This year, COVID market turbulence saw significant losses from capital markets participants, especially dealer and regional banks, associated with credit valuation adjustments. Whilst markets have 'calmed', it would not take much for turbulence to flare up again. Market participants are not taking anything for granted.

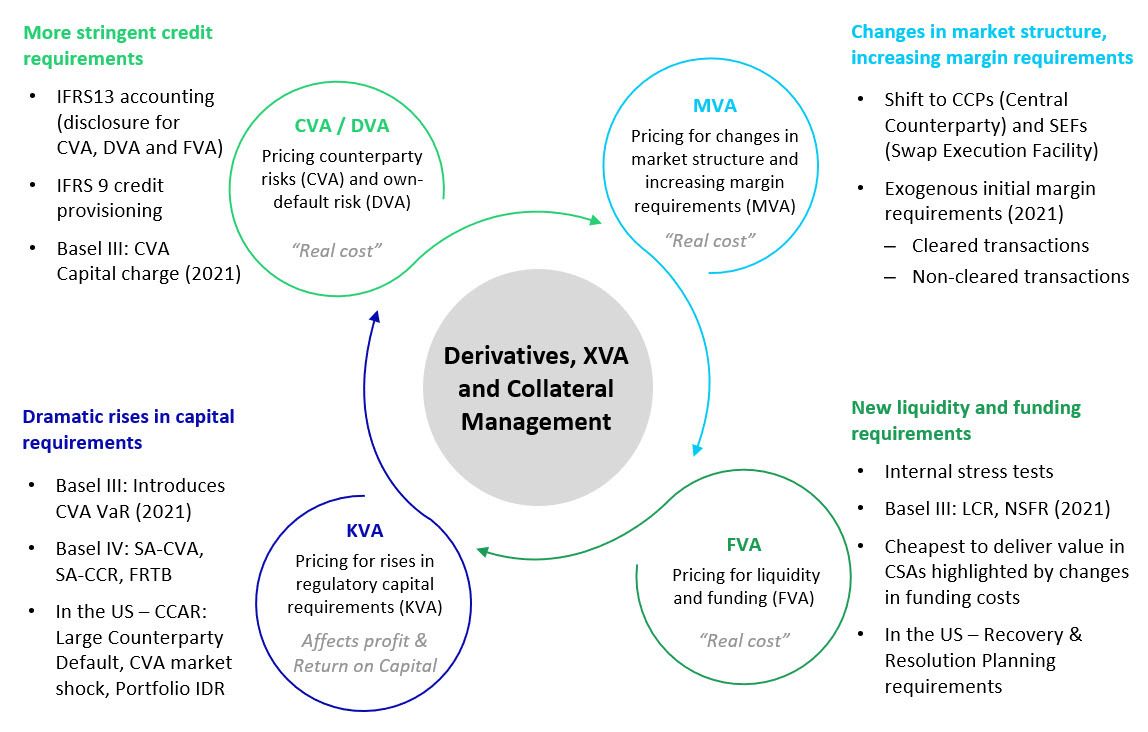

The XVAs are a family of valuation adjustments reflected in the pricing of derivatives trades, to incorporate the costs of hedging, funding, collateral margins and capital into trades, and to take into account incoming regulatory rules such as Basel III leverage and liquidity ratios that also shape pricing decisions.

Over the years, dealer banks are balancing a pragmatic tightrope of needing to reflect these additional costs into how they price trades with client counterparties, including XVA components such as counterparty risk (CVA), own-default risk (DVA), funding (FVA), capital (KVA) and margin (MVA) in order to minimize the mispricing of trades, yet still remain competitive in winning deals with prospects.

There are a dazzling arrange of regulatory acronyms and numbers that have crept into the financial industry's lexicon, many to do with regulations, risk capital and emerging technologies. These are arguably confusing at times, but there are real and profound changes happening. Multiple cohorts of regulations are transforming the economics of global financing, collateral and derivative markets, where impact to participants from a profit, returns and cost standpoint is multifaceted.

For dealer banks, a best-in-class XVA framework is key to appropriately price, hedge and manage the risk originated from changes in the quality of the counterparties and/or in the cost of funding margin and collateral requirements in OTC transactions. This is still a work in progress - firms may have core capabilities to price market-implied CVA in place, but the path towards achieving a best practice approach for their market-implied XVA framework for pricing, hedging, accounting and risk management continues to evolve through sustained advances in technology, development and quantitative approaches.

At the same time, as derivative pricing on the sell side becomes more complex, buyside and corporates that employ derivatives are increasingly also needing to understand the all-in derivative pricing and determine if prices offered are fair value. They also need to reflect these in their accounting, financial reporting, and regulatory obligations.

Celent wil be releasing a series of reports to deliver insights on the implications of next generation technologies on XVA management practices, emerging themes, future solution trajectories, and vendor offerings. Watch this space.

To learn more about how capital markets firms are upgrading their operations, please contact Celent for more information on our latest reports on these topics. Please see here Celent's insights for Capital Markets.