Indian exchanges prepare for greater competition

18 April 2012

Muralidhar Dasar

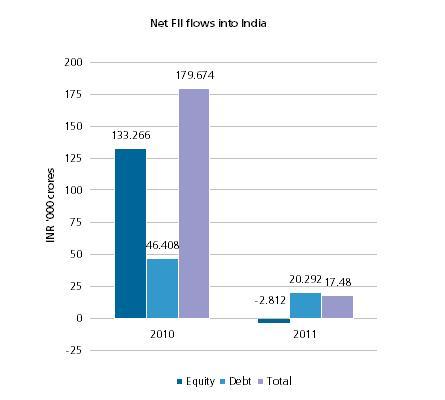

The Indian capital markets regulator, SEBI, is talking reforms as it recently announced a blueprint that is potentially set to increase competition among exchanges. The regulator’s stance on increasing competition and allowing foreign investment in exchanges was closely anticipated in recent months, especially among large global banks. SEBI had to address pressing concerns on attracting foreign investment (Figure indicates the drastic fall in FII inflows into India in 2011) and failing to keep pace with developments in global capital markets. The new move by SEBI has cleared the way for listing of stock exchanges. This decision comes after an expert committee headed by former Reserve Bank Governor Bimal Jalan submitted its report in 2010 on governance and ownership issues relating to market infrastructure institutions. While SEBI has broadly accepted the recommendations, it has gone ahead with the move to allow public listing of exchanges despite the committee recommending against such a move on ‘conflict of interest’ grounds. The blueprint indicates that public holding of exchanges should be at least 51%, while exchange operator, banks and insurance companies are allowed to hold up to 15%. Foreign investors are allowed to hold up to 5%. Exchange operators, however, would not be allowed to list on their own exchanges. SEBI is watching developments in global capital markets closely. The developed markets in US and Europe are far ahead in terms of maturity of market infrastructure, while India is yet to reach a stage where alternative trading venues can compete with incumbent exchanges. The NSE started in 1994 to compete with the then singly dominant exchange, BSE. But ironically the NSE has today itself become what it set out to defeat, accounting for close to 75% of equity volumes. The attention is on regional exchanges to play more aggressively. With an intention to infuse more competition, the regulator has warned that dormant exchanges that are not attracting liquidity would have to be wound up. SEBI has stipulated a minimum annual trading volume of INR 1000 crores for exchanges to continue operating and the same would be reviewed after 3 years. While we see it as a timely warning bell, it is not enough. We have to wait and see how SEBI looks to empower and encourage regional exchanges. The Delhi Stock Exchange has already woken up to the competition by following in the footsteps of LSE in upgrading its IT infrastructure by partnering with MilleniumIT, a technology player which provides ultra-low latency trading solutions. The debate in ongoing in the case of clearing houses and the regulator is expected to come out with its view soon on having a single clearing house versus introducing interoperability. Although it appears that policy challenges facing SEBI are similar to those faced by regulators in developed markets in the past, and despite indications that SEBI is trying to align with developed markets, we should be careful while concluding that the Indian regulator would eventually follow in the footsteps of US and Europe. [caption id="attachment_606" align="aligncenter" width="445" caption="Net FII flows into India"] [/caption]

[/caption]

[/caption]

[/caption]