Countries and regions around the world are accelerating efforts to evolve and advance financial market infrastructure. Against this backdrop, it is incumbent on Japan’s Zengin System to move beyond merely offering a 24/7 realtime payment infrastructure. Instead, through providing value-added services and connecting non-banks (payment service providers) and their diverse range of service offerings, the focus should be on evolving the next-generation payment system and fostering an arena for financial service innovation in next-generation financial services.

Japan was ahead of the curve when it launched the first iteration of the Zengin System in 1973, processing real time payments—albeit limited to weekday and daytime operation. In October 2018, the Zengin More Time System launched, making real time payments possible around the clock. Similarly, other markets globally have updated payment infrastructures to support real time, around-the-clock payments—with the UK doing so in 2008 and North American and major European countries and regions following suit by late 2017.

In Japan, most depository financial institutions, apart from a few banks without retail services, participate in the Zengin More Time System, which provides 24/7 real time payments. In North American and European markets boasting similar levels of service, a central challenge is increasing the number of connected institutions and transaction volumes handled. In the United States, the around-the-clock Clearing House Real-Time Payment system currently connects to approximately only approximately 5% of US banks. Meanwhile, in other countries, only a minority of large financial institutions are directly connected. In these markets, many small and medium-sized banks are limited to indirect connections to the banking system via other banks’ direct connections. Moreover, the use of the Zengin System differs from other markets in that it boasts an overwhelmingly larger volume—both in terms of transaction volume and in terms of transaction numbers and financial value transacted.

In 2019, Japan’s payment infrastructure marked major milestones indicative of future trends. These landmark developments came five years after the 2014 establishment under the Financial Services Agency’s Financial System Council (FSC) of a study group tasked with mulling advancements in the payments sector. The group generated research and reports on future directions and challenges, including the “Strategies for Reforming Japanese Payment Systems” report (December 2015) and the SWIFT Whitepaper, “Japan’s Payments Systems: Digitisation, Globalisation & Innovation” (May 2016). Major milestones logged in 2019 included the following:

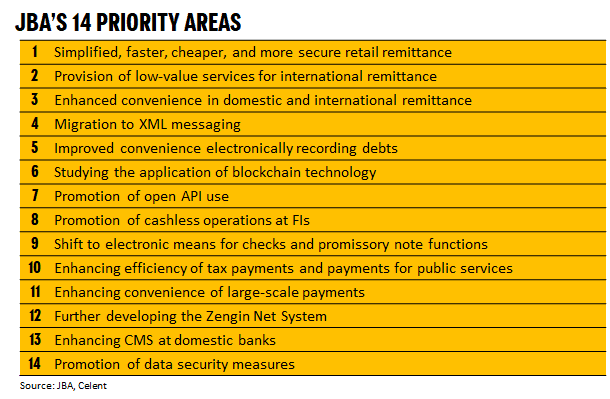

- Release of Japanese Bankers Association (JBA) 14 priority areas under the FSC

- FSC report by a working group reviewing the legal infrastructure for payment and financial services legislation