NACHA Payments 2018: A Corporate Banking Perspective on Real-Time Payments

I’ve been attending the NACHA Payments conference for many years, either as a banker, technologist, or industry research analyst. In recent years, the conference has been re-invigorated as the US begins to implement faster, real-time payment solutions.

With my research focus on corporate banking and treasury management, I attend NACHA with a somewhat different lens than some of my colleagues. This year, one of my interests was adoption of real-time payments by corporate and commercial clients.

Corporate Real-Time Payment (RTP) Adoption

Corporates remain lukewarm on real-time payment use cases. For example, “The Future of Payments: A Corporate Treasury Perspective” from EuroFinance and SWIFT found that only 42% of treasurers are looking for instant payments. The majority of supplier and payroll payments are scheduled in advance, making low-cost domestic ACH the payment type of choice. For the insurance industry, RTP proponents tout the ability to make immediate claims payments, but often a claim is paid to multiple parties, which isn’t easily handled by real-time payment rails. For example, when paying a homeowner claim, the payment might be split between the homeowner, mortgagor, and repair company, with final payment only occurring once the work is satisfactorily completed.

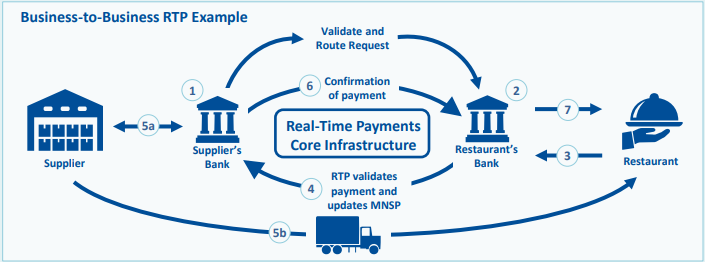

One RTP use case showing promise for business-to-business (B2B) and consumer-to-business (C2B) transactions is Request for Payment. In this scenario from The Clearing House’s “How do Real-Time Payments Work” brochure, a restaurant orders produce for immediate delivery from a supplier that does not extend trade credit.

The restaurant needs the produce for tonight’s dinner service, and the supplier needs to be paid before shipping the goods. Using the immediate messaging capabilities of a fully-featured RTP system, the supplier can request and receive payment nearly instantly. This scenario also applies to payment for services rendered. For example, a plumber completing a household repair can create an invoice on a tablet, sending it to the homeowner for immediate payment and creating a receivable in the plumber’s accounting software.

Currently, most treasury management systems (TMS) and enterprise resource planning (ERP) systems can only initiate and approve payments in batches. To transmit the payment file to their bank, a host-to-host file channel is typically used, with the bank picking up the payment file and processing the outgoing payments in yet another batch transaction. So for corporate adoption of real-time payments to take off, both banks and corporates need to invest in real-time payment initiation and processing capabilities.

More importantly, corporate treasury and finance professionals don’t yet see a compelling reason to shift away from traditional payment methods, highly reliable and tightly integrated into their day-to-day cash flow management activities. That said, corporate treasurers ARE looking for improvements in tracing payments in case of problems, quality and completeness of remittance information, and predictability of the total cost of a transaction.[1]

[1]The future of payments: a corporate treasury perspective, EuroFinance Corporate Treasury Network, 2017