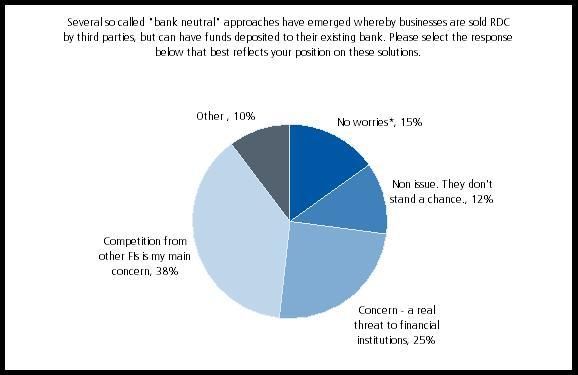

Since remote deposit capture (RDC) made its debut several years ago, 90% of client adoption has been at the hands of financial institutions offering generic solutions. Once primarily aimed at retaining treasury management clients, 60% of financial institutions surveyed in August 2009 now cite deposit gathering the primary objective of RDC. But alongside banks, non-financial institutions have embraced RDC and are entering the market with bank-neutral solutions. The most recent example is Intuit’s Check Solution for QuickBooks introduced with the latest release of QuickBooks in late September. These channels are emerging for one compelling reason: opportunity. Celent sees three specific advantages inherent in many of the non-financial institution sponsored solutions. 1. Solution Differentiation. Third party software vendors can provide highly integrated workflows beyond the generic solutions most financial institutions are likely to deploy. Integrating RDC solutions with vertically focused applications provides conspicuous advantages. 2. Developed Sales Channels. Demand for RDC is greater than financial institutions collective ability and/or willingness to fulfill. Third parties seeing this opportunity are maneuvering to fill demand. In many cases, each of these third parties bring with them substantial client bases, brand equity and some degree of customer loyalty. Consider Intuit with its 4+ million QuickBooks customer base. 3. Customer Preference. A number of scenarios are friendly to bank-neutral solutions. Large property management firms with properties in multiple states, for example, are compelled to have banking relationships in each state. A single, bank-neutral solution is likely preferable to buying several solutions, one from each bank. The prevailing attitude among financial institutions concerning these emerging third-party solutions is casual. Among respondents to Celent’s August financial institution survey, only 25% expressed concern. 15% welcomed the advent of third-parties who would do the “heavy lifting” as long as the bank retained the deposit relationship.  Is this an appropriate response given the market position of Intuit? We think so. The compelling value of Intuit Check Solution for QuickBooks doesn’t lie in reducing trips to the bank, but in making all aspects of receiving and posting payments fast and easy. RDC has become one of many integrated components in the QuickBooks payments ecosystem. In this regard, banks can’t compete using generic RDC solutions. Resistance is futile. Banks can learn from Intuit by integrating RDC into applications they do own – internet and mobile banking solutions. If it is all about deposits, then banks would do well to prepare for the likelihood that the majority of deposits may soon be collected via RDC – directly or via third parties.

Is this an appropriate response given the market position of Intuit? We think so. The compelling value of Intuit Check Solution for QuickBooks doesn’t lie in reducing trips to the bank, but in making all aspects of receiving and posting payments fast and easy. RDC has become one of many integrated components in the QuickBooks payments ecosystem. In this regard, banks can’t compete using generic RDC solutions. Resistance is futile. Banks can learn from Intuit by integrating RDC into applications they do own – internet and mobile banking solutions. If it is all about deposits, then banks would do well to prepare for the likelihood that the majority of deposits may soon be collected via RDC – directly or via third parties.