On 12th June 2023 (just yesterday), Nasdaq announced their intentions to acquire Adenza (which itself was created from the coming together of Calypso, a provider of front-to-back trading technology; and Axiom SL, a regulatory reporting solution provider).

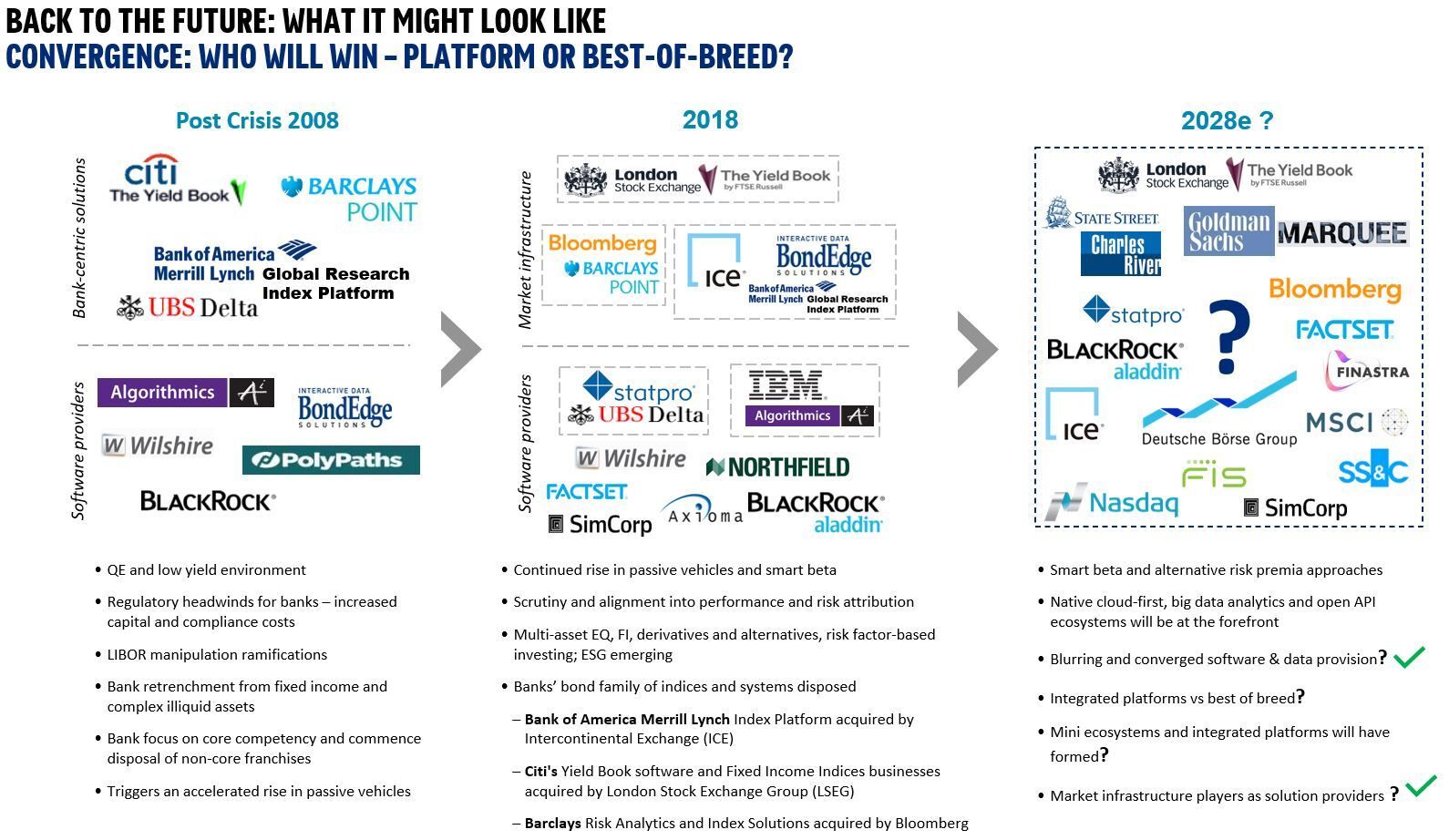

My reaction to this development harks back to a number of reports and roundtables we did with our clients in Q1 2019. Back then, we anticipated specific convergence themes (as shown below). One of them was financial market infrastructure players as (software) solution providers. At that time, we anticipated "market infrastructure players as solution providers" to play out in 2028 — therefore, whilst this Nasdaq-Adenza transaction wasn't a surprise, the timing has happened faster than we had anticipated!

Up to now, we have seen (are seeing) the rapid rise of market infrastucture players as solution providers, for instance:

- London Stock Exchange Group (LSEG) --> Refinitiv, Acadia, Tora

- Deutsche Borse --> SimCorp, Axioma (Qontigo), ISS

- Intercontinental Exchange (ICE) --> Black Knight, Urgentem, Trayport

- Nasdaq --> Adenza (Calypso and Axiom SL), Verafin, Solovis, eVestment

Learning from a backstory will give us a clue to the future

With the above, there is a backstory to these developments, which Celent clients will know from their access to our market studies. The genesis of the the landscape of consolidation and convergence, in my view, goes back more than thirteen years ago when the global financial crisis hit. This “backstory” here is tied to the sell side’s post-crisis actions and dynamics, which in turn, is playing into the reconfiguration of the financial industry's technology value chain — resulting in the manifestation of what we see happening today. This you seldom hear about in totality, and looking at past developments, I believe will give us clues to the future for sellside and buyside buyers of technology, as well as solution providers. Let me explain more.