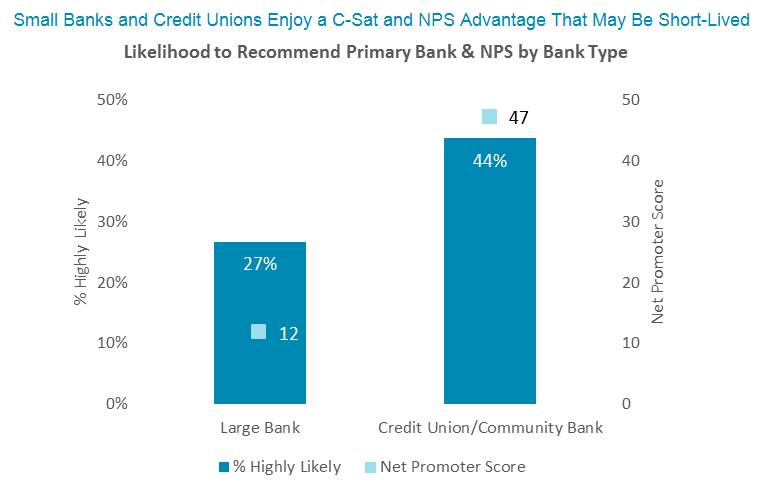

Small institutions have a measurable customer service advantage over big banks in many areas. They can't afford to rest on their laurels, however. Today’s advantage may be tomorrow’s liability.

Part 1 made the case for the imperative to perfect the branch experience based on current customer preferences. In Part 2, Celent makes the case for the urgency of perfecting the digital experience based on how customer preferences are evolving.

Customer service excellence requires consistently exceeding customer expectations. Too many banks think a slick new digital outfit alone will make the look beautiful. But banks can’t deliver excellent customer service with digital alone. Since beauty is in the eye of the beholder, banks pursuing customer service excellence must execute well when and how their customers choose to interact with them. Celent's research finds that for the overwhelming majority of US adults, this means executing well both digitally and in-person.

This report draws from two consecutive surveys fielded in February 2018 among banked US adults. Sample sizes (2,360 and 2,450) were chosen to ensure statistically representative results across age, income, and location segments of the population.