Investment management: Structural drivers and sustainable change

Structural drivers are changing the investment industry's economics, but do responses reflect real, sustainable change?

We are having conversations with a handful of asset managers and asset owners who are making plans for systems upgrades in areas such as frontline portfolio construction, risk aggregation, and fund accounting -- the minority is greenfield (from Excel and fortunately so!), and others are to replace what they currently have that is not fit-for-purpose, or they are not happy with their vendor's directional pace (or a lack of it). I would like to make a few observations on where/how the industry is reponding.

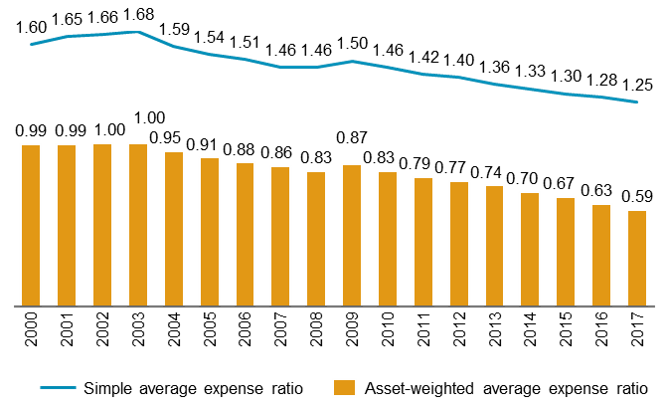

In a time of significant global wealth flows, changing investment paradigms, and shifting technologies, structural challenges continue to sweep the industry, not least from the persistent decline in margins for active managers in part due to the onslaught of passives (index funds, ETFs, and smart beta vehicles).

Source: Investment Company Institute. For the most up-to-date figures about the fund industry, please visit www.ici.org/research/stats.

Nothwithstanding other factors, we expect these price compression trends to continue, and in response to these dynamics, fee structures are changing to better reflect client interests and value for money. Indeed, as part of fee or margin pressure deliberations that concern many of our clients, operational and cost rationalization should be part of the industry's 'toolkit' to unlock the margin compression dilemma.

--------

However, rationalization alone is insufficient. It is our view that a dual approach towards lean costs and upgrading capabilities for enchanced alpha generation will be critical (and more so) in order to navigate opportunities for the future, and to achieve more favourable economics, especially for active managers.

In the flow of conversations about potential systems changes or replacements, what I would like to see are more "strategically framed, but tactically oriented" discussions around technology architecture and data approaches in order to underpin a wealth and asset management firm's go-to-market strategy. That is the focus of my recent research studies and I hope to share some of that in an upcoming 'Trends Shaping Portfolio and Investment Risk Management' webinar session. There will also be showcase examples of emerging technology capabilities, if anyone would like to join us to discuss.