How Financial Firms Must Adapt to the COVID-19 Era

How have technology priorities changed within financial services as a result of the COVID-19 pandemic? It’s easy to assume that financial institutions (FIs) will behave in the same way—that digital will accelerate, that we’ll continue to work from home, or that the impact on cashflow going into 2021 will be difficult.

In reality, the financial services industry isn’t just one thing. Each of its multiple pockets can behave differently. That’s what we discussed on May 27th in “Counterintuition, Outliers, and Hockey Sticks: FIs in the Age of COVID-19,” the first webinar in Celent’s eight-part Survive to Thrive series about how the pandemic is changing technology priorities across financial services. Upcoming sessions will address the impacts on Corporate Banking, Retail Banking, P&C Insurance, Life and Health Insurance, Capital Markets, Wealth Management, and Risk. Here, I’d like to share key takeaways from our first session. (If you missed it, watch the on-demand recording.)

So Far: The Impact of COVID-19

COVID-19’s impacts for financial services falls into three categories, each with implications for technology strategy:

Counterintuition

Some things that we thought would happen didn’t actually play out. This may be due to thinking about first-, but not second- or third-order effects.

- With the US Paycheck Protection Program (PPP), it may have seemed likely that the biggest banks would be the biggest lenders in this program created to help small businesses. That wasn’t the case. Instead, the smallest banks by asset size (with

- In insurance, lines are highly specific, creating fragmentation even within this single segment of financial services. Negative attention—with the potential for reputational damage—has been given to some stories, such as business interruption claims that went unpaid. COVID-19 is also driving a range of responses to changing insurance needs. In the life insurance industry, the pandemic emphasized that many are underinsured; this created an influx of new business requests, but much is being declined as underwriting rules get tighter. On the other side, there’s a positive takeaway within auto insurance: as the number of miles driven has fallen, some insurers are giving a portion of premiums back to customers.

- Responses to cash usage emphasize the importance of being familiar with the marketplace. It may have seemed likely that cash usage and visits to bank branches might go down uniformly. But Japan’s preferences for cash remained strong: Japan’s cashless ratio is below 20%, compared to 96% in South Korea and 66% in China.

Ratchets

Changing human behavior is very difficult. Changing it back is even more so. We encounter these ratchet moments in life frequently. (Once you get your own washing machine, you’re not likely to return to the laundromat.) They exist in financial services, too.

FIs need to determine how big the potential ratchet moments are and the scale of the possible impact(s) over time. Assess:

- Cash usage: Will we be using cash more once we feel comfortable spending in person? Will we be going contactless or moving to peer to peer (P2P) payments?

- Mobile banking: Will people go back to the branch when it becomes easier to do so?

- Video calls: Will we keep using video calls or will we revert to phone calls and/or in-person meetings?

- Real estate: How will real estate be repurposed? Different solutions are already appearing for different types of businesses.

- Financial organization: Just as the pandemic has driven people to tackle overdue household chores, it may spur them to get their financial houses in order. It hasn’t happened yet, but what will be the implications for FIs as clients get to that state?

Hockey Sticks

Absent an exogenous shock, there aren’t many hockey sticks in behavior, yet we’re seeing them today and are likely to see more announcements along these lines:

- The US savings rate has spiked, with $1 trillion of additional US deposits in the 1st quarter.

