Earlier this year, Celent released a report, Branch Boom Gone Bust: Predicting a Steep Decline in US Branch Density, which made comparisons between the decline of brick-and-mortar video rental stores, like Blockbuster, and branch banking in the US. Celent argued that the decline of Blockbuster at the hands of digital alternatives is a cautionary tale for banks that still value a traditional branch network. As I’m sure no surprise to most, Blockbuster recently announced that they would be shutting down all remaining retail locations—around 300—effectively ending operations.

"This is not an easy decision, yet consumer demand is clearly moving to digital distribution of video entertainment," said Joseph P. Clayton, DISH president and chief executive officer. "Despite our closing of the physical distribution elements of the business, we continue to see value in the Blockbuster brand, and we expect to leverage that brand as we continue to expand our digital offerings."From the chart below, taken from the above Celent report, its clear that this has been in store for a while. Yet as countless blogs and news articles praise or nostalgically lament the once-great video giant’s downfall, an old question is being explored once again: what will happen to the independent video rental store? Put simply, they're evolving. Faced with years of low business and an ever shrinking cult customer-base, many small video retailers are innovating in an attempt to draw business back into stores, adding value in areas un-served by Netflix or Redbox. From the an article by Indiewire.com:

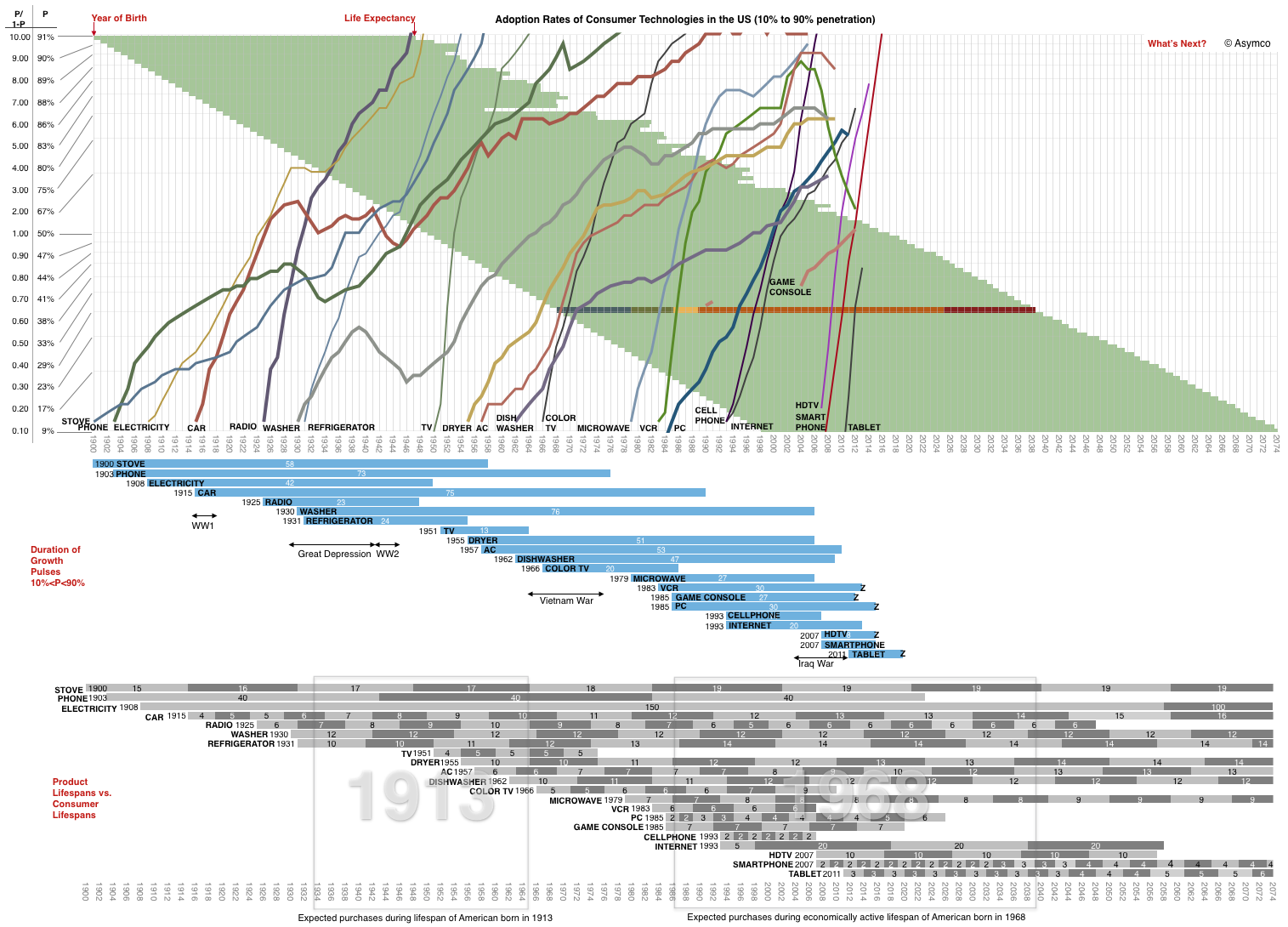

“Videology in Brooklyn put a bar in front and a big video screen in back, where customers can sit at tables and drink while watching free screenings. It doesn't even look like a rental outlet anymore -- it moved all the discs aside from the new releases off the floor and put in computer kiosks for customers to browse the inventory. Vidiots in Santa Monica, supported by its community and patrons from the Hollywood film community, raised money to open a screening room and a non-profit foundation that holds workshops, classes, and outreach programs. It's redefining its sense of purpose.”Is this an example for banks? Sure it is. Similar to what’s happening in retail, banks can add value to a branch-based experience. Consider this line from the above quote: “[The video store] doesn't even look like a rental outlet anymore.” Small video retailers are refreshing the idea of what a video store is, and what it could be. Smaller banks like Umpqua Bank have already explored this idea years ago, and even megabanks like Wells Fargo are exploring the possibility of compact “boutique” branches. The rise of digital The other day I came across a cool chart from Horace Dediu that does a good job at visualizing the change in consumer behavior that drove Blockbuster underwater, and is driving younger generations toward less branch engagement. A larger version can be found here.

