Comparing Channel Priorities: Europe and the US Revisited

6 January 2011

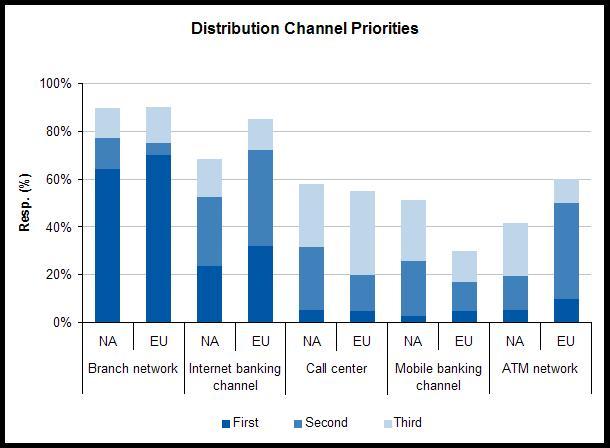

This revisits an earlier blog entry comparing stated channel priorities between US and European banks. I’m encouraged by the spirited discussions it spawned. Some have been critical of bank’s slow – even flawed – approach to multichannel delivery. We agree. There are clear philosophical, generational, organizational and systems barriers to a swift and through transition from a branch centric to multichannel operations. If it were easy, more banks would be there, but it’s an intricate and complex set of challenges in many financial institutions – particularly the large ones. But, that wasn’t the point of the last blog entry. Rather, it meant to simply highlight some differences observed in relative channel priorities between Europe and the US, particularly the mobile and ATM channels. So let’s return to the two questions posed earlier with the benefit of the many that were so kind as to weigh in with their perspectives. 1. Why is the ATM channel such a comparatively high priority among EU banks? 2. Conversely, why is the mobile banking channel such a comparatively low priority? But, first a short digression on the research cited.  In both the Celent and Oliver Wyman research, surveys used a forced ranking technique when inquiring about relative channel priorities. Doing so requires survey respondents to select one answer as first priority, another as second, and so on. The idea is to better distinguish among closely competing priorities. An alternative approach is to invite respondents to rate each channel on a relative priority scale. The risk in doing so is that everything can look “most important”. Neither approach is perfect. In retrospect, I wish we had asked the question both ways. Here’s why. The specific question asked in the Celent survey was: “Given limited resources, indicate the relative priority among your delivery channels based on what gets funded in your organization.” More than a few respondents noted that channel priorities are all very closely grouped, and that coming up with a clear ranking order was difficult. Add to that, within any given financial institution, the stated channel priority might vary internally. That said, the data presented above might overstate (somewhat) the practical priorities among channels. Practically, does it really matter if a given channel is priority #2 versus priority #3 if all requested projects get funded? Perhaps not, but the differences can shed insight into how financial institutions think about the various channels. The Celent survey also asked respondents, “What is driving these priorities?” The response was an open text field, meaning respondents could type in anything they wanted. The answers are revealing. By a large margin, most FIs said that the following drive channel priorities: 1. Customer demand or channel usage (a clear #1) 2. Transaction cost (a distant #2) 3. Competition - FI’s perceived need to react to competition or be disadvantaged (an even more distant #3) Relatively few FIs in Celent’s sample seemed to indicate that channel priorities are based on a long-term strategy. Instead, many seem to be chasing transaction metrics. In other words, the greater the channel usage, the higher its priority. The obvious problem with this approach is that emerging channels will be under appreciated by definition. More strategically driven FIs will choose to get ahead of the usage curve - in fact influence channel usage with innovative delivery mechanisms. Such FIs will likely forever remain in the minority. Back to the questions… So if channel priorities are driven by usage in most FIs, then the differences between Europe and the US might be explained (at least in part) by differences in the payments landscape between the two markets. Cash usage, in particular, remains higher in Europe compared to the US. For example, the Payments Council announced in December 2010 that debit cards have just overtaken cash usage in the UK. Such occurred in the US around 2005 or so. Consequently, ATMs would be logically more highly used in Europe than in the US and a higher channel priority as a result. Additionally, there are more examples of in-branch self-service in Europe than the US, serving to broaden the functional use of ATMs as well as overall usage. What about mobile banking differences? Several weighed in suggesting that Europe has had mobile banking for years, so it’s not as trendy as it has become in the US – and that’s why the mobile channel is a lower priority in Europe. I tend to think that the differences have more to do with how “mobile” is defined in the minds of individual survey respondents. If Europeans consider smart phones as “internet devices”, then the explosive growth of smart phones might be associated with the internet channel – a very close #2 priority behind the branch channel in Europe.

