There are *exactly* 608 US firms offering banking fingerprint authentication

2016/03/23

Dan Latimore

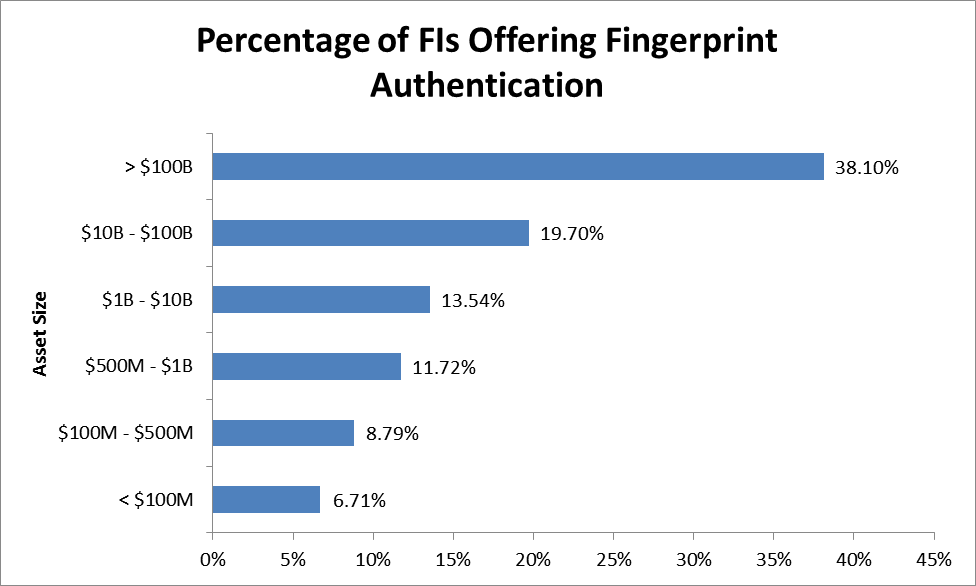

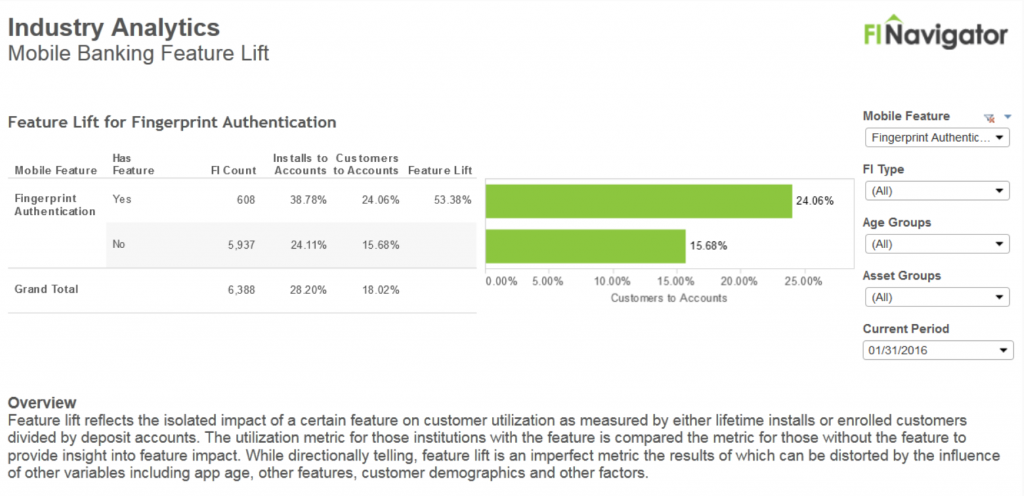

Biometrics are hot. Fingerprint authentication (Apple’s version is Touch ID) is one of the most common forms of biometric verification. So, quick – how many American banks let customers log on to their accounts using this method? Based on the press, you might optimistically think a few thousand, right? And, in fact, ApplePay just activated its 1000th bank (adoption is another story, and the subject of another post). Well, as of January 31, the actual number (not an estimate, not an extrapolation, and not a piece of data from Apple) was 608. That’s 9.52% of the 6,388 FIs offering a mobile banking application. How does that compare to three months ago, at the end of October 2015? At that point just 252 FIs were offering it. That’s an increase of 241% in a quarter, certainly a sign of robust growth. Some of the increase comes from clients implementing from their hosted solution provider. Others (generally bigger banks) are developing it in-house. And yet, it’s not as popular with the large banks as one might think (of the 21 with more than $100bn in assets, only 8 offer fingerprint authentication; 3 of the top 4 have it).  Does fingerprint authentication pay off? By one measure, something we call “feature lift,” it does indeed make a difference for customers. Banks whose customers have installed fingerprint authentication have an uplift of 53% in enrolled customers per deposit account relative to banks who don’t offer it. While this is correlation, not causality, it shows that the banks who offer this feature have more customers enrolled in mobile banking than those who don’t. We’re looking forward to analyzing many more mobile banking features to see which ones offer the biggest impact on customer enrollment.

