Banks are asking the wrong customer engagement question

30 July 2015

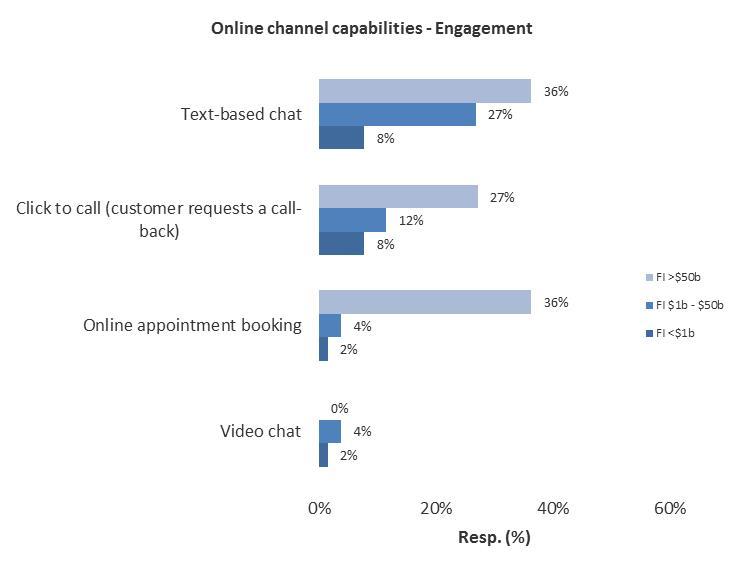

I have heard banks ask, “How to we use digital channels to bring traffic into the branch?” The rational is straightforward. After years of promoting self-service channels, branch foot traffic is declining – along with the sales opportunities that foot traffic represents. It’s a logical question, but the wrong question. A better question would be, “How do we enable effective customer engagement on their terms regardless of the channels involved? Rather than seeking to influence customer channel preferences, banks should be all about maximizing the effectiveness of each and every engagement opportunity, regardless of channel. They don’t seem to be. One no-brainer example is digital appointment booking – the ability for customers to book an appointment with a banker at a time and place of their convenience – using the bank’s online or mobile platform. Doing so represents convenience for the customer, a logical indicated action as part of online product research and an opportunity to improve branch channel capacity planning (because of the added visibility the mechanism provides). But, the most compelling reason to offer digital appointment booking in my opinion is because doing so maximizes the effectiveness of branch engagement. How so? Done well, frontline staff know who is coming and for what purpose. Consequently, they’re better prepared for the conversation. Banks that have implemented digital appointment booking are seeing significant improvements in sales results. Digital appointment booking should be commonplace – but isn’t. In a October 2014 survey of NA financial institutions, just 8% of respondents offered this capability. Most were large banks.  Source: Celent survey of North American financial institutions, October 2014, n=156 Even better would be to extend the appointment booking option to digital channels, as a phone or telepresence conversation. Engagement doesn’t have to be limited to face-to-face interactions – but is, in all but the largest banks. In the same survey referenced earlier, just 20% offered text based chat online, 12% offered click-to-call and 2% offered video chat.

Source: Celent survey of North American financial institutions, October 2014, n=156 Even better would be to extend the appointment booking option to digital channels, as a phone or telepresence conversation. Engagement doesn’t have to be limited to face-to-face interactions – but is, in all but the largest banks. In the same survey referenced earlier, just 20% offered text based chat online, 12% offered click-to-call and 2% offered video chat.  Source: Celent survey of North American financial institutions, October 2014, n=156 So, while banks offer abundant digital transactional capabilities, engagement remains largely something only offered at the branch. That dog won't hunt for long!

Source: Celent survey of North American financial institutions, October 2014, n=156 So, while banks offer abundant digital transactional capabilities, engagement remains largely something only offered at the branch. That dog won't hunt for long!

Source: Celent survey of North American financial institutions, October 2014, n=156 Even better would be to extend the appointment booking option to digital channels, as a phone or telepresence conversation. Engagement doesn’t have to be limited to face-to-face interactions – but is, in all but the largest banks. In the same survey referenced earlier, just 20% offered text based chat online, 12% offered click-to-call and 2% offered video chat.

Source: Celent survey of North American financial institutions, October 2014, n=156 Even better would be to extend the appointment booking option to digital channels, as a phone or telepresence conversation. Engagement doesn’t have to be limited to face-to-face interactions – but is, in all but the largest banks. In the same survey referenced earlier, just 20% offered text based chat online, 12% offered click-to-call and 2% offered video chat.  Source: Celent survey of North American financial institutions, October 2014, n=156 So, while banks offer abundant digital transactional capabilities, engagement remains largely something only offered at the branch. That dog won't hunt for long!

Source: Celent survey of North American financial institutions, October 2014, n=156 So, while banks offer abundant digital transactional capabilities, engagement remains largely something only offered at the branch. That dog won't hunt for long!