The banking sector is facing the formidable challenge of responding to COVID-related changes to customer behavior and the adverse impact of economic weakness. In parallel, there is the presence of a potential new class of competitors with powerful networks and deep investment pockets (the so-called big techs). This combination of factors will most likely drive significant discontinuity in the banking sector.

Our joint report with the International Banking Federation (IBFed) analizes the competitive dynamics in major markets. The status quo is defined by continued dominance of traditional banking players, and a niche penetration by big techs and specialist fintech in most major markets. However, in a few major markets, the analysis highlights how the unique scale and “ecosystem” model of big techs has the potential to fundamentally change competitive dynamics in banking. We have spoken with a broad range of industry participants and policymakers across most major markets to gauge current views and challenges for the future.

In our report, we raise important questions for policy-makers, banks and society in general. Big tech technology capabilities can bring benefits in customer outcomes and efficiency that can be put to good use for society — to serve inclusion, to fight financial crime, to improve the cyber and operational resilience of our financial system, to name a few. But they also raise new types of risks and challenge the traditional “vertical” (sector-oriented) model of regulation and supervision, which may no longer serve society’s best interest today.

The main question for banks is how to prepare for the possibility of a major incursion of the big techs into their core markets, where this has not happened already. It is possible that big techs choose not to engage in core banking markets, but the general sense from our interviews it is not a question of if but when. Banks may therefore need to rewrite their past formula of success, and transform the way they serve customers, interact with third-parties and make the very fundamental strategic choices of whether they wish to compete as a “network” business model or compete in specific businesses serving others’ network.

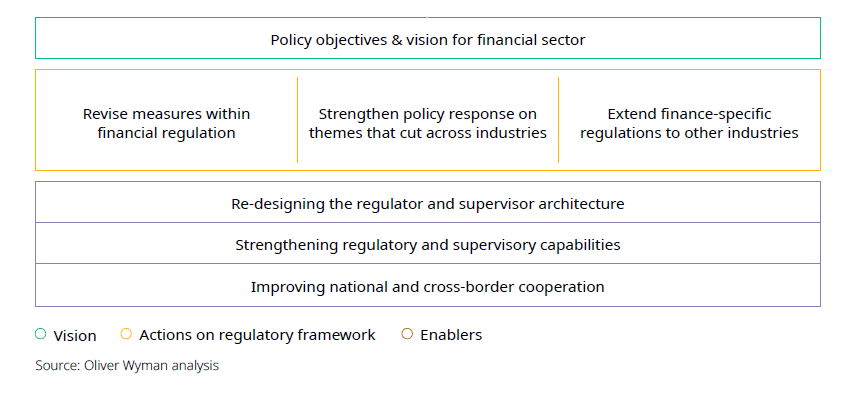

Financial services policy-makers — quite rightly — have prioritized COVID response and forebearance in the banking sector. However, there is a clear need to get on the front foot to support and shape an orderly modernization of the financial sector that will be required in the post-COVID economic and financial regeneration. The two extremes of policymaker response are unattractive: 1. unfettered, open competition with a blanket relaxation of participation rules will pole-axe weak banking business models and create financial stability risks and probably consumer protection issues; 2. high barriers to entry for non-banking players will slow down innovation and protract the existence of non-viable banking models. There is an optimal policy response somewhere in between the two extremes: this will require policy-makers to think differently with respect to competitive boundaries, accept higher uncertainty and faster responses and possibly re-think the institutional architecture that governs the intersection of financial services and technology sectors.

In a world that is understandably concerned with COVID response, we hope these insights highlight the risks of a disruptive change that could result from banking sector weakness and restructuring and encourage policy-makers and the banking sector to invest time in shaping successful future business models and the orderly transition required.

You can access the full report here.