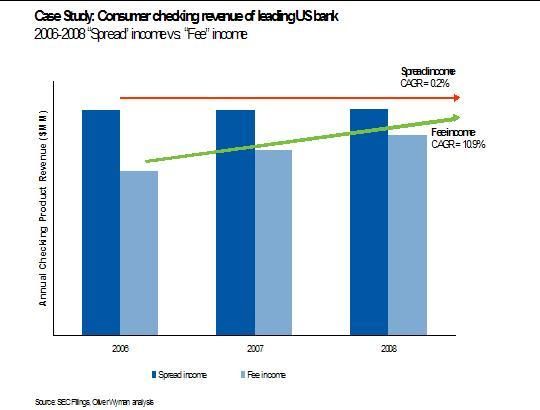

In today's New York Times, the paper announced that Wells Fargo had lost a Federal Court ruling to the tune of $203 million. Wells Fargo, like most other large banks, processes checking and debit transactions from largest to smallest, rather than in the order received. There are a number of rationales for this policy. One is that it is likely that the larger check is for a more important payment such as a mortgage payment or utility payment. Small checks would be to other service providers. The flaw in the logic comes in if the bank is charging overdraft fees and paying all three transactions regardless of the order processed. There is no customer benefit to processing largest checks first if all three are paid regardless. This practice also maximizes overdraft revenue, which is a huge chunk of the fee revenue that has been driving free checking as shown below. [caption id="attachment_1705" align="aligncenter" width="540" caption="Fee income is increasing faster than spread income"] [/caption] Let's review how this works. Suppose I have $100 in my checking account and write three checks (or had three debit card transactions) for $40, $50 and $120, in that order. If these checks were processed in the order received, the checks for $40 and $50 would clear and the check for $120 would generate a single overdraft charge. If the checks are processed in descending order, the check for $120 would generate an overdraft as would the $40 and $50 checks for three overdrafts rather than one. The changes to Reg E that become effective for existing customers on August 15 will reduce fee revenue, as I have laid out in the Celent report Reg, Reg, Go Away. If this ruling stands, it will put another nail in the coffin of free checking. Banks will need to respond in innovate ways, some of which I have laid out in this same report.

[/caption] Let's review how this works. Suppose I have $100 in my checking account and write three checks (or had three debit card transactions) for $40, $50 and $120, in that order. If these checks were processed in the order received, the checks for $40 and $50 would clear and the check for $120 would generate a single overdraft charge. If the checks are processed in descending order, the check for $120 would generate an overdraft as would the $40 and $50 checks for three overdrafts rather than one. The changes to Reg E that become effective for existing customers on August 15 will reduce fee revenue, as I have laid out in the Celent report Reg, Reg, Go Away. If this ruling stands, it will put another nail in the coffin of free checking. Banks will need to respond in innovate ways, some of which I have laid out in this same report.