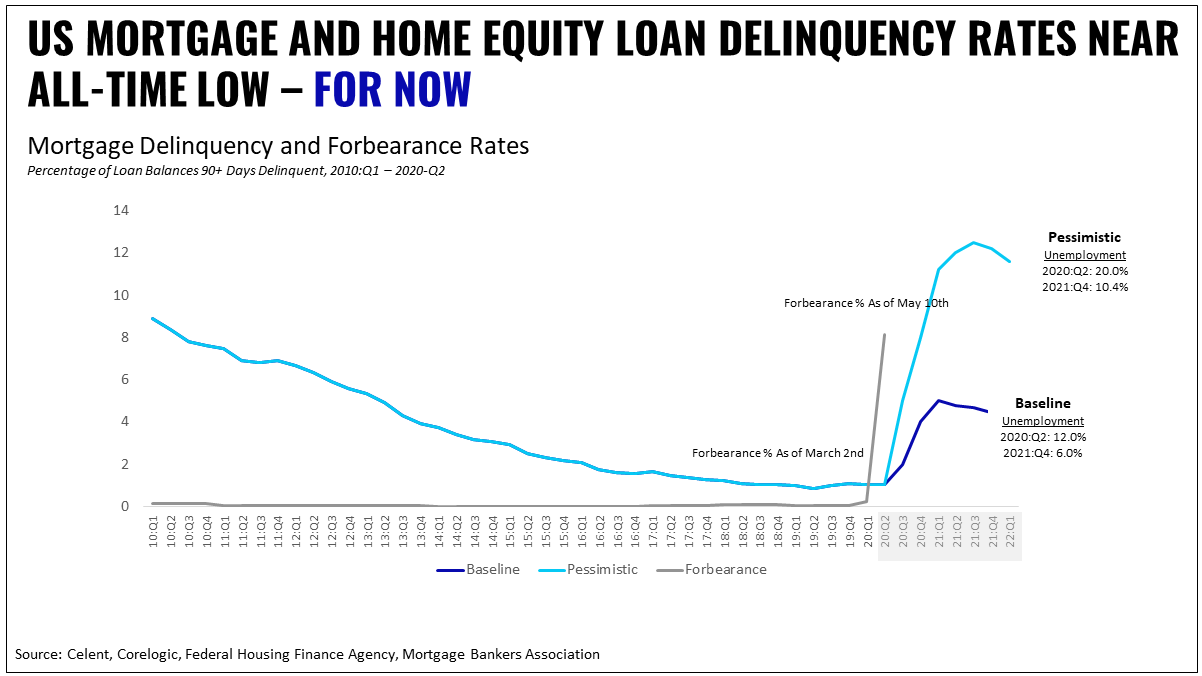

- Mortgage forbearance ticked up significantly at the end of April. CoreLogic predicts that loan delinquencies will increase significantly, whether the scenario evaluated is baseline or pessimistic. In either case, implications are dire and will impact how banks invest resources into things like collections technology.

- Within insurance, Allianz Care saw a 235% increase in international health insurance policies applications and an 83% surge in web traffic, due in large part to new business processing.

