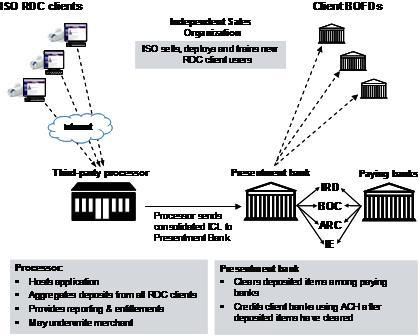

Remote deposit capture (RDC) has taken financial institutions by storm. In just over three years since its debut, more than half of all US banks have adopted solutions, along with a significant number of credit unions and retail brokerages. But this extraordinary adoption among financial institutions has thus far led to comparatively tepid client adoption.Based on multiple research efforts, we can conclude that this lopsided picture is not the result of an exaggerated view of the market opportunity. The rationale for such historically temperate sales and marketing efforts among banks is defensible in many cases. But RDC is no longer a nascent market. The time has passed for financial institutions to take a more aggressive stance. RDC: The Perfect ISO Opportunity? The credit card business isn’t what it used to be. Market growth has cooled, with stiff competition and challenging margins. Independent sales organizations (ISOs) appear more than eager for the opportunity to expand their product lines beyond card services. For ISOs, the opportunity is two-fold: cross-selling RDC to current merchants and expanding reach beyond card-heavy clients into entirely new markets within existing geographies. From a market development perspective, the scenario is close to ideal. Compared to financial institutions, ISOs appear to be in a good position to act on the opportunity. But, how is this going to work? ISOs will need to provide remote deposit capability that allows businesses the ability to maintain existing bank relationships. Ironically, that won’t likely be done using the image based processing that Check 21 envisioned. That’s because most banks aren’t ready to receive image cash letter (ICL) deposits, and those that are limit such arrangements to large volume clients because of the time-consuming file certification and management overhead involved. Instead, ISOs are likely to utilize a third party aggregator and a presentment financial institution, into which all the collective small business check deposits will be sent via image. Then, the presentment financial institution will settle with multiple banks of first deposit using ACH credits, while presenting items to paying banks via image exchange (Figure 1).In so doing, banks of first deposit maintain deposit relationships, businesses enjoy the benefits of remote deposit, presentment banks earn fee revenue, and ISOs do what they do best – sell and service clients. It might actually work.  Not All Roses As attractive as RDC may be for ISOs, success won’t be a slam dunk. ISOs don’t know check payments like they know cards. Thorough training will be an imperative. Additionally, the RDC value proposition is highly varied among market segments. Many ISOs enjoy specialization, and won’t find their target market segments a good fit for RDC. Unlike merchant acquiring, RDC is not required for check acceptance. Some segments (restaurants, for example) will make lousy targets for RDC. ISOs will need to sort this out. Secondly, the processing model presents significant return item risk to presentment financial institutions. To mitigate this risk, presentment banks will wait until all funds are good before originating the ACH credit to banks of first deposit. Client funds availability will likely be delayed compared to bank direct RDC models. It’s too early to tell if this will be a factor in selling. But, the biggest risk to the success of ISO RDC delivery is the business model itself. Today’s bank direct RDC pricing leaves plenty of room for ISO profit. But, if free scanners and lower monthly maintenance fees become the norm, there may be insufficient profit opportunity left for an ISO in the middle. Will ISOs claim the RDC market as they have done with cards? It’s simply too early to tell. Many banks regret what has occurred with merchant acquiring and won’t let that happen again with RDC. But that won’t stop ISOs from getting a foothold in this large and diverse market. Some banks, those primarily seeking core deposit growth, welcome third party involvement to take care of the hardware deployment and provisioning. So what can be predicted with certainty? Just this: it’s going to be fun to watch!

Not All Roses As attractive as RDC may be for ISOs, success won’t be a slam dunk. ISOs don’t know check payments like they know cards. Thorough training will be an imperative. Additionally, the RDC value proposition is highly varied among market segments. Many ISOs enjoy specialization, and won’t find their target market segments a good fit for RDC. Unlike merchant acquiring, RDC is not required for check acceptance. Some segments (restaurants, for example) will make lousy targets for RDC. ISOs will need to sort this out. Secondly, the processing model presents significant return item risk to presentment financial institutions. To mitigate this risk, presentment banks will wait until all funds are good before originating the ACH credit to banks of first deposit. Client funds availability will likely be delayed compared to bank direct RDC models. It’s too early to tell if this will be a factor in selling. But, the biggest risk to the success of ISO RDC delivery is the business model itself. Today’s bank direct RDC pricing leaves plenty of room for ISO profit. But, if free scanners and lower monthly maintenance fees become the norm, there may be insufficient profit opportunity left for an ISO in the middle. Will ISOs claim the RDC market as they have done with cards? It’s simply too early to tell. Many banks regret what has occurred with merchant acquiring and won’t let that happen again with RDC. But that won’t stop ISOs from getting a foothold in this large and diverse market. Some banks, those primarily seeking core deposit growth, welcome third party involvement to take care of the hardware deployment and provisioning. So what can be predicted with certainty? Just this: it’s going to be fun to watch!