Although 2020 has certainly been a unique year it hasn’t put a damper on the momentum that has been building over the last few years in the Life and Annuity policy administration system (PAS) space.

The North America-based vendors of core systems for Life and Annuity insurers have drawn more than their share of attention based on recent acquisition activity. In addition, the pent-up demand from insurers investing in new platform technology is driving investments for established vendors and fueling funding for new entrants into an already crowded market.

Since the collapse of interest rates in 2009, Life and Annuity insurers, for the most part, held off on making investments in big ticket items like PAS for many years. Fast forward to the last few years, Life and Annuity insurers have made the decision to invest in upgrading for the digital age. As a result, there has been a tsunami of acquisition activity, new entrants and established vendors investing heavily on revamping their offerings.

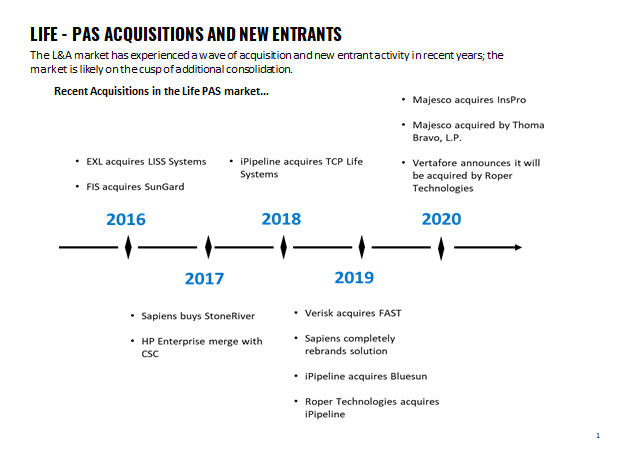

Below is just a sample of activity that has taken place over the last few years in the Life and Annuity system market…

The sustained wave of M&A activity demonstrates how vendors and investors are responding to that demand in the Life and Annuity PAS market. It also may indicate the how vendors and investors perceive increasing their value to insurance companies with providing a full suite of solutions.

The M&A activity has been a mix of public and private equity (PE) backed transactions. iPipeline, as an example, was part of the PE portfolio of Thoma Bravo before being acquired by Roper Technologies which is public. Thoma Bravo filled the portfolio gap with the recent acquisition of Majesco. StoneRiver and FAST were also private before being acquired by public companies Sapiens and Verisk respectively. This M&A activity would indicate many see a sustained need for life and annuity insurers to replace antiquated technology for years to come.

The same goes for the new entrants in the field. New PAS providers and low-code/no-code platform providers are invading the space. Calcfocus with Achieve, iPipeline with SSG Digital, Penn River, Socotra and Unqork just to name a few.

What are the benefits to insurers from all this activity?

- Vendors making significant investments to broaden, deepen and digitize capabilities

- Enable North American insurers to expand digital roadmaps

- More options and within those option more robust functionality

- Expanded vendor services beyond just PAS such as data and analytics

- Rapid advances in the application of emerging technology

- Increased product efficiency and configurability

… And the benefits for the portfolio owners and vendors in the space?

- Increasing revenue from existing customers with an expanded portfolio of offerings through the associated M&A activity

- Opportunity to expand market share by gaining new customers

- Expense control through the application of emerging technologies

- Increase customer satisfaction through continuous investment

This all adds up to be a one of the best times for insurers who are shopping for a new PAS solution. An evolving array of choices, heavy investments in core systems, expanding portfolio of solutions, and a plethora of new entrants all make for a good barometer of the health of the market, at least in the eyes of the investors.