買い物時の口座間決済はクレジットカードに取って代わるか?

2018/08/22

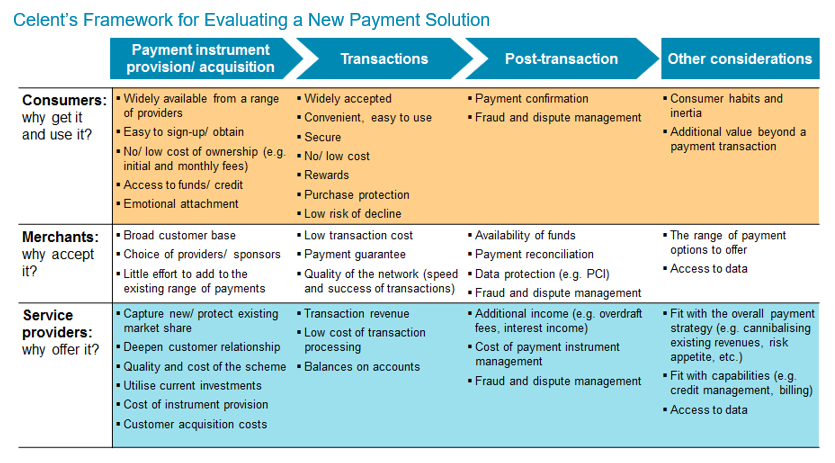

口座間決済 (A2A《Account-to-Account》Payments)が成功するには、カードから学ぶべきことがたくさんある。

Key research questions

- リテールにおけるA2A決済の例は?

- A2A決済がカードから学べることは?

- A2A決済が最初に成功するリテール領域は?

Abstract

A2A決済は消費者により多くの選択肢を提供するだろう。しかし、カードおよびカード型デジタルトークンがすぐになくなることはないだろう。

欧州決済サービス指令 (PSD2, The Second European Payment Services Directive) は、顧客銀行口座からの直接の支払いを目的として、決済指示サービス提供者 (PISP, Payment Initiation Service Providers)として認可されるサードパーティのための基礎を築いた。ショッピング、特にオンラインショッピングで利用でき、実店舗でも利用できる可能性があるということで、欧州ではA2A決済の気運が高まっている。

セレントは、A2A決済が買い物時の現実的な選択肢になり得るということは認めるが、特にカードのシェアが高い市場においては、A2A決済が成功するために解決すべきいくつかの障害があると考える。

本レポートでは、A2A決済とカード決済の相対的利点を調査している。更に、A2A決済がカード決済に対抗するために何が必要かを考察している。