Evaluate Your Technology Strategy

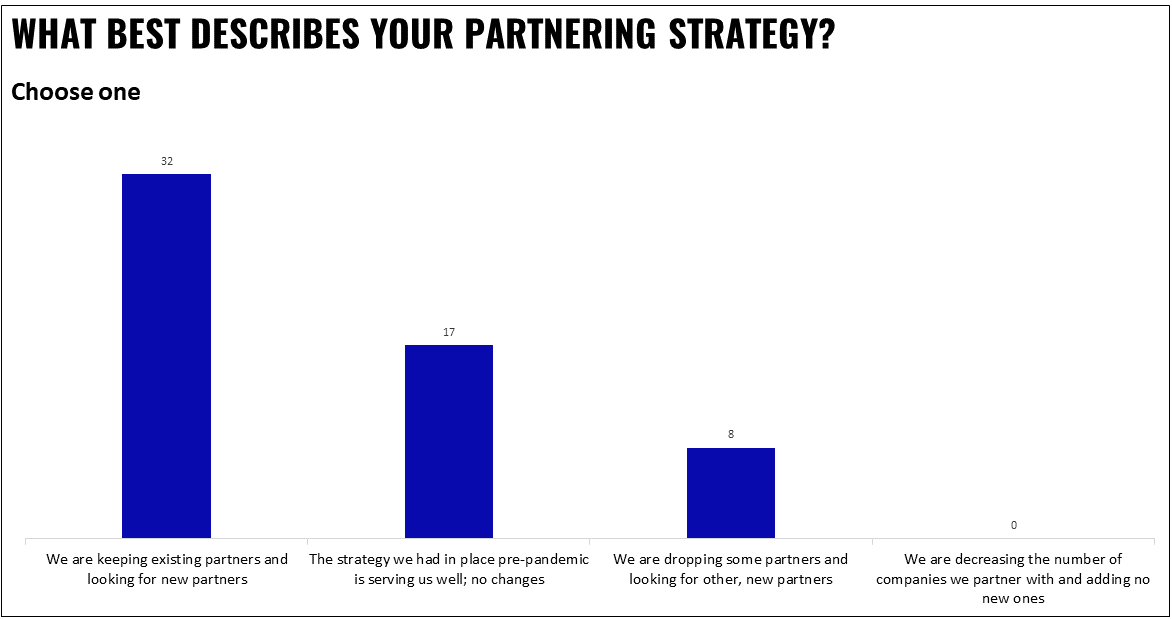

Clearly, all sorts of things have played out since the pandemic hit. What are the implications for technology strategy across industries within financial services? Responding to a flash poll during the live webinar session, 56% of participants answered that their partnering strategy is to keep existing partners and look for new partners. This reflects the need to team up with partners who execute initiatives better, faster, cheaper than some of the FIs are able to themselves.

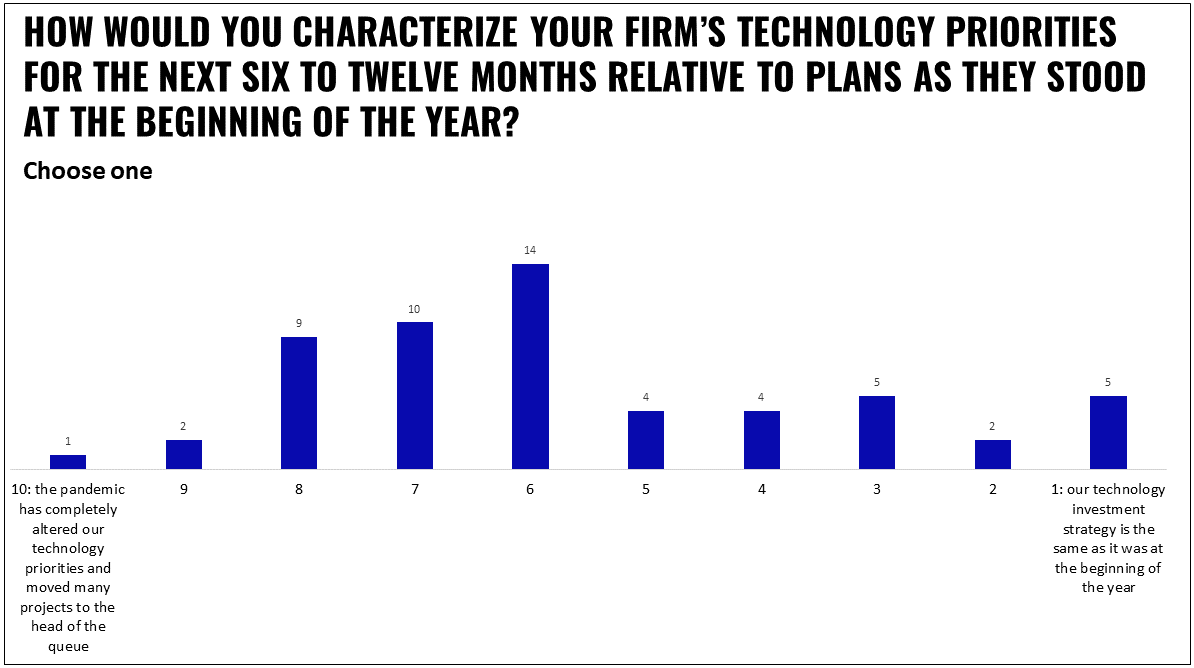

The pandemic is starting to alter technology priorities and moving projects to the head of the queue. Celent is hearing this from clients; polling during the webinar echoed this. In a typical financial planning year (January to December), the summer months are usually the time for planning for the subsequent year. That priorities for 2021 are already being questioned as FIs go into their planning cycle isn’t surprising.

