How Financial Institutions Are Responding to COVID-19 Constraints

Many lenders adapted quickly to new customer channel preference (digital versus branch), employee work from home (WFM) requirements, new IT security issues, and loan forbearance programs. Urgent technology gaps were closed to keep the business running, and digital automation priorities generally increased given the unforeseen outlook as to how long it would take for the physical world to return to normal. Financial institution response sometimes varied by institution size:

·Larger, more sophisticated, and/or better run institutions have been able to accelerate the pace of process and technology change.

·Smaller or less sophisticated institutions with older technologies are transforming at a slower pace. The backlog of urgent project has only increased.

·Reliance on trusted third-party technology partners has increased.

A key question in 2021 is, where are the retail lending market trends, where are they heading in the future, and how should financial institutions continue to adapt?

Retail Lending Market Trends

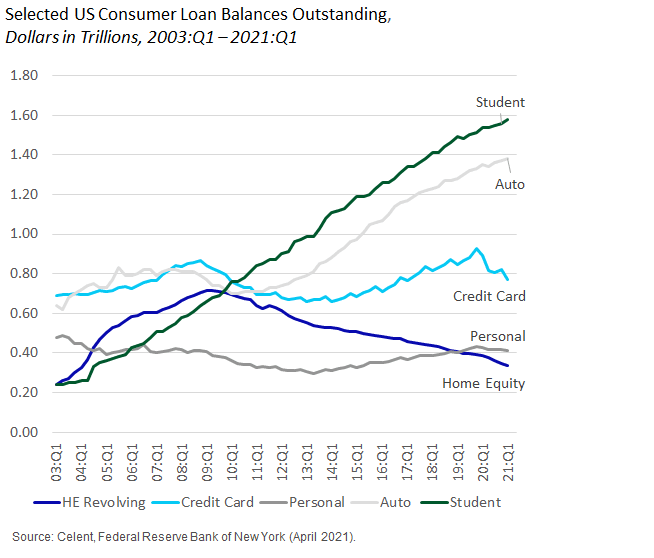

Figure 1 charts US retail loan growth from 2003 to 2021.

There are four key points to emphasize from the chart:

·Automobile and student lending continue to growth through business cycles, including the past two recessions

·Credit card lending goes up and down with the economy

·Personal lending is the smallest lending category although it has grown slowly but steadily for the past eight years

·Home equity lending remains on a decade-long, downward trajectory since the subprime mortgage crisis. Strong economic growth has not changed this pattern.

Where is Each Retail Loan Origination Market Heading?

Retail loan origination includes numerous distinct lines of business. Although they have many similarities, there are also distinct differences in market drivers, growth trends, customer requirements, and technology use:

Automobile lending: used automobile purchases are increasing and prices are increasing. This is occurring because affordability is an issue for consumers hurt by the pandemic.New auto sales have been relatively flat for the past four years but are holding up in 2021 after rebounding from a significant dip in early to mid-2020.Total auto sales are likely to growly slowly as more people going back to work.

Student lending: this is the largest lending segment in terms of size and rate of growth. However, approximately 90% of student loans outstanding are government loans that are originated, owned, and serviced by state and federal governments. Financial institutions primarily play a role in the smaller private student loan market for undergraduate students, graduate students, and the parents of students.

Credit Card Lending: new card lending has recovered somewhat from the drop in 2020, but many consumers are wisely being more conservative in their credit use. Loan demand is also down due to more people working from home and spending more time at home. This downward trend will reverse somewhat as more consumers begin to spend more time away from home.

Personal Lending: there is growth and innovation in unsecured personal lending, but risks are relatively high and lenders need to assess the credit and fraud risk of loan applicants.In addition, ‘buy now, pay later’ (BNPL) lenders are flooding the market with short-term personal loans that compete with traditional loan products and are a substitute product for credit cards.

Home Equity Lending: there are positive and negative dynamics for fixed-rate home equity loans (HELs) and lines of credit (HELOCs). With more consumers spending more time at home for work and leisure, some are borrowing to improve and/or expand their homes.Other homeowners have become more financially conservative, and are not taking out new HELs or HELOCs, are not using existing HELOCs except in case of emergency, or are paying down existing lines of credit. This downward trend may reverse in the near future as recent first-time home buyers build equity and seek to improve their property in greater numbers.

What Strategies Should Retail Lenders Implement?

Lead generation, customer relationship management, digital engagement, and efficient back-office processing are more critical than ever before in an era where virtually all lenders sell through digital channels. Moreover, the interest rates for many loan product types increased in 2021, which combined with more fiscally conservative consumers restricts loan market size and intensifies competition.

Consumers need financial institution support through their lifetime of saving, borrowing, asset accumulation, and payments cycles. In terms of customer needs and lender actions:

·Consumers—especially those that are suffering through the pandemic—need better personal financial management solutions, and financial institutions need better customer 360 software and analytics to deliver the right information, advice, and product recommendations to the right customer at the right time.

·Consumers that have thrived financially through the pandemic have increased their savings as they’ve spent less.Financial institutions can either offer them higher yield investment vehicles for that spare cash, or cross-sell retail products, travel, or other services and offer financing to pay for them.

Next Steps

For more information on retail lending trends, strategies and technology, contact us and see: Top Trends in Global Retail Lending 2020-2021: COVID-19 Mandates Faster Transition of Business and Technology Strategies