The adoption of smartphones and tablets, even in relation to internet and mobile phones, sit in stark contrast to the group. The second part of the graph shows the duration of growth from 10% adoption to 90% adoption in years. For smartphones and tablets (estimated), these numbers are in the single digits. The result is a substantial decrease in the development life-cycle of innovation, early adoption, and late adoption. For branches, this means a dramatic and rapid shift in the way consumers interact with their financial institutions. Blockbuster trailed both Netflix and Redbox by almost five years before releasing competing products. The company not only failed to react to shifting demand, they arguably contributed to it. The founder of Netflix started the company after he paid $40 for a late video rental. Blockbuster continued to remain unmoved by customer complaints over late fees, eventually settling a series of lawsuits over the matter. Customers in turn, looked to innovative start-ups (i.e. Redbox and Netflix) to fill the void. Blockbuster failed to adapt. The path forward is a mix of early adoption and, like independent video stores, a rethink of traditional business practices. Let’s be clear, branches won’t die, but it’s difficult to make the case that significant redesign won’t happen. Will banking bloggers someday down the road, sitting in an independent video rental coffee shop, write about the nostalgia of traditional branch banking? Probably.

The adoption of smartphones and tablets, even in relation to internet and mobile phones, sit in stark contrast to the group. The second part of the graph shows the duration of growth from 10% adoption to 90% adoption in years. For smartphones and tablets (estimated), these numbers are in the single digits. The result is a substantial decrease in the development life-cycle of innovation, early adoption, and late adoption. For branches, this means a dramatic and rapid shift in the way consumers interact with their financial institutions. Blockbuster trailed both Netflix and Redbox by almost five years before releasing competing products. The company not only failed to react to shifting demand, they arguably contributed to it. The founder of Netflix started the company after he paid $40 for a late video rental. Blockbuster continued to remain unmoved by customer complaints over late fees, eventually settling a series of lawsuits over the matter. Customers in turn, looked to innovative start-ups (i.e. Redbox and Netflix) to fill the void. Blockbuster failed to adapt. The path forward is a mix of early adoption and, like independent video stores, a rethink of traditional business practices. Let’s be clear, branches won’t die, but it’s difficult to make the case that significant redesign won’t happen. Will banking bloggers someday down the road, sitting in an independent video rental coffee shop, write about the nostalgia of traditional branch banking? Probably.