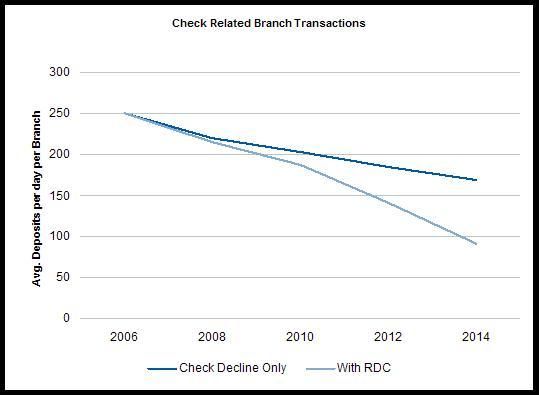

JPMorgan Chase has apparently launched a targeted campaign to boost its Chase Quick Deposit, remote deposit capture client base with some unusually rich discounts. Specifically, Chase is offering two years of free Chase Quick Deposit (normally $50/mo, plus the $855 Panini MyVisionX scanner to power it. Total retail value = $2,055. Like any offer, there are specific requirements to this offer. -- Users must deposit at least 10 checks per month -- Offer is valid for new Chase Quick Deposit users only -- $500 cancellation fee if discontinued within 12 months -- Offer good through July 31, 2010 Some banks may balk at such aggressive pricing in the small business RDC segment. What is Chase thinking? I can guess – and they’re on to something. The minimum monthly check deposit requirement is a pretty good clue. According to its 2009 Annual Report: • Last year, 61,000 people in 5,154 Chase branches in 23 states served more than 30 million U.S. consumers and small businesses • Retail operations teams processed 700 million teller transactions • Chase added 2,400 branch sales staff last year – personal and business bankers, mortgage officers and investment representatives – to better serve its customers. What is Chase doing? It is becoming more efficient, while strategically transitioning its branch network from transaction processing centers to sales and service centers. Significantly growing its small business RDC customer base – even without associated fee revenue – can pay large dividends to Chase. How? By reducing the number of small business branch deposits. Self-service deposits are less costly to process than paying tellers to do them. The graph below depicts Celent’s estimate of declining check transaction volume in the average US branch with and without small business RDC assistance. [caption id="attachment_1562" align="aligncenter" width="539" caption="Declining Check Transaction in the Branch"] [/caption] So, the robust promotion of Chase Quick Deposit reflects both a shift in RDC strategy (from PxV product revenue to a self-service reason for being) and a shift in branch strategy (from transaction centers to sales & service centers). Chase serves as a great example for other banks to follow. Celent is currently researching the evolution of North American branch infrastructure. Weigh in on the link below, and we’ll send you a complimentary executive summary of the results. http://www.surveymonkey.com/s/Branch

[/caption] So, the robust promotion of Chase Quick Deposit reflects both a shift in RDC strategy (from PxV product revenue to a self-service reason for being) and a shift in branch strategy (from transaction centers to sales & service centers). Chase serves as a great example for other banks to follow. Celent is currently researching the evolution of North American branch infrastructure. Weigh in on the link below, and we’ll send you a complimentary executive summary of the results. http://www.surveymonkey.com/s/Branch