In both the Celent and Oliver Wyman research, surveys used a forced ranking technique when inquiring about relative channel priorities. Doing so requires survey respondents to select one answer as first priority, another as second, and so on. The idea is to better distinguish among closely competing priorities. An alternative approach is to invite respondents to rate each channel on a relative priority scale. The risk in doing so is that everything can look “most important”. Neither approach is perfect. In retrospect, I wish we had asked the question both ways. Here’s why. The specific question asked in the Celent survey was: “Given limited resources, indicate the relative priority among your delivery channels based on what gets funded in your organization.” More than a few respondents noted that channel priorities are all very closely grouped, and that coming up with a clear ranking order was difficult. Add to that, within any given financial institution, the stated channel priority might vary internally. That said, the data presented above might overstate (somewhat) the practical priorities among channels. Practically, does it really matter if a given channel is priority #2 versus priority #3 if all requested projects get funded? Perhaps not, but the differences can shed insight into how financial institutions think about the various channels. The Celent survey also asked respondents, “What is driving these priorities?” The response was an open text field, meaning respondents could type in anything they wanted. The answers are revealing. By a large margin, most FIs said that the following drive channel priorities: 1. Customer demand or channel usage (a clear #1) 2. Transaction cost (a distant #2) 3. Competition - FI’s perceived need to react to competition or be disadvantaged (an even more distant #3) Relatively few FIs in Celent’s sample seemed to indicate that channel priorities are based on a long-term strategy. Instead, many seem to be chasing transaction metrics. In other words, the greater the channel usage, the higher its priority. The obvious problem with this approach is that emerging channels will be under appreciated by definition. More strategically driven FIs will choose to get ahead of the usage curve - in fact influence channel usage with innovative delivery mechanisms. Such FIs will likely forever remain in the minority. Back to the questions… So if channel priorities are driven by usage in most FIs, then the differences between Europe and the US might be explained (at least in part) by differences in the payments landscape between the two markets. Cash usage, in particular, remains higher in Europe compared to the US. For example, the Payments Council announced in December 2010 that debit cards have just overtaken cash usage in the UK. Such occurred in the US around 2005 or so. Consequently, ATMs would be logically more highly used in Europe than in the US and a higher channel priority as a result. Additionally, there are more examples of in-branch self-service in Europe than the US, serving to broaden the functional use of ATMs as well as overall usage. What about mobile banking differences? Several weighed in suggesting that Europe has had mobile banking for years, so it’s not as trendy as it has become in the US – and that’s why the mobile channel is a lower priority in Europe. I tend to think that the differences have more to do with how “mobile” is defined in the minds of individual survey respondents. If Europeans consider smart phones as “internet devices”, then the explosive growth of smart phones might be associated with the internet channel – a very close #2 priority behind the branch channel in Europe.

In both the Celent and Oliver Wyman research, surveys used a forced ranking technique when inquiring about relative channel priorities. Doing so requires survey respondents to select one answer as first priority, another as second, and so on. The idea is to better distinguish among closely competing priorities. An alternative approach is to invite respondents to rate each channel on a relative priority scale. The risk in doing so is that everything can look “most important”. Neither approach is perfect. In retrospect, I wish we had asked the question both ways. Here’s why. The specific question asked in the Celent survey was: “Given limited resources, indicate the relative priority among your delivery channels based on what gets funded in your organization.” More than a few respondents noted that channel priorities are all very closely grouped, and that coming up with a clear ranking order was difficult. Add to that, within any given financial institution, the stated channel priority might vary internally. That said, the data presented above might overstate (somewhat) the practical priorities among channels. Practically, does it really matter if a given channel is priority #2 versus priority #3 if all requested projects get funded? Perhaps not, but the differences can shed insight into how financial institutions think about the various channels. The Celent survey also asked respondents, “What is driving these priorities?” The response was an open text field, meaning respondents could type in anything they wanted. The answers are revealing. By a large margin, most FIs said that the following drive channel priorities: 1. Customer demand or channel usage (a clear #1) 2. Transaction cost (a distant #2) 3. Competition - FI’s perceived need to react to competition or be disadvantaged (an even more distant #3) Relatively few FIs in Celent’s sample seemed to indicate that channel priorities are based on a long-term strategy. Instead, many seem to be chasing transaction metrics. In other words, the greater the channel usage, the higher its priority. The obvious problem with this approach is that emerging channels will be under appreciated by definition. More strategically driven FIs will choose to get ahead of the usage curve - in fact influence channel usage with innovative delivery mechanisms. Such FIs will likely forever remain in the minority. Back to the questions… So if channel priorities are driven by usage in most FIs, then the differences between Europe and the US might be explained (at least in part) by differences in the payments landscape between the two markets. Cash usage, in particular, remains higher in Europe compared to the US. For example, the Payments Council announced in December 2010 that debit cards have just overtaken cash usage in the UK. Such occurred in the US around 2005 or so. Consequently, ATMs would be logically more highly used in Europe than in the US and a higher channel priority as a result. Additionally, there are more examples of in-branch self-service in Europe than the US, serving to broaden the functional use of ATMs as well as overall usage. What about mobile banking differences? Several weighed in suggesting that Europe has had mobile banking for years, so it’s not as trendy as it has become in the US – and that’s why the mobile channel is a lower priority in Europe. I tend to think that the differences have more to do with how “mobile” is defined in the minds of individual survey respondents. If Europeans consider smart phones as “internet devices”, then the explosive growth of smart phones might be associated with the internet channel – a very close #2 priority behind the branch channel in Europe.

[...] the Customer In a previous post we addressed the all too common method of determining channel priorities – following the [...]