According to the International Monetary Fund, Asia accounts for nearly two-thirds of global growth, and the region remains the world’s most dynamic by a considerable margin. The Asia-Pacific region also dominates global banking, with approximately 40% of total bank assets and profits generated in the region.

Against this backdrop, I’m finishing up a research project to detailing APAC corporate banking, drilling into operating income performance, segment revenue, technology trends, and opportunities and challenges. The report highlights trends in China, Japan, India, South Korea, Australia, Indonesia, Taiwan, Thailand, Hong Kong, Singapore, Vietnam, and Malaysia (listed in 2017 GDP order). The results will soon be published in an upcoming Celent report, Connected Corporate Banking in Asia-Pacific.

In the meantime, here is a preview of key findings:

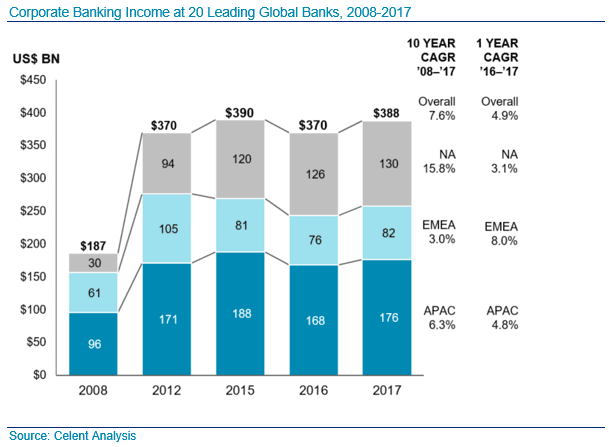

1. Corporate banking operating income: In 2017, corporate banking was responsible for 39% of overall operating income across the 20 banks in Celent’s analysis. Looking at these banks by geography, APAC corporate banking represents 45% of total operating income.

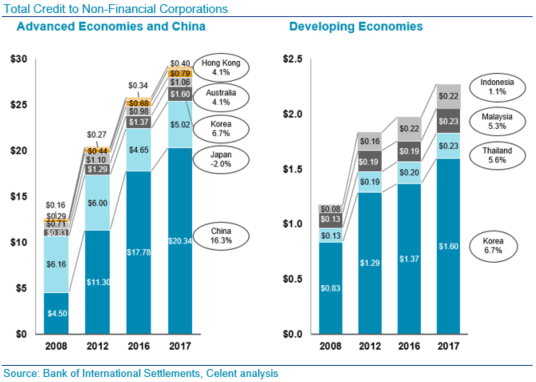

2. Commercial lending growth: Looking at data from the Bank for International Settlements (BIS), credit to corporations across the region grew more than 12% since the 2008 financial crisis. The fastest growth occurred in China, growing more than 16%, boosted by central bank management of interest rates and lending caps. Japan lost ground, with total credit falling 2%, largely as a result of the central bank’s purchases of corporate bonds at negative interest rates. The shift of corporate funding to bond issuance and away from bank credit hurts banks’ lending margins and thus profitability.

3. Global transaction banking revenue: Oliver Wyman develops GTB revenue pool estimates and forecasts annually from its comprehensive sizing database. 2017 was a very good year for cash management and payments, growing more than 8%. Over the next 5 years, Oliver Wyman forecasts that GTB revenue growth will accelerate to 5%. As shown below, APAC continues to dominate both revenue share and growth, with 6% CAGR from 2010 to 2017, and no signs of slowing down with an additional 6% growth forecast through 2022.

4. Key trends: Four key trends are driving corporate banking technology investment in the Asia-Pacific region:

• Socioeconomic factors.

• Regulatory and industry initiatives.

• Customer experience.

• Emerging tech.

Best practice banks are leveraging technology to differentiate themselves in the Asia-Pacific region, increasing their share of the corporate banking revenue pool. They are competing with the large globals, who have mature digital strategies for corporate banking, manifested in their integrated portal offerings and solution sets across the corporate banking product spectrum. They are also competing with a handful of banks headquartered in the region who have staked their futures on innovative solutions using emerging technologies.

Be on the lookout for the Celent report “Connected Corporate Banking in Asia-Pacific” to gain more insight into the region’s opportunities and challenges, as well as how banks can use disciplined and focused execution to gain competitive differentiation. Also, the Celent Corporate Banking Team will be at SIBOS; and Alenka Grealish, Gareth Lodge, and I look forward to meeting with you.