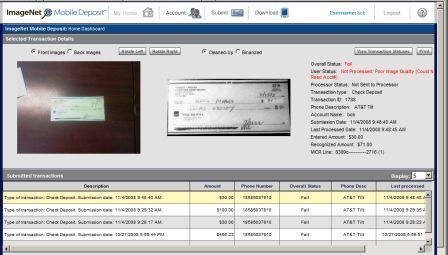

On 28 April, NCR announced its integration of Mitek Systems' ImageNet Mobile Deposit to its’ APTRA Passport imaging platform. The NCR decision follows integrations already completed by J&B Software and RDM Corporation. This was a smart move on NCR’s part in our opinion. Others are sure to follow. Mitek announced its ImagNet Mobile Deposit platform in January 2008 and followed with announcements of Blackberry support in September 2008 and Apple iPhone compatibility in October. To be sure, Mitek is pushing the envelope with remote deposit in an environment where the industry is barely adept at small business RDC using specialized check scanners and “consumer capture” is largely offered among credit unions alone. But all this is changing. In our opinion, mobile remote deposit is destined to succeed for two reasons: convenience and device ubiquity. Apple shipped 2.3m iPhones in 2007 and 13.7m in 2008. RIM boasts about 25 million BlackBerry subscribers through February 2009. The world is quickly going mobile, and mobile banking is riding the wave. Bank of America alone boasts well over a million mobile banking users (June 2008). Apart from risk concerns, why wouldn’t mobile RDC be an obvious feature for select mobile banking users? We’re not alone in expecting mobile remote deposit to catch on. In research derived from a Fiserv-sponsored online survey of roughly 300 customers in October 2008, one third of respondents see a need to offer mobile deposit capture services to their business customers. The majority of respondents indicated that businesses that sell products and services at the buyer’s location (such as home appliance repair businesses and food and beverage distributors with trucks in the field) are their primary target market for mobile deposit capture. We agree. Banks would do well to launch mobile RDC first to business clients while there may still be fee income to be had. But banks clearly aren’t rushing into mobile RDC as they had with RDC’s original incarnation. Caution is understandable, but scoffing is short sighted. Celent’s position is that viability of mobile check deposits rests on four requirements: 1. Client usability - the application must be fast, simple to use and provide reasonably consistent performance despite widely varying lighting conditions, steadiness of hands and check stock characteristics. Obviously, mobile deposits introduce greater variability in image characteristics than images captured on specialized scanners. 2. Operational viability - even the most enriching user experience would be for naught if mobile deposits wreak havoc in the back offices of deploying financial institutions. 3. Security - image and data transmissions would need to be secure. Any security vulnerabilities would prove disastrous. 4. Broad device support - part of the value proposition for mobile deposits rests on not having to invest in image capture devices. To provide some direct experience in using ImageNet Mobile Deposit, Celent requested a test account from Mitek and experimented using the authors AT&T Tilt device. Installing and learning the simple application took no longer than 15 minutes. Sample deposits were performed using a mix of personal and business checks after lining out the check codeline for security. Overall user experience was favorable – even for this novice camera phone user. And, the image analytics appear to have been up to the task. With intentional carelessness toward lighting, contrast and steadiness of hand, resulting check images appeared Check 21 ready. Mobile RDC is clearly a nascent market, and banks have lots on their hands these days. But sitting on the mobile RDC sidelines may leave banks wishing they hadn’t. [caption id="attachment_459" align="aligncenter" width="448" caption="Checks captured on the author's device with intentional carelessness"] [/caption]

[/caption]