Here Comes the Assualt on Overdraft Fees

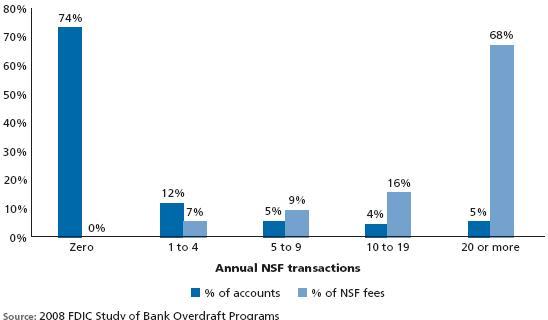

[/caption] The report concludes: “Institutions that can put a definitive fee transformation strategy in place are likely to find they are well-positioned for the future. In contrast, institutions that remain exposed to the choices of regulators and consumers do so at their own peril.” It might be too late. A regulatory imperative to act may be close aboard. The Obama administration has proposed the creation of a new agency empowered to write and enforce rules protecting consumers in financial transactions, removing that power from banking regulators. But as debate for that idea simmers, more proximate danger lies ahead in the form of legislation specifically targeted at outlawing courtesy overdrafts without consumer opt-in. According to the Washington Post, Sen. Christopher J. Dodd (D-Conn.) plans to introduce legislation requiring banks to get permission from customers, rather than allowing overdrafts automatically. If customers decline and then try to overspend, the transaction would be rejected. A similar bill is pending in the House. But hasty changes to bank’s DDA pricing policies could be risky. A careful strategy is needed – and time is of the essence it appears. Creative solutions may be the answer. Several very interesting and creative products have emerged in 2009 that will likely put the competitive squeeze on banks that remain reliant on NSF fee revenue. These deserve a close look.

[/caption] The report concludes: “Institutions that can put a definitive fee transformation strategy in place are likely to find they are well-positioned for the future. In contrast, institutions that remain exposed to the choices of regulators and consumers do so at their own peril.” It might be too late. A regulatory imperative to act may be close aboard. The Obama administration has proposed the creation of a new agency empowered to write and enforce rules protecting consumers in financial transactions, removing that power from banking regulators. But as debate for that idea simmers, more proximate danger lies ahead in the form of legislation specifically targeted at outlawing courtesy overdrafts without consumer opt-in. According to the Washington Post, Sen. Christopher J. Dodd (D-Conn.) plans to introduce legislation requiring banks to get permission from customers, rather than allowing overdrafts automatically. If customers decline and then try to overspend, the transaction would be rejected. A similar bill is pending in the House. But hasty changes to bank’s DDA pricing policies could be risky. A careful strategy is needed – and time is of the essence it appears. Creative solutions may be the answer. Several very interesting and creative products have emerged in 2009 that will likely put the competitive squeeze on banks that remain reliant on NSF fee revenue. These deserve a close look. - ING Direct now offers an online-only interest-bearing account it calls Electric Orange with free overdraft protection

- BancVue offers a turn key rewards checking product that is taking off among community banks and credit unions. The product, Kasasa, comes bundled with marketing, training and consulting aimed at maximizing the impact of the new approach.

- USAAis promoting its free checking product with free overdraft protection, free limited ATM withdrawls and the ability to deposit checks into your account with a home scanner or even an iPhone.

- Bank of America, CitiBank, Wachovia and others are promoting creative savings accounts which when bundled with DDAs will likely grow average deposit balances.

Comments

-

Finally, I can't believe this is just happening now. And in the past the programs were mandatory(at least at bank of america). How crazy is that? They are basically lending you money without your permission. sometimes the interest rates on these "loans" are in the thousands.

and for those that say i need to pay better attention to my bank account balance. Go f___ yourself. I refuse to waste my life ever thinking about money.

-

These fees absolutely became predatory. They can quickly turn what could and should be a minor mistake into a major obligation that can take months for the consumer to work their way out of. By taking the fee first, what might have been one overdraft becomes several, each with its own fee, causing more overdrafts, etc.

While this has never been an issue for me, both of my now young adult children have gotten caught in overdraft buzz-saw. Our daughter was hit with 8 $35 fees before she got the first notice. All but the first one would not have been NSF except for the fees, since she made a deposit that promptly disappeared without her knowledge.

Greed always eventually comes back to haunt you. Just ask the sub-prime lenders.

I think the notion of an automatic "courtesy overdraft" that charges outrageous fees for the courtesy is obnoxious. If I don't have sufficient funds in my account, don't put the transaction through. I fully support banks being mandated to have an opt-in requirement before implementing an overdraft protection service.