Fiserv: Changing the Game with RCC

27 January 2010

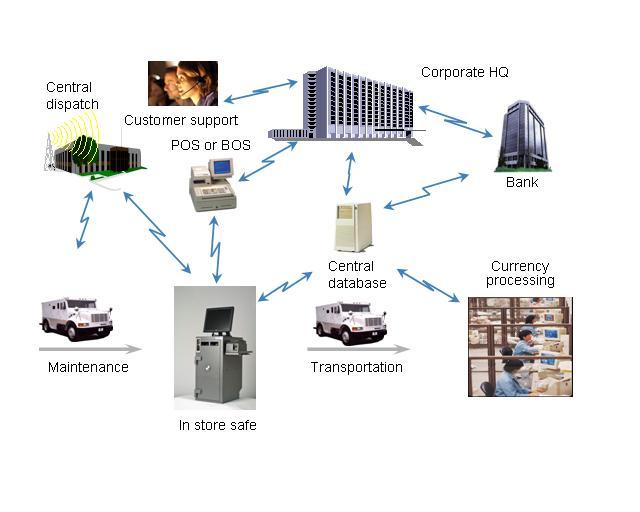

Remote cash capture (RCC) is the deployment of secure, validating currency accepting and recycling equipment (aka smart safes) at merchant locations coupled with information reporting and provisional credit mechanisms. Such equipment has been in use for nearly 15 years in the US as a means to improve merchant cash cycle control. The advent of bank-offered provisional credit based on validated currency residing at the merchant location has been a relatively recent phenomenon with the first implementations in 2004. Its emergence has caused a surge in interest and adoption of these devices. The offering of provisional credit by participating financial institutions has significantly improved the merchant business case for remote cash capture. But, the float benefits involved are secondary. The primary benefit of provisional credit is its enablement of wholesale reengineering of the cash cycle within merchants and between merchants, armored couriers and banks cash vault networks. In the process, RCC removes the substantial cash handling burden historically carried by bank branch personnel, largely without the assistance of meaningful automation. In short, RCC is a win-win-win wherever the merchant business case warrants. Remote cash capture relies upon four components.

- Secure, in-store safes that accept, validate and count currency with a high degree of accuracy and dependability. Such safes have been available since 1995, but have only recently been linked with banks for provisional credit.

- Same-day electronic transmission of the precise safe deposit information to central treasury and optionally, the merchant’s financial institution.

- Ability and willingness for the financial institution to grant ledger credit for remotely validated cash. A growing number of banks are offering provisional credit based on the validated currency. Commonly, cash logistics providers guarantee the funds, covering any losses resulting from discrepancies discovered following physical cash verification.

- Associated cash logistics servicing. This includes armored cash pick-up, change order servicing, web based reporting, deposit aggregation, virtual vaulting and equipment maintenance. [caption id="attachment_1180" align="aligncenter" width="640" caption="RCC's many Moving Parts"]

[/caption]

[/caption]

- The barrier to entry for regional armored couriers will be significantly lowered. This will likely increase competition for RCC solutions at the courier level, improving service levels and settling prices.

- A significant number of smaller banks are likely to enter the fray.

- Service dynamics are likely to become fluid across the board. Historically, the armored couriers were in the driver’s seat, with the banks playing a secondary role – mere providers of provisional credit. Now, banks may start selling RCC while capturing the cash processing business too, rather than conceding it to the couriers. The couriers may evolve to play the lesser role – mere transporters of cash. Should this occur, participating banks could capture more than just deposits with RCC.