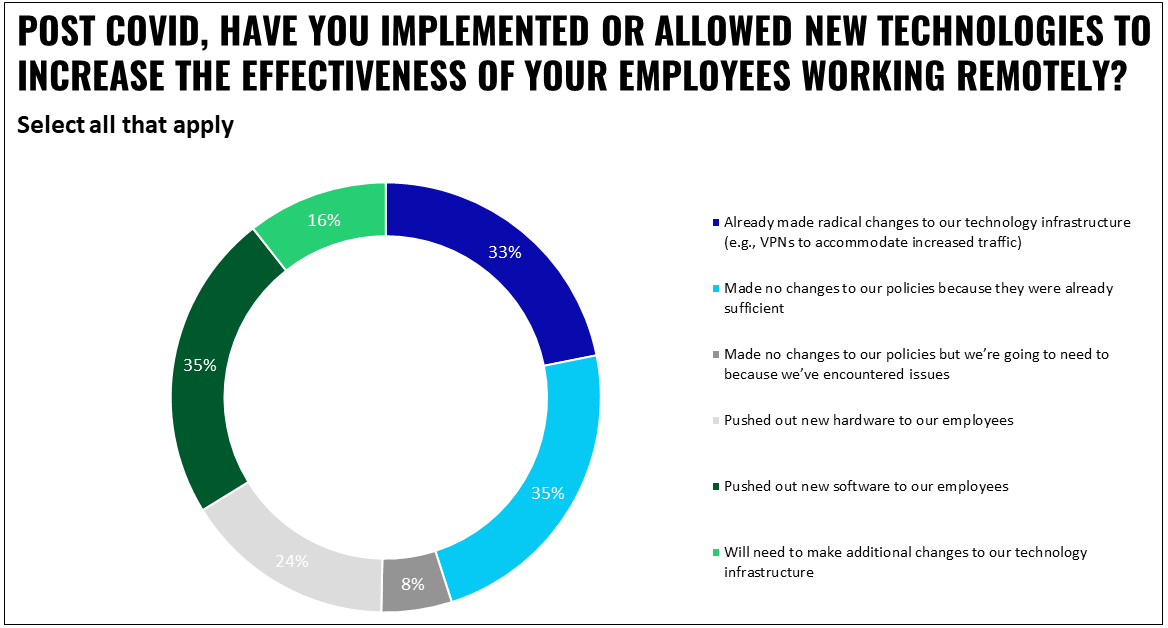

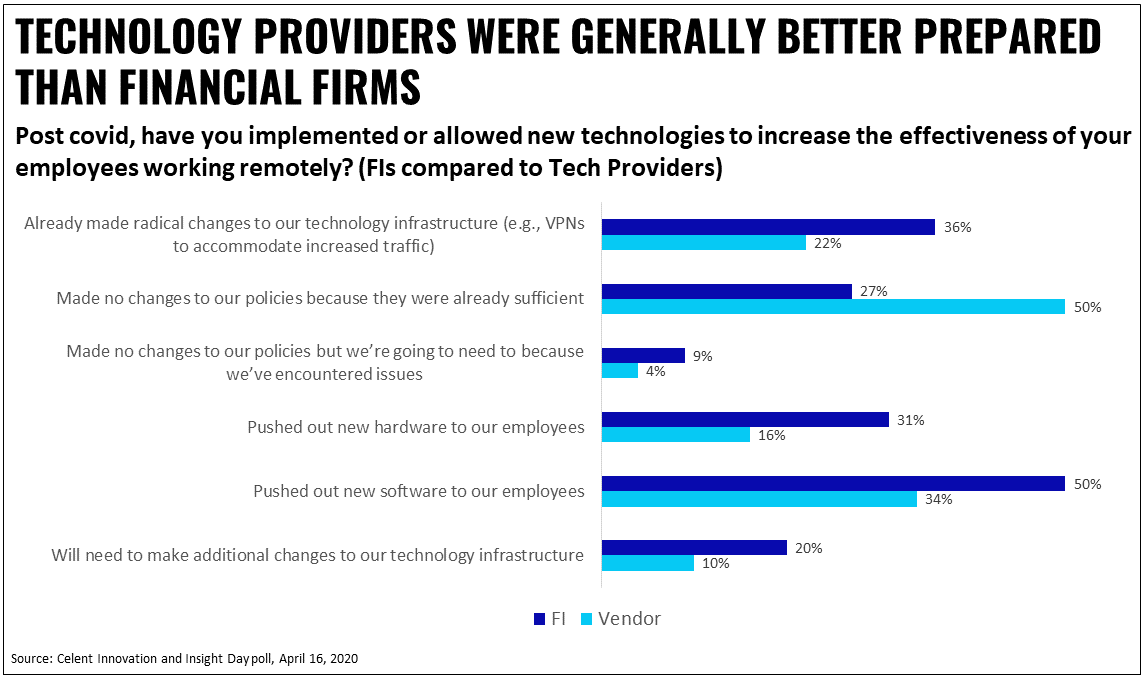

COVID-19 has already driven more than a third of FIs to make radical changes to their tech infrastructure to improve the effectiveness of employees who are working remotely. The results from the live webinar, as shown in the chart below, indicate that even more FIs have made radical changes than was the case when the same question was asked the same question during Celent’s Innovation & Insight (I&I) Day, held on April 16 this year[C|P2]. A growing number are also indicating that they’ll need to make additional changes.

Consider the Systems and People Driving Tech Priorities

It can be all too easy to get trapped in our silos or work on optimizing an individual process without knowing what’s going on in the rest of our own institution—or the rest of the world. Instead, make decisions regarding technology priorities through the lens of systems thinking. This holistic approach focuses on how the different parts of a system interact with each other, how feedback loops occur over time, and how this all works in the context of larger systems. (For additional reading, the book Thinking in Systems by Donella H. Meadows is excellent.)

With systems thinking in mind, remember that people are the driving force behind the decisions you make regarding technology priorities. Evaluate the behavior not just of consumers, but of employees, partners, and regulators. All of these individuals take actions and have reactions that are shaped by experiences as the response to COVID-19 plays out.

Be mindful of the possible impact of a key aspect of systems: latency. Just as COVID-19 has a 14-day lag between infection to manifestation of systems, many events have effects that don’t play out for weeks or months. Keep latency in mind as you place your bets in the coming months; beware of reading signal too early.

