Celent recently published a report titled CIO Priorities in Capital Markets Infrastructure: Technology Empowers New Models that analyzes technology trends among market infrastructure (MI) providers based on a survey of 20 leading players across the globe. The majority of the MIs in our study have undertaken significant upgrades, core transformations, and legacy modernization in the past five years. A large part of this spending can be attributed to business and regulatory changes. For many MIs this is also accompanied by general stability or improvement in its macro-climate, which some said is critical for undertaking major tech upgrades. They expect the next cycle to occur in four to five years. Therefore, most exchanges expect only incremental growth in their technology spending before then, but no one mentioned reducing spending.

However, we see a shift in spending breakdown between running the business and changing the business, especially with the conclusion of regulatory projects and intensifying focus on new technology adoption. Participants mentioned spending around 5% of their technology budgets on changing the business in the past, but that is likely to go up to 20%–25%, or even 50% in the case of the bigger market infrastructures that can amortize their fixed costs more efficiently.

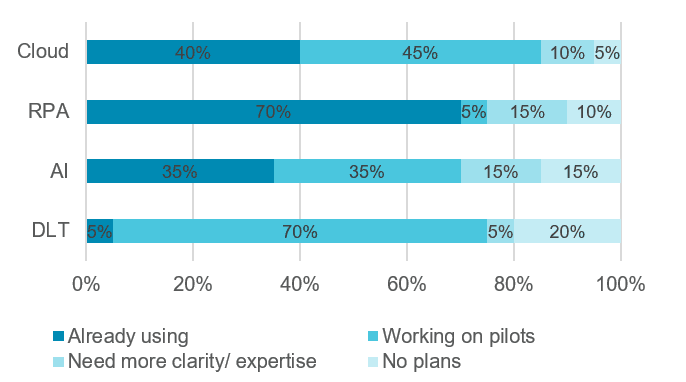

Growing Interest in Technology Innovation

Leading MIs are approaching new investments with the aim of further reducing operational costs through process efficiencies, optimization, cheaper hardware, and even offshoring or young-shoring. Some are also developing new business solutions and delivery models that can generate additional revenue. Specifically, a lot of experimentation is going on in the areas of cloud adoption, data lake usage, machine learning for building analytics tools, etc. From a functional standpoint, the main areas of new investments are in trade analytics, clearing, risk management and post-trade services, which are seeing significant new investments. Specific initiatives include sentiment analysis on retail investor behavior, automated research aggregation, distribution of broker-neutral research, transaction cost analytics in non-equity asset classes, transaction reporting, cross margining solution, triparty collateral management solution, and reconciliation of OTC trades, securities, fees and commissions, and so on.

Most MIs have historically developed the absolute core in-house. While some leading players still do that, it is becoming very costly for smaller players to adhere to international standards and continuously upgrade as per regulatory changes. Even leading players are now more open to buy core platforms from third party providers and undertake significant customization with in-house resources. Especially when old platforms come close to the end of their lifecycle, or new asset class support is developed, leading players prefer the buy-and-customize approach over reinventing the wheel. MIs across the world prefer to work with international vendors because their solutions are recognized and accepted by market participants and regulators in other countries, and are also compliant with the latest standards and practices.