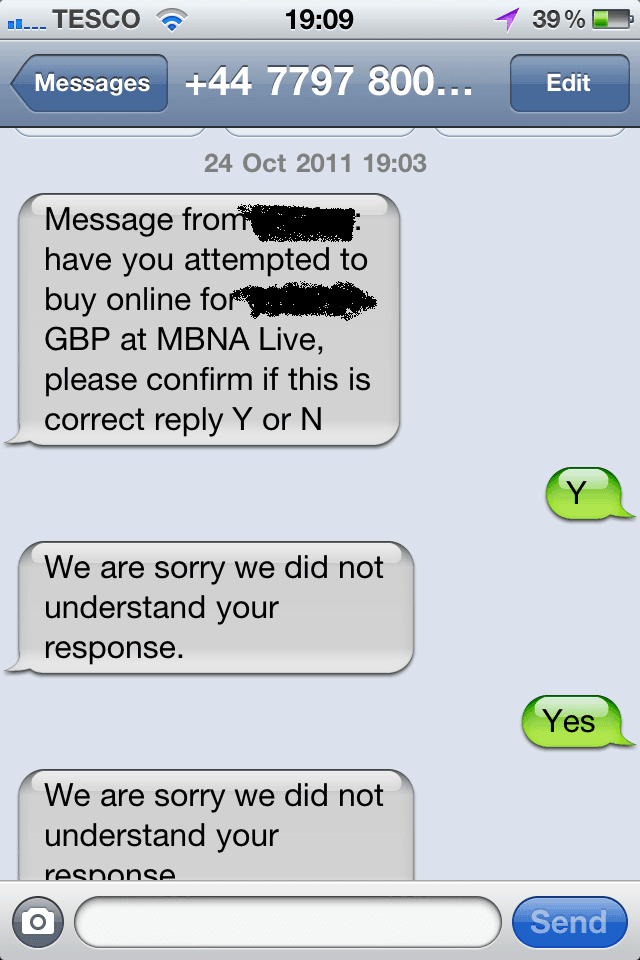

It seems to be a point of perverse pleasure to my friends that as a banking expert I actually seem to suffer worse treatment from my bank than they do! I suspect that this is in part my imagination. Having had repeated conversations around x for umpteen years, to then suffer issues around x is frustrating. Case in point – customer experience + fraud prevention. I recently had need to make 4 or 5 large transactions, with payment coming from my bank account. My bank branch won’t initiate a faster payments for me “for fraud protection reasons”. My telephone bank service won’t do the transaction according to them because the receiving bank doesn’t do Faster Payments. In reality, I know that the receiving bank won’t accept large value (but not that large) because of fraud. As a result, I usually pay via debit card on each card providers website. This month, 3 transactions in a row was blocked by my bank for, you guessed it, fraud reasons. Two of them I can perhaps understand – relatively infrequent previous interactions, so no discernible patterns. The third is the same amount, on the same day, to the same provider, in the same way, and with using SecureCode to sign the transaction. That’s frustrating, but I can almost live with that. It’s how it was then dealt with. Below is an excerpt of the automated text I got.  This went one for 4 or 5 more attempts, all to no avail. I'm afraid I'm unable to share my latter answers in case you are of a sensitive nature. Pity also I can’t play you a recording of the automated phone calls, because they were even odder. Having confirmed the transactions were mine, it thanked me, stated that it had declined the transactions and then hung up. But oddest still was the discovery that my bank has multiple fraud departments. Nothing in usual in that other than the discovery that one of them was secret. The bank wasn’t allowed to know its phone number, only I would know that. So when I asked how would I know if it was a genuine bank department if they didn’t know about it, they said the person would answer it with the name of the bank. When I rang, they wouldn't identify themselves, but I had to give all personal details for them to check my status. Either that, or for them to now take over my complete identity. Fraud protection at its best. So what can we learn from this? There is a fine line to be trod. For example, I don’t want the bank to ask me about every transaction but I don’t want the exceptional transaction to go unspotted. Equally, I want to the interaction to be brief but thorough. Fraud protection should be treated as a product, and the customer experience is as important, if not more so, than say the account opening procedure – the risk in an existing client s more predictable than in a new one for example. Banks who can address this may have a potent advantage of those who can’t. With more transactions, over more channels in an increasingly international world, this is a problem that is not going to go away. Rather than an opportunity, for many banks it will increasingly become a risk to their relationship to their clients.

This went one for 4 or 5 more attempts, all to no avail. I'm afraid I'm unable to share my latter answers in case you are of a sensitive nature. Pity also I can’t play you a recording of the automated phone calls, because they were even odder. Having confirmed the transactions were mine, it thanked me, stated that it had declined the transactions and then hung up. But oddest still was the discovery that my bank has multiple fraud departments. Nothing in usual in that other than the discovery that one of them was secret. The bank wasn’t allowed to know its phone number, only I would know that. So when I asked how would I know if it was a genuine bank department if they didn’t know about it, they said the person would answer it with the name of the bank. When I rang, they wouldn't identify themselves, but I had to give all personal details for them to check my status. Either that, or for them to now take over my complete identity. Fraud protection at its best. So what can we learn from this? There is a fine line to be trod. For example, I don’t want the bank to ask me about every transaction but I don’t want the exceptional transaction to go unspotted. Equally, I want to the interaction to be brief but thorough. Fraud protection should be treated as a product, and the customer experience is as important, if not more so, than say the account opening procedure – the risk in an existing client s more predictable than in a new one for example. Banks who can address this may have a potent advantage of those who can’t. With more transactions, over more channels in an increasingly international world, this is a problem that is not going to go away. Rather than an opportunity, for many banks it will increasingly become a risk to their relationship to their clients.