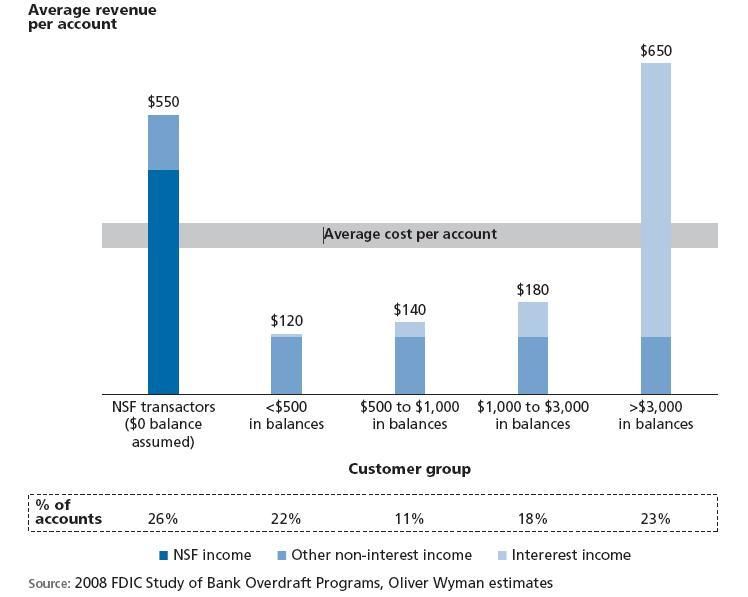

The inverted bell shaped curve in DDAs.

The most profitable DDA customers are those at the top of the scale who keep large balances and provide low cost deposits, and those at the bottom of the scale who keep very low balances and generate NSF or overdraft fees. They subsidize the other half of customers in the middle who neither keep large balances nor bounce checks.

Why is this important? Competitors are slowly chipping away at both the top and the bottom of the markets. Direct banks are offering high rates to lure away the balances. Most people know about ING Direct or E*Trade Bank. On the bottom end of the balances the General Purpose Reloadable (GPR) card is making inroads and the 100 pound gorilla of mass retailing, Wal-Mart is moving into this space in a big way with their 3/3/3 pricing: That’s $3 to buy the card, $3 to load cash onto it, and $3 per month. With Wal-Mart’s aggressive pricing and huge retail presence, this move could move GPR cards out of the ethnic neighboroods and niche markets and into the mainstream. Main street banks should take note.

A no-brainer for banks is to offer GPR cards to those who don’t qualify for a checking account. Do banks want to wait for Wal-Mart to take their customers or move them to a more suitable product themselves? Wal-Mart is persistent and wants to be a power in financial services for years. They don't want all your customers, just the 25% with low balances and high profit.