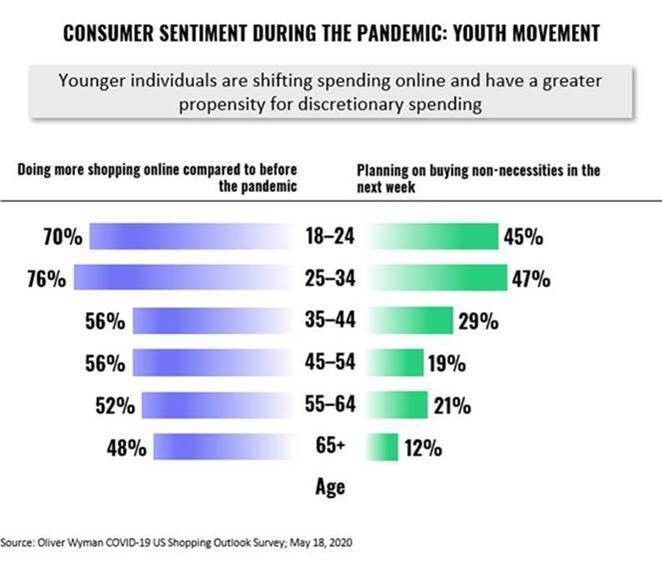

In a recent Oliver Wyman study on the impact of COVID stay-at-home guidelines on individual spending habits, they found what most might have guessed, an dramatic acceration in online shopping.

Now add the fact that a number of companies are either considering, planning or in fact moving a higher percentage of their historically in-office workforce to remote. Companies like Facebook, where last week Mark Zuckerberg announced that “…I think that it’s possible that over the next five to 10 years — maybe closer to 10 than five, but somewhere in that range — I think we could get to about half of the company working remotely permanently.” That would equate to about 24,000 of the current 48,000 employees.

At Celent, I analyze the life insurance side of industry. In addition to what Facebook and others outside the insurance industry have stated, I have spoken to a number of life insurers that are also considering drastic increases to the percentage of their remote workforce. Nationwide was one of the first insurers to announce changes as a result of COVID-19. In an April 29, 2020 press release they announced, “a plan to permanently transition to a hybrid operating model that comprises primarily working-from-office in four main corporate campuses and working-from-home in most other locations”.

When I think of the rapid acceleration of more people working from home which reflects directly to the dramatic increase in online shopping, I think of the impacts to life insurance products, product sales and distribution. The question that begs for life insurers is how all this will translate to future individual insurance product consumption. These cultural shifts, which essentially transpired overnight, will have a significant and lasting impact on life insurance shopping habits. Pre-COVID, Life insurance has been a traditionally relationship-based business and relatively slow to move to direct channel distribution. Unlike the property side of insurance that has made the leap to direct online sales years ago, Life has been very slow to follow. Excluding fairly recent entrants into the life market like Haven Life, traditional life insurers may sell products online, but overall their sales are generally minor as a percentage of the overall business.

Some of the resistance with traditional insurance carriers to the transition to direct products has come from the independent, general agent, or Broker Dealer side of the business. It wasn’t all that long ago an influential percentage of agents to take the position that if an insurer sold products direct impacting their livelihood, they would either focus on other products or transition to another carrier that didn’t support direct distribution. Now that COVID-19 has created a seismic acceleration of online shopping habits forced primarily due to stay-at-home orders and working from home mantra, life insurers must have an online distribution channel and for those that do they will likely be considering an increase in products options, product simplification and increasing focus for online sales.

The acceleration to direct also means that those who sell life insurance the traditional way will be faced with adapting to the new normal. Gone are the days of a face-to-face meeting around the kitchen table of a prospect or a client. Now it’s a virtual meeting around any table, anywhere, at any time. For the young agent this may be a godsend but for Life industry average aged agent at 60, this may a bit more challenging.

Long-Term Implications & Considerations

- Add more scenario options in your business continuity plans. Have you resolved all your issues from wave 1? Wave 2 is predicted and so is a possibility of a third wave, what is the prolonged impact to your product and distribution model? Business continuity is also an area where regulators may increase scrutiny in the future.

- Anticipate a dramatic increase to the remote workforce of insurers, clients, and prospects. How do you position products, services and technology solutions for the post-COVID future?

- Digital acceleration fuelled by the new remote paradigm. Key systems and services must be automated, and cloud based. Those who don’t digitize risk being left behind.

- Expect capital budgets to reflect a pivot to the digital agenda. Significant increase in product options and product simplification to be sold through direct digital channels.

- Physical contraction of the total number of agents, BD’s, etc. in Life and Annuity distribution sales. This is predicated on the acceleration of direct digital online distribution.

In summary, I will use a line from the Matrix “There's no escaping reason, no denying purpose. Because as we both know, without purpose, we would not exist."- Agent Smith (The Matrix Reloaded). The life industry insurers and agents serve the purpose of developing protection products, matching buyers to the right product for their needs and maintaining strong relationships. The way both evolve digitally within the new post-COVID normal will define the opportunities of the future.