Risk and compliance functions have traditionally lagged in adopting new technology. But that had started to change in the last 24 months, and the challenges of the pandemic are accelerating this change. Efficient and effective compliance in the emerging digital era will require financial institutions to improve process automation, introduce automated insight generation, and support agility and flexibility. In some risk functions such as financial crime compliance, we have already seen adoption of new solutions powered by next generation technology such as artificial intelligence (AI) and machine learning (ML).

Financial institutions prefer to adopt next generation solutions to complement and augment existing systems and processes. Therefore, while deploying them, they must pay attention to integration and interoperability of the new solutions with existing systems as well as to infrastructure optimization to support exponential computation power needs and seamless connectivity with upstream and downstream systems.

A question that often comes up in relation to application of next generation solutions in risk and compliance operations, especially solutions powered by AI and ML, is about sourcing of new solutions. There are still a few large banks that have the resources and capabilities to develop in house next generation technology-based solutions in compliance. A good example is Goldman Sachs who has developed a machine learning-powered watchlist screening tool for their consumer banking business line for which they won a Celent Model Risk Manager 2021 award.

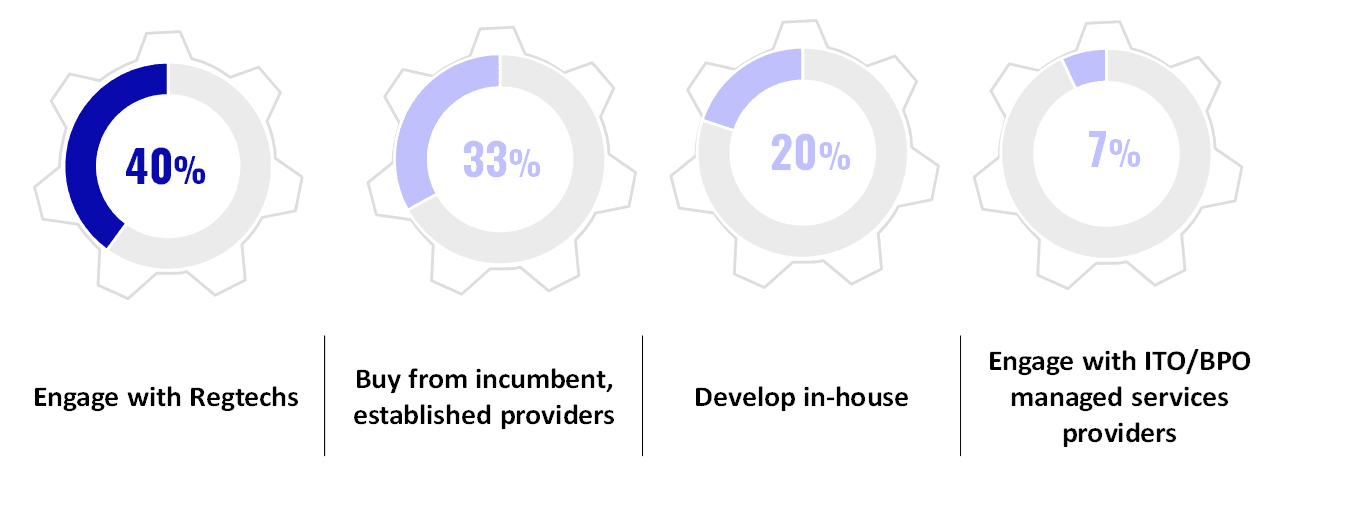

But in general, banks view their role diminishing in effecting innovation in non-core areas such as risk and compliance. This was reflected in a poll conducted during Celent’s Model Risk Manager Award announcement session, where the highest share of poll respondents indicated that working with regtech providers was the most preferred sourcing strategy risk technology, followed by buying solutions from incumbent, established providers.

What is the most preferred sourcing strategy for risk technology? (Select one answer)

Source: Celent

Costs, development time, and risk of failure are cited as big reasons behind banks retreating from innovation in non-core areas. Another challenge is to find talented resources with expertise in both risk function and new technology. Therefore, for innovation banks are increasingly looking at the regtech ecosystem. Regtechs are perceived to be agile, nimble, iterative, and unconstrained by old technology and bureaucracy. They also provide a low-cost, low-risk, and faster route to innovation. Incumbent vendors, because of their proven expertise, are still preferred for running critical pieces front to back, but can be perceived to be bureaucratic, reactive, hard to customize or integrate, and costly.

While there is a great deal of interest in innovating with regtechs, the flip side is that in some cases the new solutions and providers are still not proven or mature enough for direct adoption within the highly regulated and complex environments of banks. Furthermore, a rapidly burgeoning regtech ecosystem makes it hard to separate the contenders from the pretenders. Additionally, young companies may be viewed unfavorably from a procurement and vendor risk management perspective.

So, banks are exploring various ways for engaging with the regtech and fintech ecosystems. Some are acting as investors, incubators, collaborators, partners, and clients. Some banks have dedicated teams to track emerging companies, conduct pilot programs, and collaborate intimately. This trend was reflected among some Celent Model Risk Manager 2021 award winners.

For example, United Overseas Bank (UOB) has applied AI in their watchlist screening and transaction monitoring operations by leveraging the solution provided by the Singapore based regtech firm Tookitaki. Tookitaki is a graduate of UOB’s innovation accelerator, The FinLab, by which UOB fosters the growth of financial technology start-ups including collaborating with them to support its own innovation and digitalization efforts. For this implementation, UOB worked closely with Tookitaki to co-create customized machine-learning models by tuning Tookitaki's pre-packaged models to suit the bank’s specific AML needs.

Another example is HSBC which has implemented an ML-powered transaction monitoring solution exclusively designed for its insurance business. In this implementation, HSBC worked very closely with the vendor Featurespace to tune the models for their insurance specific needs and deploy it over Google cloud.

These trends are also reflected in the strategies of the incumbent and established providers of risk technology where we see technology and commercial partnerships developing among incumbent providers and regtech firms, and in some cases outright acquisition of regtech firms by incumbents. Celent has closely tracked the evolution of regtech solutions in our research; we will continue to expand our research as the regtech ecosystem matures and regtech adoption grows among banks.