Beijing, China 23 December 2008

Insurance in Hong Kong: Market and IT Overview

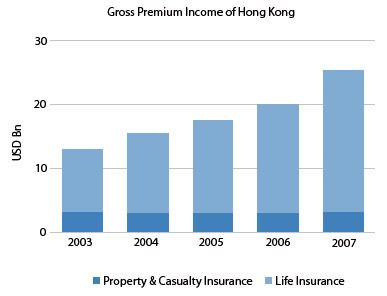

The life insurance business currently dominates Hong Kong’s insurance industry and is a major source of growth, occupying a 70% market share. Property and casualty insurance have experienced a slower growth rate.

The insurance market in Hong Kong has become relatively sophisticated, with a gross premium income of USD25.3 billion in 2007, up from USD13 billion in 2003. The density of Hong Kong’s insurance market (per capita premium income calculated as per total population) is USD2,787.6, ranking 14th in the world, while insurance penetration (the ratio of premium income against the gross domestic product) is 10.5%, making it 8th in the world.

Hong Kong’s insurance market is one of the most open markets. Of the insurance companies operating in Hong Kong, 91 companies were incorporated in Hong Kong, and the rest were from different countries and regions, with a majority being registered in the U.S., Bermuda and the U.K.

I

nvestors have become increasingly prudent about the purchase of investment-linked products due to the influence of US subprime crisis, making traditional life insurance products more likely to attract investors’ favor.

"With

intense competition in the market, companies need to developinsurance types that leverage their specific advantages. Large companies also need to adjust their product structure according to the market,"says Wenli Yuan, Celent senior analyst and author of the report.I

nsurance products have shifted from pure insurance to a combination of protection, saving and investment functionalities. Because there is no restriction on mixed operation, financial institutions that are able to offer comprehensive services in future will occupy a larger share of the market. Meanwhile, the role of traditional insurance agents will gradually change to financial planner as customers’ needs evolve.The 51-page of report includes 4 tables and 27 charts.

A table of contents is available online. of Celent's Life/Health Insurance and Property & Casualty Insurance research services can download the report electronically by clicking on the icon to the left. Non-members should contact info@celent.com for more information.