The (L)IBOR rate which we have all known and loved-then vilified and hated is going away. Regulators and market watchers saw the rate has easily manipulated and potentially unfair-to a more market based benchmark rates. We are in a massive 250 trillion dollar transition from the London Interbank Offered Rate to Alternative Risk Free Rates (AFRs). This creates challenges for firms to consider the technology providers they will partner with for this crucial transition.

For some this transition is existential and changes are required across their full suite of businesses and counterparties with 1000s working through the myriad implication. The fear today is unintended consequences and the long tail of complicated interactions at the product, hedge, exposure, counterparty, and risk level.

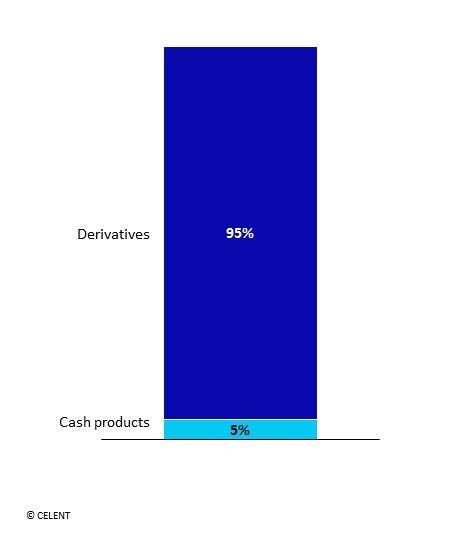

Tail Wagging the Dog

OTC and exchange traded derivatives are 95% of the dollar LIBOR notional outstanding:

For those old enough to remember Y2K, the hyped move from 1999 to 2000, the IBOR transition has a similar feel, at least in the financial services, without the apocalyptic feel…(that ended with a whimper). Perhaps, a more appropriate comparison was the post-Dodd Frank move to interest rate clearing. Yes, there were many workflow changes, but big differences that arose in pricing, valuation, model management, technology, capital allocation, risk, and created unintended consequences.

Of the considerable efforts required, the technology, system and infrastructure challenge will be the bulk of the effort for most firms. Celent expect that technology will be 35% percent of the overall spend by firms which skews toward capital markets focused firms. A large part of the overall technology spend will be in upgrading, replacing, or rearchitecting existing systems to work in today’s rate regime, the long tail transition away from LIBOR, and in a future state of AFRs.

- Many have asked was the IBOR era an error or is the change the bigger error. We shall see.

Technology Solutions for the LIBOR Transition