The pandemic is showing us that interconnectedness is a key feature of the world we’re going to be living in. To help your clients and solidify your lifetime relationship with them:

- Be proactive. Banking, insurance, and wealth clients are going to need advice, counseling, and financial help. Reach out to them across all phases of their life; don’t wait for them to call you.

- Put your data house in order. You’re likely going to be collecting significant amounts of new data about new behavior. Make the most of that data. Look for new patterns that can create effective offers or tweak underwriting models.

- Watch signals carefully. Let the dust settle before describing the new normal. Be aware of second order effects.

- Look for good partners. At a time when technology providers were generally better prepared than financial institutions to respond to COVID, some FIs can benefit greatly by working with partners.

- Use scenario planning. As data scientist Barrie Wilkinson, my colleague from Oliver Wyman, discussed during I&I Day, scenario planning can help evaluate the feedback loops present in the systems that will impact FIs. Don’t lock yourself into anything.

- Be humble, flexible, and agile. What’s going to happen next is uncertain. Be prepared to pivot.

Additional Survive to Thrive Resources

We hope that you’ll join the conversation. Visit the Survive to Thrive hub page to:

- Register for upcoming live webinars in this eight-part series,

- Watch past webinars, available on-demand, and

- Access additional resources about industry-specific technology responses to COVID-19.

- To learn more or to set up a meeting with a Celent analyst, please message us.