It used to be that most bankers I interacted with had a keen interest in benchmarking their bank’s performance against peer group institutions. More recently, I’m noticing more interest in hearing about innovation among other non-bank retailers. I think this is wise and is why I am an avid reader of the broader retailing industry and follow eMarketer among others.

Why is there wisdom in this? Simply because diversity of thinking spurs innovation and accelerates value delivery. In banking, as in all areas of life, we cannot behave differently until we think differently. For too long, bankers thought like…. bankers. Only recently have we witnessed banks intentionally hiring non-bankers to fill key leadership roles. Now, this is becoming commonplace.

Here is but one example of how legacy bankthink led to missed opportunity. Ask most any non-bank retailer why they invested in digital and you’d likely hear somethink like “to better sell and service our customers”. Until recently, if you were to ask most any banker that same question, you would likely hear something like, “To migrate low-value transactions to self-service channels, thereby lowering the cost-to-serve”. Both views have merit, but they reflect dramatic differences in strategic intent and result in similarly dramatic differences in value delivery. One view is focused on revenue, while the other on cost reduction. After more than two decades of digital banking, we are now see growing interest in actually selling stuff digitally – something virtually all other retailers have been doing all along!

Yes, banks should be taking cues from other retailers – with caution.

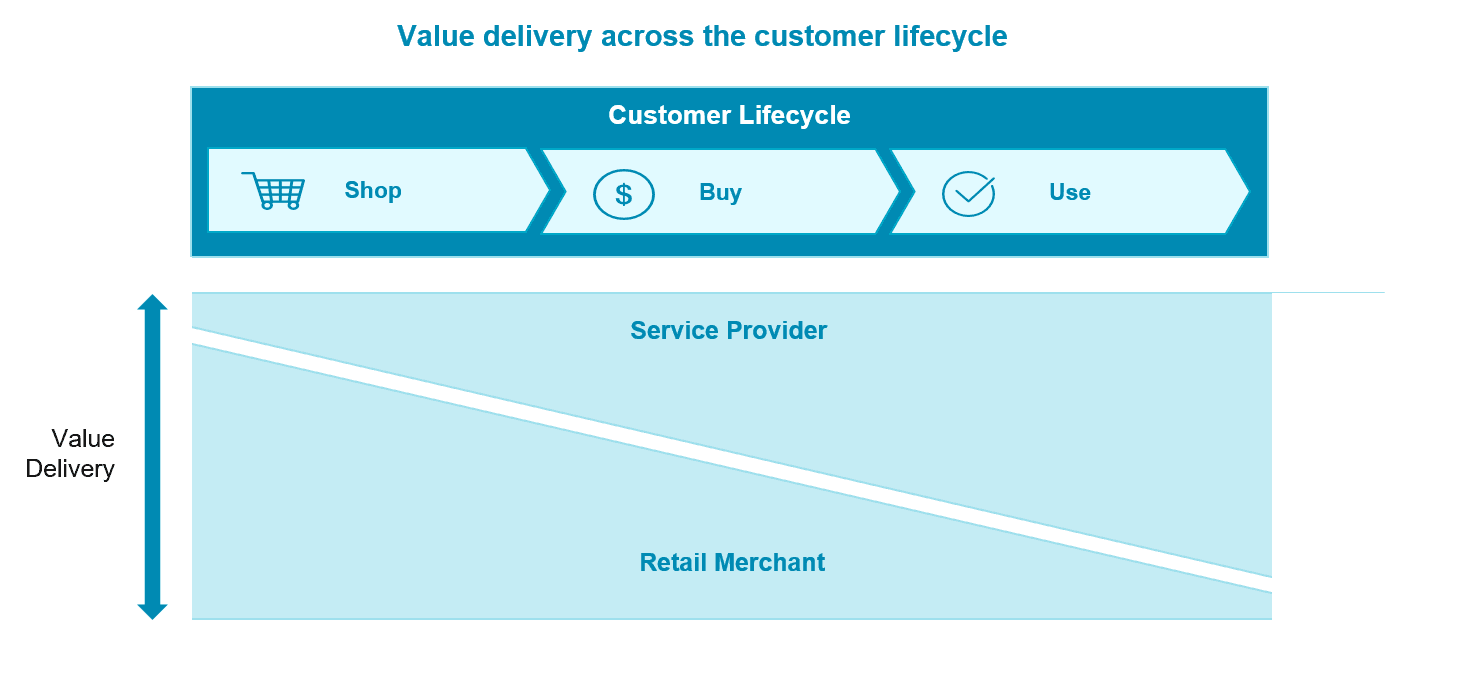

Why call for caution? It comes down to value delivery – how banks create, deliver and reinforce value to their customers. In my view, retail merchants deliver value that is front-loaded in the customer lifecycle – during the shopping and buying use-case. Beyond facilitating easy returns, there is little value to be delivered once the product is in consumer’s hands. Value delivery for banks, like other service providers is back loaded in the customer lifecycle. There is significant opportunity for value delivery after the account or loan is originated!