Countering the Risk of Counterparties: Emerging Trends, Practices, and Technology in CVA Management

Abstract

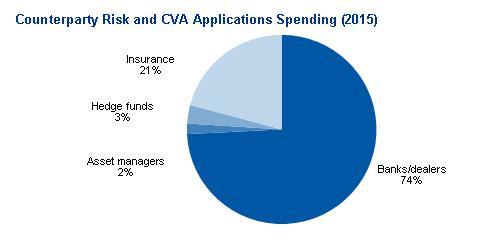

Globally, Celent expects firms to spend in excess of $850 million in 2012 on counterparty risk and CVA management systems, rising at a CAGR of 9.6% to $1.1 billion in 2015.

The strategic importance of credit value adjustment (CVA) and counterparty credit risk (CCR) management was brought to the forefront during the recent financial crisis. Virtually all active CVA groups faced major challenges in managing profit and loss volatility, with many tier 1 broker-dealers seeing significant losses from their CVA books. In a new report, Countering the Risk of Counterparties: Emerging Trends, Practices, and Technology in CVA Management, Celent finds that, despite considerable reform efforts, adverse conditions have not gone away. However, CVA management practices are advancing considerably in scope and depth.

Celent anticipates that expenditures by financial firms for CVA management will grow in strength with regulation and volatile market conditions, which are already pushing the management of counterparty risk and CVA towards the top of the agenda for most capital markets banks. External spending on CVA IT applications/components in particular will grow from $849 million in 2012 at a 9.6% CAGR to $1,116 million in 2015. Tier 1 dealer banks have led and will lead the charge, but regional and local financial institutions are following suit to upgrade underlying technology infrastructures in line with evolving business ambitions.

“In the coming years, Celent expects brokerages, market makers, and capital markets businesses of financial institutions to face multiple headwinds,” says Cubillas Ding, Research Director at Celent and author of the report. “Banks especially are faced with increased capital and funding costs, higher fixed expenditures and operational overhead, and an uncertain economic outlook.”

Beyond the initial regulatory rules from Basel III and Dodd-Frank central clearing, Celent predicts emerging organizational responses from dealer banks and the rapid evolution of CVA practices around the pricing and risk management of counterparty risk to create second and third order ripples through the industry, extending to buy side and corporate derivatives end users. While dealer banks are taking decisive investments to integrate the pricing of CVA and funding value adjustments (FVAs) into the front office, CVA pricing practices and methodologies are not uniform among various institutions. Hence, these divergences are fueling greater “market shopping” behaviour from the buy side and corporate end user prospects. Such second and third order dynamics also imply that firms will require enhanced decision support capabilities and enhanced infrastructure to navigate the imminent changes.

As part of a series of reports, Celent analyzes the top emerging trends in counterparty risk and CVA management, spending drivers, and their implications for technology strategies. The report also examines the broad landscape and characteristics of CVA solutions available in the market.