Does fingerprint authentication pay off? By one measure, something we call “feature lift,” it does indeed make a difference for customers. Banks whose customers have installed fingerprint authentication have an uplift of 53% in enrolled customers per deposit account relative to banks who don’t offer it. While this is correlation, not causality, it shows that the banks who offer this feature have more customers enrolled in mobile banking than those who don’t. We’re looking forward to analyzing many more mobile banking features to see which ones offer the biggest impact on customer enrollment.  How did we access this information? I’m very excited to say that Celent is collaborating with FI Navigator to analyze the mobile banking market in an unprecedented depth of detail. FI Navigator has assembled a database of every US bank and credit union offering retail mobile banking, together with the vendors who host them. We’re feverishly analyzing this trove of data to bring you a report at the end of April. It’s different from, and additive to, work made available to our existing clients; you can find the particulars here. To let you in on how the sausage is made, we originally tried to find out how many banks offered fingerprint ID by doing a standard search (which turned up press releases and the like) and by contacting a few vendors. We were able to arrive at roughly 250 banks in total, including several dozen from one vendor (from whom it was difficult to get precise answers in terms of commitments, scheduled go-lives, and actual implementations). It turns out that we undercounted by more than half. The beauty of the FI Navigator data is that it’s derived from a variety of sources – on a monthly basis – that let us deduce and infer a huge amount of actual information about the entire US retail mobile banking population, not just a subset. By integrating unstructured website data and conventional financial institution data, FI Navigator expands the depth of peer analytics and the breadth of market research to create vertical analytics on financial institutions and their technology providers. So, in addition to my excitement at this new and powerful data source, I have three takeaways about fingerprint authentication:

How did we access this information? I’m very excited to say that Celent is collaborating with FI Navigator to analyze the mobile banking market in an unprecedented depth of detail. FI Navigator has assembled a database of every US bank and credit union offering retail mobile banking, together with the vendors who host them. We’re feverishly analyzing this trove of data to bring you a report at the end of April. It’s different from, and additive to, work made available to our existing clients; you can find the particulars here. To let you in on how the sausage is made, we originally tried to find out how many banks offered fingerprint ID by doing a standard search (which turned up press releases and the like) and by contacting a few vendors. We were able to arrive at roughly 250 banks in total, including several dozen from one vendor (from whom it was difficult to get precise answers in terms of commitments, scheduled go-lives, and actual implementations). It turns out that we undercounted by more than half. The beauty of the FI Navigator data is that it’s derived from a variety of sources – on a monthly basis – that let us deduce and infer a huge amount of actual information about the entire US retail mobile banking population, not just a subset. By integrating unstructured website data and conventional financial institution data, FI Navigator expands the depth of peer analytics and the breadth of market research to create vertical analytics on financial institutions and their technology providers. So, in addition to my excitement at this new and powerful data source, I have three takeaways about fingerprint authentication:

Does fingerprint authentication pay off? By one measure, something we call “feature lift,” it does indeed make a difference for customers. Banks whose customers have installed fingerprint authentication have an uplift of 53% in enrolled customers per deposit account relative to banks who don’t offer it. While this is correlation, not causality, it shows that the banks who offer this feature have more customers enrolled in mobile banking than those who don’t. We’re looking forward to analyzing many more mobile banking features to see which ones offer the biggest impact on customer enrollment.

Does fingerprint authentication pay off? By one measure, something we call “feature lift,” it does indeed make a difference for customers. Banks whose customers have installed fingerprint authentication have an uplift of 53% in enrolled customers per deposit account relative to banks who don’t offer it. While this is correlation, not causality, it shows that the banks who offer this feature have more customers enrolled in mobile banking than those who don’t. We’re looking forward to analyzing many more mobile banking features to see which ones offer the biggest impact on customer enrollment.  How did we access this information? I’m very excited to say that Celent is collaborating with FI Navigator to analyze the mobile banking market in an unprecedented depth of detail. FI Navigator has assembled a database of every US bank and credit union offering retail mobile banking, together with the vendors who host them. We’re feverishly analyzing this trove of data to bring you a report at the end of April. It’s different from, and additive to, work made available to our existing clients; you can find the particulars here. To let you in on how the sausage is made, we originally tried to find out how many banks offered fingerprint ID by doing a standard search (which turned up press releases and the like) and by contacting a few vendors. We were able to arrive at roughly 250 banks in total, including several dozen from one vendor (from whom it was difficult to get precise answers in terms of commitments, scheduled go-lives, and actual implementations). It turns out that we undercounted by more than half. The beauty of the FI Navigator data is that it’s derived from a variety of sources – on a monthly basis – that let us deduce and infer a huge amount of actual information about the entire US retail mobile banking population, not just a subset. By integrating unstructured website data and conventional financial institution data, FI Navigator expands the depth of peer analytics and the breadth of market research to create vertical analytics on financial institutions and their technology providers. So, in addition to my excitement at this new and powerful data source, I have three takeaways about fingerprint authentication:

How did we access this information? I’m very excited to say that Celent is collaborating with FI Navigator to analyze the mobile banking market in an unprecedented depth of detail. FI Navigator has assembled a database of every US bank and credit union offering retail mobile banking, together with the vendors who host them. We’re feverishly analyzing this trove of data to bring you a report at the end of April. It’s different from, and additive to, work made available to our existing clients; you can find the particulars here. To let you in on how the sausage is made, we originally tried to find out how many banks offered fingerprint ID by doing a standard search (which turned up press releases and the like) and by contacting a few vendors. We were able to arrive at roughly 250 banks in total, including several dozen from one vendor (from whom it was difficult to get precise answers in terms of commitments, scheduled go-lives, and actual implementations). It turns out that we undercounted by more than half. The beauty of the FI Navigator data is that it’s derived from a variety of sources – on a monthly basis – that let us deduce and infer a huge amount of actual information about the entire US retail mobile banking population, not just a subset. By integrating unstructured website data and conventional financial institution data, FI Navigator expands the depth of peer analytics and the breadth of market research to create vertical analytics on financial institutions and their technology providers. So, in addition to my excitement at this new and powerful data source, I have three takeaways about fingerprint authentication: - The gap between hype and reality for fingerprint authentication is big, but shrinking;

- Banks don’t have to be large to do this; and

- More banks should be offering fingerprint authentication.

[…] recent report by Celent indicates that 38% of banks with $100 billion or more in assets — there are 21 of them in the […]